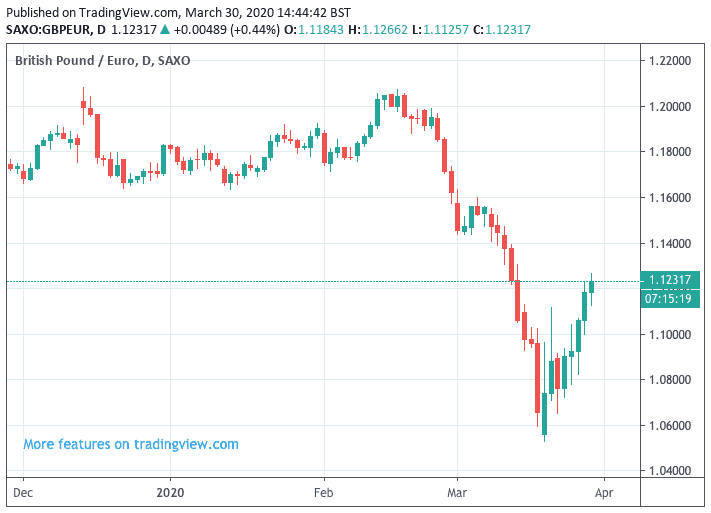

- GBP/EUR recovers above 1.12

- Widespread EUR weakness is key driver

- Eurozone states unable to agreed joint fiscal approach to coronavirus impact

- GBP bats off Fitch credit downgrade

Image © Pound Sterling Live

- GBP/EUR spot at time of writing: 1.1226

- Bank transfer rates (indicative): 1.0933-1.1012

- FX specialist rates (indicative): 1.1100-1.1125 >> More information

A broad-based decline in the Euro has allowed the Pound to build on its late-March recovery, with Monday's 0.75% gain in purchasing power taking the Pound-to-Euro exchange rate back above 1.12 to 1.1260.

The key element in the GBP/EUR exchange rate's advance does appear to be related to the Euro's waning fortunes; the clue being a 1.0% decline in the world's most liquid pair, the Euro-Dollar exchange rate. However, as we note in this article there are some industry specialists who now see relative value in betting on a broader recovery in Sterling against its continental neighbour.

"EUR’s five-day streak is set to end through today’s session as the currency makes a move below 1.11 and toward the 1.1050 mark," says Shaun Osborne, Chief FX Strategist at Scotiabank. "Domestic developments centred on rising COVID-19 cases and casualties in the bloc—in Spain, intensive care requirements have exceeded the country’s capacity during the weekend—while Eurozone governments have yet to agree on opening up the European Stability Mechanism—which would come to the rescue of those most afflicted peripheral countries, such as Spain."

John Hardy, Saxo Bank's Head of FX Strategy, says the inability of Eurozone countries to agree on an unified response to the economic toll meted out the coronavirus outbreak is a likely driver of the Euro exchange rate complex's relative underperformance.

"Peripheral spreads are pushing back wider this morning after last week’s disastrous EU video-summit. How does Europe get on the same page? Euro may languish until it does – especially versus JPY if risk sentiment comes under pressure again," says Hardy.

'Peripheral spreads', refers to the the difference paid on government debt by the Eurozone's weaker countries (Greece, Spain, Italy) versus the Eurozone's core countries (Germany, France, Netherlands). If the spread on the yields widens it suggests investors demand more compensation for holding the debt of the likes of Spain and Italy, hardly surprising if we consider the trajectory of the coronavirus outbreak in these two countries.

Last week saw Eurozone finance ministers try and thrash out an unified response to the economic toll of the coronavirus, with some countries asking that the Eurozone set up a joint bond that would be issued to finance the recovery from the crisis. However, core nations such as the Netherlands are understood to be firmly against such an outcome.

In short, the Eurozone remains divided when it comes to fiscal unity, and this could be a consideration for investors when considering the Euro.

"After the unprecedented support packages pushed through last week, the only one missing was for the European Union as a whole. The leaders there could not agree to launch coronavirus bonds on a pan-European level. This did not go down well with markets," says Christian Gattiker, Head of Research at investment bank Julius Baer.

Analysts who watch the options market warn of sizeable expiries in EUR/USD due today, which has been cited by some as being partly behind the decline in value of the Euro.

Indeed, putting a finger on the exact cause of the Euro's weakness at the onset of a new week is difficult to do in the current context of high market volatility and we do note that month-end is fast approaching which tends to be a time of large capital flows that can shift currency valuations.

Gauging the scale of the flows, and which currencies will ultimately benefit, is however a difficult task. One analyst we follow says the Euro should actually benefit at the expense of the Dollar at the end of March as portfolios adjust their currency exposure owing to last week's large rally in stocks.

Perhaps this rebalancing will still play out and provide the Euro with some strength over the next 24 hours or so.

Regardless, the declines in the Euro have allowed GBP/EUR to build on the 2.77% advance recorded last week, ensuring Sterling whittles down March's decline to 3.12%.

The month's low was recorded at 1.05195 and it did appear at the time that Sterling was en route to breaking the all-time low set in December 2008 at 1.02.

According to Saxo Bank's Hardy, the contrast between the UK and the Eurozone's inability to agree a unified fiscal approach to dealing with the economic impact of the coronavirus outbreak could be one reason to gear up for a recovery in GBP/EUR.

"Is it worth it for Sterling bulls to set up shop soon in EUR/GBP – on the argument that sterling is cheap and the UK is more ready and willing on fiscal measures and stabilisers in the needed size," says Hardy.

The UK government has thus far agreed a total support package of direct tax and spending measures to the tune of £119bn (5.3% of GDP), according to analysis from Capital Economics. Fitch estimate that the whole package will cost 4.4% of GDP in 2020.

The efforts of the government are meanwhile done in close coordination with the Bank of England who have initiated numerous schemes aimed at providing businesses with finance while unleashing a new wave of quantitative easing which should ease financial pressures.

It is this joined-up approach that the Eurozone lacks, and could yet benefit Sterling against the Euro.

The call by Hardy comes as markets are left considering the implications of a downgrade to the UK's sovereign debt (gilts) by ratings agency Fitch over the weekend.

The agency cited the twin issues of a surge in government spending and uncertainty over future EU-UK trade relations as why investors should turn more cautious on the ability of the UK to service its public debt over coming years.

When downgrading the UK's sovereign debt rating from AA to AA-, Fitch said they took into account, "the deep near-term damage to the UK economy caused by the coronavirus outbreak and the lingering uncertainty regarding the post-Brexit UK-EU trade relationship".

However, financial markets appear to have paid little regard to Fitch's move as demand for UK gilts has actually risen on Monday, driving down their yield.

"Much ado about nothing," says Shaun Osborne, Chief FX Strategist at Scotiabank. "Major bond markets are mostly firmer, driving yields lower; Gilts are outperforming despite the UK’s sovereign downgrade by Fitch on Friday."

Osborne notes the downgrade partly led to an up to 1%+ drop for the GBP in the early hours which it has since faded.

"The GBP may be gearing up for an important appreciation in the coming weeks if the PM’s team puts forth an extension request to the EU-UK trade talks amid the coronavirus outbreak, with the government facing pressure from business bodies at home. A poll released over the weekend also showed that around two-thirds of Britons think the government should extend the transition period beyond end-December."