- Potential 'Evening Star' reversal pattern is forming on GBP/EUR charts.

- As technical forecster tips turnaround from 1.1481 and fall toward parity.

- Comes with EUR tading like EM currency, rising and falling with the ZAR.

- After March spat over corona bonds stokes renewed EUR breakup fears.

Image © Adobe Images

- Spot GBP/EUR rate at time of writing: 1.1473

- Bank transfer rates (indicative): 1.1177-1.1258

- FX specialist rates (indicative): 1.1307-1.1376 >> More information

Pound Sterling's two-week rally against the Euro has faded over the course of the past 48 hours and it could eventually turn back towards financial crisis lows according to signals emerging from the market's set-up, which suggests GBP/EUR is about to complete an 'evening star' candlestick reversal pattern.

Sterling has risen nearly 10% against the Euro since March 16 when it bottomed out after a -12.6% decline that began on February 18, but the recovery has now brought it into contact with the 61.8% Fibonacci retracement of the 2020 downtrend and 55-day moving-average of prices, which both offer resistance.

These levels give insights into the technical setup in the market, which in turn offers clues as to how the future might play out for the exchange rate pair.

In addition, this week's price action has led to the formation of a potential evening star reversal pattern on the daily chart that, if completed, would indicate a sharp turn lower from here.

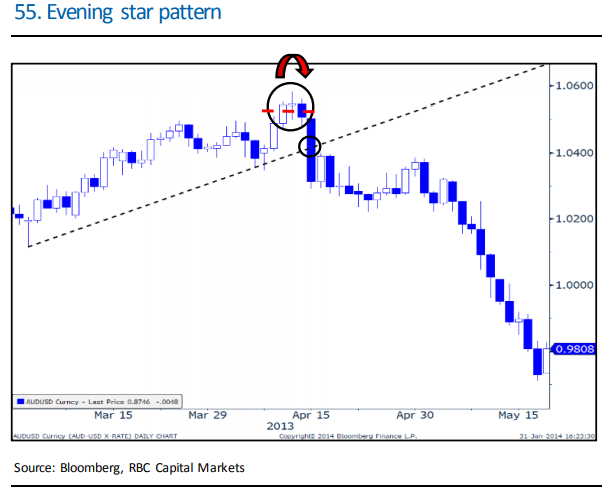

"The first day of price action reinforces the overall bullish trend. However, the formation of a star on the second day, with a small real body, indicates a potential change in sentiment. This is magnified by the third candle, which produces a strong countertrend selloff and closes below the mid-point of the first day," says George Davis, chief technical strategist at RBC Capital Markets, in a brochure explaining key concepts to clients. More on that here.

Above: RBC Capital Markets graph shows evening star reversal pattern.

Davis says "penetration of a support level will often confirm the bearish implications" of the evening star pattern.

However, in this instance Sterling will be left sat on top of its 200-day moving-average, a notable support level but one which is tipped by other analysts to give way in the coming days.

"We note a 13 count on the 60 minute chart and positive intraday Elliott wave counts – they imply the end of the down move. A recovery above .9022 is needed to target .9225 and then the March high at .9501. Above .9501 all we have is the .9803 2008 high," says Karen Jones, head of technical analysis for currencies, commodities and bonds at Commerzbank, referring to EUR/GBP.

Jones has warned that a close above the April 14 Pound-to-Euro rate high of 1.1520 will negate her outlook for an eventual EUR/GBP rise to the 0.9803 high seen in the 2008 financial crisis, which gives a GBP/EUR rate at 1.0200.

She says that in order for Sterling to get down there a number of other important levels first need to give way, with those being 1.1084, 1.0840 and 1.0525 when expressed in Pound-to-Euro terms.

Those latter levels could all act as support for Sterling along the way and temper the pace of the anticipated decline. Jones advocated Thursday that Commerzbank clients bet on a fall in the Pound-to-Euro rate from 1.1412 but to abandon the pursuit if prices hit 1.1520.

