- EUR/USD underwhelms in wake of vaccine news

- But, Soc Gen anticipate a recovery

- Interest rate outlook a significant USD headwind

Image © Adobe Images

- EUR/USD spot rate at time of publication: 1.1793

- Bank transfer rates (indicative guide): 1.1380-1.1463

- Transfer specialist rates (indicative guide): 1.1680

- More information on superior exchange rates here.

The Euro has proven to be an unexpected loser of the positive investor sentiment triggered by news Pfizer had succeeded in developing a vaccine that is able to protect against Covid-19 infection, but one leading foreign exchange analyst says the single currency can yet make a powerful comeback.

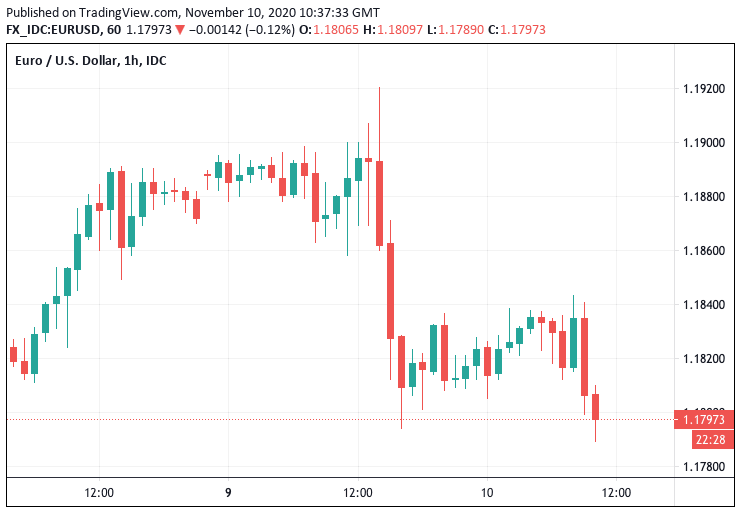

The Euro fell half a percent against the U.S. Dollar on Monday and has extended a further 0.11% lower on Tuesday to reach 1.1797, however Kit Juckes, Global Head of Foreign Exchange Research at Société Générale, says there is a good chance the EUR/USD exchange rate will hit 1.20 by the time December comes around.

"There's nothing here to make me bullish of the dollar unless the Fed makes a very dramatic U-turn," says Juckes in a daily briefing to clients. "That's enough to make me think that EUR/USD will continue to hold above 1.16 support and will probably break the year's high just above 1.20 before the end of the month."

The foreign exchange text book says the Dollar is a classic safe haven that should rise when equity markets are falling and decline when they are rising. The eye-watering gain in equities that followed news that Pfizer's vaccine had a 90% success rate should therefore have been on balance positive for the Euro.

Above: EUR/USD has fallen over the past 24 hours. If you are looking for a better exchange rate it could be worth considering a market order that would allow you to automatically transact when your ideal rate is reached. Learn more here.

However, it is too soon to suggest a major shift in foreign exchange market relationships has suddenly transpired over the past 24 hours and the outlook for the Euro-to-Dollar exchange rate is constructive, with Juckes saying in a recent research note that a 9-year dollar rally, started by the ECB, was ended by the Fed and politics can't change that.

"The ECB’s rate hikes took EUR/USD back close to 1.50. Inflation, above 3% that summer, was back below 1% by 2013, by when the economy wasn’t growing either. The Japanese, in the meantime, had succeeded in dragging the yen back from the massive overvaluation that followed the financial crisis and the appointment of PM Abe at the end of 2012 helped push the yen lower too," says Juckes.

Juckes explains the market's subsequent evolution:

"The market started to speculate about the timing of Fed policy normalisation from the summer of 2012 onwards.2-year note yields had reached their low point in mid-2011, a little above zero, longer yields turning higher a year later. 2013’s ‘taper tantrum’ accelerated the process, though it caused enough market turmoil to make the FOMC think twice.

