Image © Adobe Images

- EUR/USD spot rate at time of writing: 1.1838

- Bank transfer rate (indicative guide): 1.1420-1.1503

- FX specialist providers (indicative guide): 1.1656-1.1727

- More information on FX specialist rates here

The Euro-to-Dollar rate could see more bouts of profit-taking that serve to draw it further away from recent highs in the weeks ahead, according to strategists at Deutsche Bank and other firms, although analyst forecasts for the single currency still favour a bullish year-end outcome.

Europe's unified unit had bucked the major currency trend that saw Dollars bought early in the Thursday session with other riskier currencies having been sold although even the Euro was found trading lower against the greenback during mid-morning hours.

Barring the intermittent resilience weakness has effectively extended from Wednesday into Thursday but follows explosive gains that were seen earlier in the week, which lifted the Euro-to-Dollar rate back above 1.19 and to its highest levels since May 2018.

"We have been vocal EURUSD bulls since 1.10 and argued for an acceleration in dollar weakness as EURUSD reached 1.15 in July. But with EURUSD having (nearly just) reached our 1.20 target earlier this week we now favor taking profit and see a more balanced outlook as we approach September," says George Saravelos, head of FX strategy at Deutsche Bank.

Above: Euro-to-Dollar rate shown at 15-minute intervals alongside S&P 500 futures (orange line, left axis)

Wednesday and Thursday losses have all the hallmarks of profit-taking by speculative traders, which is something that Deutsche Bank sees potentially marring the Euro's performance further toward the end of the third quarter. It bought the Euro at 1.10 but is advising its clients to cash out.

The Euro has surged since mid-May when France and Germany unveiled proposals for the now-EU coronavirus recovery fund that will bolster Brussels' multiannual budget with grants and loans for virus-stricken members.

"Greater Eurozone fiscal solidarity, widening real EU‑US two‑year swap spreads and relative central bank balance sheet expansion trends between the ECB and the Fed suggest further upside to EUR/USD. We forecast EUR/USD to lift to 1.2300 by year‑end. We do not expect new material information from the ECB’s July monetary policy meeting account today," says Carol Kong, a strategist at Commonwealth Bank of Australia.

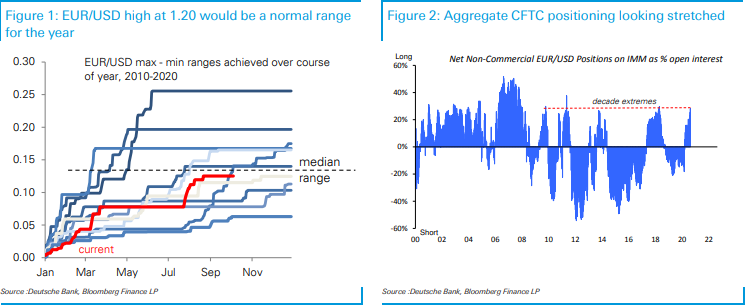

Above: Deutsche Bank graphs showing positioning EUR/USD range extremes over 10 years and net investor positioning.

The rally gathered pace in late July, not long after the recovery fund won a sooner-than-expected endorsement of national leaders, setting it on course to become operational with the next EU budget in January 2021.

Europe's rally has been supported if-not driven by the evolving positioning of speculative investors as recorded by the Chicago Futures Trading Commission, which has seen the market flip from being 'net-short' to having the largest 'net-long' since the aftermath of the Eurozone debt crisis and associated landmark pledge by then-European Central Bank chief Mario Draghi to "do whatever it takes" to keep the Euro currency and political union alive.

"Positioning is a bigger concern now," writes Saravelos, who estimates a 'fair value' of around 1.20 for the Euro. "What about the macro? Our framework for the dollar back in May broke down the move into two phases. Phase I of dollar weakness from 1.10 to 1.15 was all about the removal of the COVID risk premium. Phase II of the move has been about the end of US exceptionalism across multiple fronts: yields; growth and policy activism. All three have reversed to the detriment of the dollar in recent months."

Above: Euro-to-Dollar rate shown at daily intervals alongside S&P 500 futures (orange line, left axis)

Thursday's weakness in the Euro came as investors mulled minutes of the July Federal Reserve (Fed) meeting in a session that also offers more about recent European Central Bank (ECB) deliberations as well as the path of Turkish interest rates. The Fed turned its nose up at the idea that a so-called 'yield curve control' policy could help shepherd the economy back to normal trading conditions but otherwise came across as keen to offer further support.

Price action in financial markets has been somewhat volatile with much back-and-forth for currencies, commodities and the stock markets that many things have followed of late, with multiple narratives competing to explain nascent trends. But the Euro's correlation with S&P 500 has remained robust.

"The sharp correction in EUR/USD yesterday on the back of a relatively modest correction lower (-0.44%) in the S&P 500 from a record high is further evidence of where short-term USD risks lie," says Derek Halpenny, head of research, global markets EMEA and international securities at MUFG, who forecasts a yar-end Euro-to-Dollar rate of 1.20. "The Fed looks less likely to announce any new meaningful policy strategy in September which could help remove some near-term downside risks for the dollar. Our view of potential near-term USD correction stronger therefore remains intact with scope for EUR/USD to correct further lower in the coming days and weeks."