- EUR/USD trading in 1.1834-to-1.2050 recuperation range.

- After first weekly gain in four follows ECB action on yields.

- Fed's rate decision & guidance set to dominate this week.

Image © Adobe Images

- EUR/USD spot rate at time of writing: 1.1930

- Bank transfer rate (indicative guide): 1.1512-1.1596

- FX specialist providers (indicative guide): 1.1737-1.1846

- More information on FX specialist rates here

- Set an exchange rate alert here

The Euro-to-Dollar exchange rate opens the new week softer by 0.15% having slipped into a new and lower recuperation range that could become clearer in the eyes of investors this week if the Federal Reserve (Fed) succeeds in calming the bond market and squeezing a recent build-up of hot air out of U.S. exchange rates.

The Euro recorded its first weekly gain for a month lat week having risen 0.34% for the week, closing comfortably above 1.19 and with its most noteworthy intraday move coming after the European Central Bank (ECB) brought forward bond purchases previously scheduled to take place later in the year as part of its quantitative easing programme.

The decision ensures accommodative "financial conditions" amid a global bond sell-off that has lifted borrowing costs for many countries, and as the continent scrambles to ramp up its so-far bottom-of-the-league vaccine programme.

"QE in of itself by the ECB does not necessarily have EUR negative implications given the positive impact on the periphery. But given the current higher momentum in UST bond yields, spreads are having an influence on FX with the lowest yielding G10 currencies suffering most," says Lee Hardman, a currency analyst at MUFG. "The potential for wider spreads and bad news on vaccine roll-outs could over the short-term see EUR weaken further."

The MUFG team sold EUR/USD around 1.1935 on Friday and is looking for a fall to 1.17 in the coming weeks as the continent's economic underperformance weighs in a market where U.S. growth expectations are rising and the Fed is struggling to dissuade investors of the idea that it could lift interest rates sharply as soon as 2023. This has already seen the gap or spread between European and U.S. government bond yields moving in favour of the Dollar.

Above: Euro-Dollar with 200-day moving-average (black), 02-year (orange) & 10-year (purple) German-U.S. yield spreads.

The Dollar's correlation with yields is weak over medium and long-term horizons, while the latter may already have risen as far as they're likely to for now if the Fed pushes back against earlier increases on Wednesday. This would support the Euro and low-yielding currencies that bore the brunt of Dollar's rebound, and may even enable the Euro to mark out a top for its new range on the charts.

"Intraday rallies are now conflicting, but for now while below 1.2014 (September high) downside risk will remain. A close below the 200 day ma will target 1.1750 and the 1.1695/02 support," says Karen Jones, head of technical analysis for currencies, commodities and bonds at Commerzbank. "This is the 38.2% retracement and the September and November lows. The market is expected to hold here and attempt to recover."

ECB action has so-far calmed European bond markets and supported the Euro above its 200-day moving-average at 1.1837 - a likely important level of technical support in the short-term - but may not be enough alone for the single currency to sustain last week's renewed upward momentum.

Source: Berenberg.

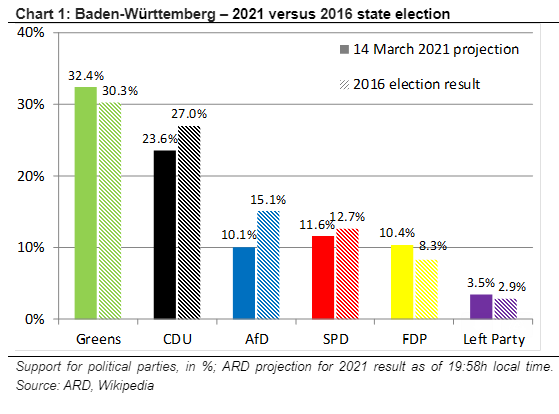

"Despite today’s setback in Baden-Württemberg and Rhineland-Palatinate, the CDU – jointly with its Bavarian sister CSU – remains the favourite to lead the next German government after the 26 September 2021 federal elections and to by and large continue Merkel’s policies. We ascribe a 75% probability to that outcome," says Holger Schmieding, chief economist at Berenberg.

Sunday's polls saw Chancellor Angela Merkel's Christian Democratic Union slide to its lowest ever share of the vote in two states, although they are seen in Germany as unlikely to undermine the ruling party's chance at remaining in post following this September's general election. This could mean they have little relevance for the Euro and that Wednesday's 18:00 Fed decision quickly comes to dominate the agenda for the single currency from early on.