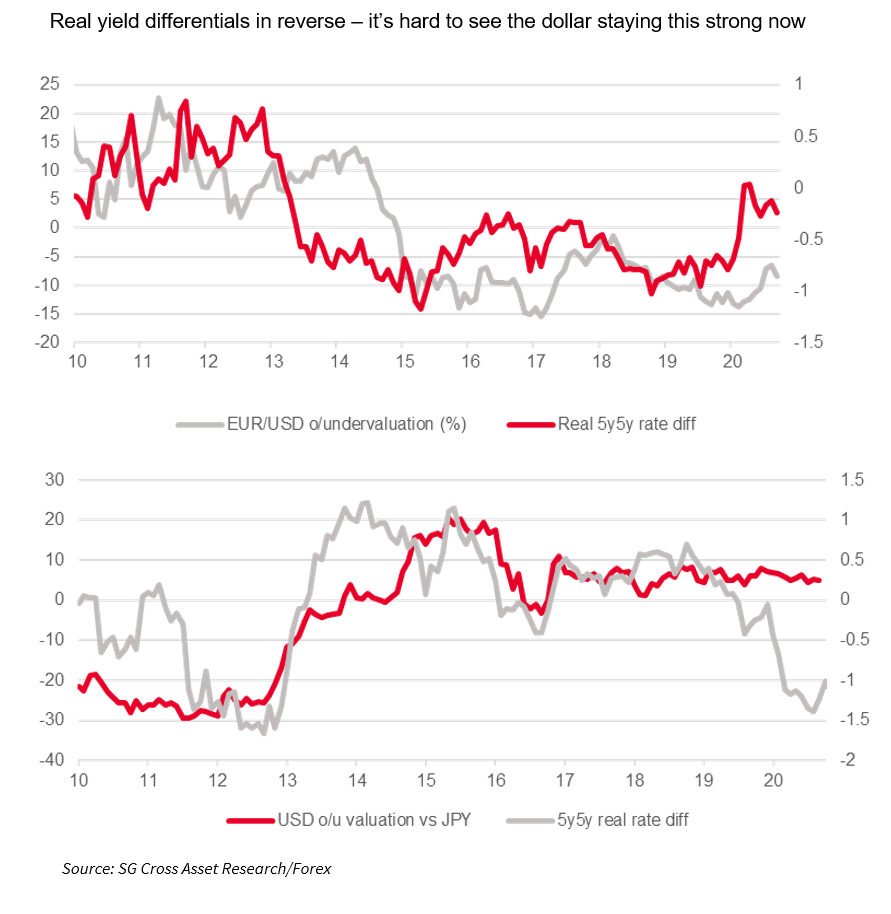

"But the Fed was clearly on a path to tighter policy, while the ECB and BOJ equally clearly weren’t. The election of President Trump saw the rise in yields accelerate and the Fed continued hiking through 2018. 2019 saw the dollar gain a bit against the euro, lose a bit against the yen, while the market focused more on emerging market developments, but COVID19 has eclipsed everything else in 2020. And the Fed, by the aggression of its policy actions in March, and shift in strategy this summer, has manged to reverse most of the rise in real yields seen by Treasuries relative to other countries, that we have seen in recent years."

For the Société Générale analyst the yield paid on government and corporate bonds on either side of the Atlantic will remain a key driving factor of foreign exchange valuations over coming days, weeks and months.

Importantly, the election of Joe Biden to the White House at the weekend will have little effect on the Dollar's trajectory from here.

"The real yield advantage that allowed the dollar to be 10% overvalued against the euro and even, slightly overvalued against the yen, has been blown aside. The last time real yields were this much higher in Japan than in the US, the yen was 20% overvalued, which would take it to USD/JPY 80 today. Could a new President do anything to change that?" asks Juckes.

He says a change in leadership can of course have a meaningful impact - as per the Treasury market after 2016 when Donald Trump rose to power - "but after a long period when the Fed was tightening and Europe/Japan were easing monetary policy, rates and yields have reconverged. And there’s still a chance that the next big policy change comes from the Eurozone grasping the nettle and adopting a more sustainable fiscal policy structure," he says.