Above: Pound-to-Euro rate at daily intervals with Fibonacci retracements of 2020 downtrend and selected moving-averages.

There was also more fundamental support for a Pound-to-Euro rate turn lower coming out of Europe on Thursday after Prime Minister Guiseppe Conte was reported by the Italian press to have said late in the prior session the country should "look at the ESM proposal after approval." His remarks were reported after European Council President Mario Centeno told Corriere della Sera that so-called corona bonds have not been ruled out by the top chamber of decision makers for the European Union and Eurozone.

This is important for the Euro because there's a European Council meeting on April 23 in which the bloc's shared response to the coronavirus crisis must be unanimously approved to avoid a political disaster that could have severe economic side effects. Italy's Conte indicated last week he would not support the proposed response because it requires struggling Southern European countries to tap the crisis era bailout fund that foisted humiliating doses of austerity and supervision on many during the debt crisis.

"Italy’s reluctance to request an ESM PCS (Pandemic Crisis Support) credit line makes the activation of the ECB’s Outright Monetary Transactions (OMT) even less likely. It also betrays a fear of the stigma that was associated with EU sovereign bailouts in the first iteration of the Eurozone crisis in 2009-2012. In this context a further widening of Italian spreads make sense," says the ING rates team in a Thursday research briefing."We had concerns earlier this week that the ECB did not stop the Italian bond sell off. Price action yesterday morning seems to have been followed by ECB intervention...but this failed to completely reverse the move."

Italian support for the collective fiscal response to the economic threat posed by coronavirus, and European contemplation of a mutualised debt instrument to sit alongside the mutualised currency is important because the crisis has stoked fresh concerns about debt sustainability on the 'periphery' of Europe and the resulting fractious debate about burden sharing or debt mutualisation has incited renewed concerns about a possible breakup of the currency bloc further down the line. Readers can find more on all of this here and here.

Above: Pound-to-Euro rate at daily intervals alongside ZAR/USD (orange line). Positive correlation turns negative March 26.

Casual observers may not have realised the March 25 corona bond proposal of nine countries and subsequent March 26 rejection of it has stoked debt-crisis-level concerns about the long-term prospect of the currency bloc remaining intact because the response of the bond market has been benign in the historical context. This is thanks largely to a European Central Bank (ECB) that once said "we're not here to close spreads" but which has ultimately sought to do exactly that when the situation called for it.

The ECB has added €850bn to its quantitative easing bond buying programme since the onset of the coronavirus crisis and tilted new purchases heavily toward the two most afflicted countries; Italy and Spain. Those countries are also the Eurozone's two most economically and financially vulnerable at the best of times although the 'spread' - or difference in bond yields between those countries and Germany - is less than 2% in 2020 when between 2011 and 2013 it hit 7.5% and sank the Euro as investors feared the intersection of politics in one part and unsustainable borrowing costs in the other would lead to a break-up of the bloc.

This action from the ECB under new President Christine Lagarde has nipped a financial crisis in the bud before it even really began and obscured the true level of concern that exists among investors in the bond market but, and for the time being at least, the currency market is still a freely functioning market and one where there is no so-called 'Fed put', Lagarde mettre or Maradona-like 'hand of god'. In some parts of this market the signs of stress are more clearly observable and one such place is in the Pound-Euro rate, which had a positive correlation with the South African Rand until very recently. That positive correlation went into reverse on March 26 when EU leaders rejected the idea of corona bonds and drew fierce criticism from Italy in the process.

Some observers noted how the Brexit referendum left the Pound trading like an emerging market currency but in 2020 Europe's unified unit was the only emerging market currency in the Pound-to-Euro rate, which now moves in the opposite direction to the ZAR/USD rate. In other words, the Euro now rises and falls with the Rand as it did back in the debt crisis and as Sterling did following the Brexit referendum as well as in the dark days of the financial crisis.

That could matter for the Pound-to-Euro rate over the coming weeks because some analysts say the sell-off in the Rand is now overdone, while the South African unit was lifting off its recent lows earlon Thursday.