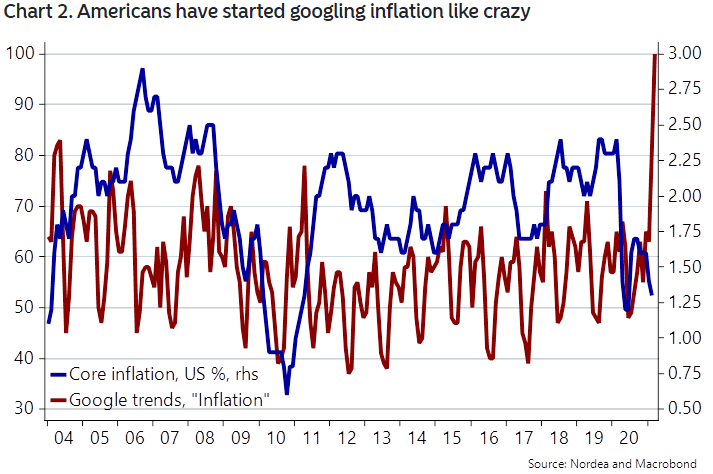

"We enter the meeting leaning short in EUR/USD," says Andreas Steno Larsen, chief FX strategist at Nordea Markets. "The inflationary consensus is already strong and judging from Google trends, it may even have reached levels never seen since we entered a new millennium. Americans googled “inflation” to an extent that is completely out of level with anything seen before, which could be a signal that consumer prices are actually starting to pick up markedly. Average Joe feels it immediately when goods like food and gasoline start rising."

Source: Nordea Markets.

Last week's sign-off by President Joe Biden on a $1.9 trillion financial aid package that includes up to $1,400 of 'helicopter money,' which could reach qualifying households as soon as this week, has lifted market expectations for GDP growth and could help to support already-elevated U.S. inflation expectations. To many this, combined with an increasing momentum in the U.S. vaccination programme, has justified recently increasing market expectations for as many as three Fed rate hikes as soon as 2023.

But markets have evidently forgotten that forecasts for the economy were improving, the job market had already bottomed out and inflation expectations recovered when in November 2009 the Federal Reserve surprised the market by announcing its second ever quantitative easing programme. Expectations for a rising rate signal also overlook tighter financial conditions resulting from the rising Dollar, higher yields and declines in stock markets, among other things, which the Fed may want to rectify this week.

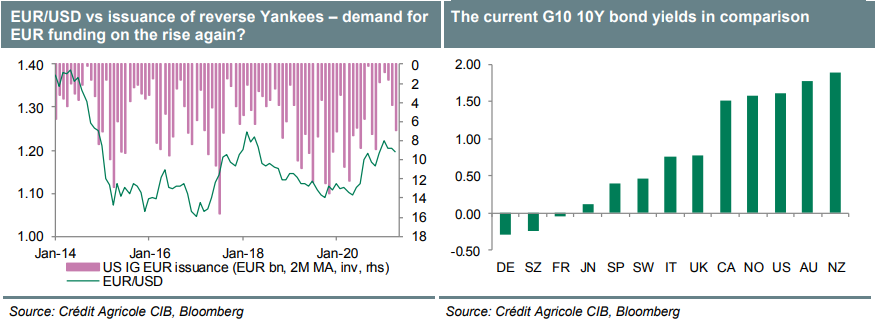

"We doubt that the Fed will want to be seen as ‘adding fuel to the fire’ by encouraging market speculation about a potential withdrawal of its monetary stimulus. We think the FOMC will maintain its cautious inflation outlook even as it presents its upgraded economic projections. Moreover, we believe that the updated Fed dot-plot would largely reaffirm the view that policy rates will remain at their current low levels in the coming years," says Valentin Marinov, head of FX strategy at Credit Agricole CIB. "A more dovish-than-expected outcome from the Fed meeting can boost risk sentiment and weigh on the USD."

Source: Credit Agricole CIB.

Investors who're wagering or otherwise expecting a signal that a 2023 rate hike is in the cards will also have overlooked that the Fed is now seeking more bang for its buck in terms of inflation than is the case with other central banks, which necessitates a "lower for longer" rate stance.

The Fed's new average-inflation-targeting policy means it now has to generate even more inflation than was the case previously, or is currently the case elsewhere, because an overshoot of the 2% target is now its stated objective. This means lower-for-longer than would otherwise be necessary.

In other words and despite that last week's fiscal stimulus is a big positive for the U.S. growth outlook this year, it may not be enough to keep the Fed from coming across as 'dovish' in its rhetoric or actions this Wednesday, which could support the Euro from mid-week on.

"EUR/USD has held good support near the 200-day moving average at 1.1830 and the big question is: was that the correction? With US Treasury yields still near 1.60% and a big Fed event risk to come next Wednesday, it is probably too soon to declare that EUR/USD is ready to resume its rally," says Chris Turner, global head of markets and regional head of research at ING, who tips a 1.1834-to-.2050 range for EUR/USD this week. "Covid challenges in continental Europe aren’t helping the EUR either, where rising case numbers, slow vaccine roll-outs and doubts about the AstraZeneca vaccine are all delaying recovery hopes."