Last week we finally got the first significant piece of economic data since June’s Brexit vote and it was not good news for the UK economy or the Pound.

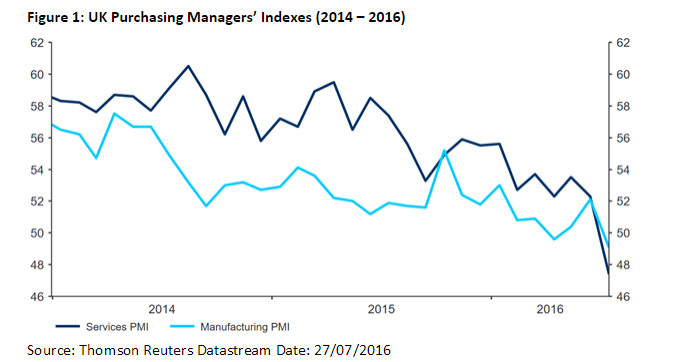

The July manufacturing and services PMIs both fell sharply, down to below the critical level of 50 that denotes contraction in activity.

The manufacturing sector suffered its worst month since February 2013, while the UK’s dominant services industry, which accounts for almost 80% of overall economic output, plunged by the most since records began in 1996, slumping to a seven year low of 47.4 (Figure 1).

Figure 1: UK Purchasing Managers’ Indexes (2014 – 2016)

Source: Thomson Reuters Datastream Date: 27/07/2016

The contraction has since been backed up the monthly Manufacturing PMI release on the 1st of August.

These numbers are consistent with a 0.4% contraction in quarterly GDP and we now see it as highly likely that the UK economy will contract in the third quarter of 2016.

We’re already pencilling in around a 0.2 - 0.3% contraction and see a moderate chance that the UK could enter into recession in 2016 for the first time in 7 years.

Unsurprisingly, Sterling fell sharply on the back of the news and is now trading just above the 31 year low versus the US Dollar reached earlier in the month.

The Pound also received little help from Monday’s uninspiring CBI Industrial Trends survey, while Friday’s consumer confidence data from Gfk experienced its largest decline since 1990.

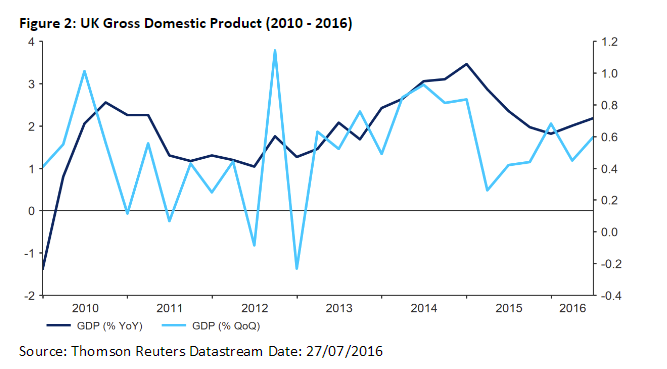

This week’s GDP figures were far more encouraging, with the economy growing 0.6% in the second quarter (Figure 2). However, they reflect economic activity prior to the referendum.

Figure 2: UK Gross Domestic Product (2010 - 2016)

Source: Thomson Reuters Datastream Date: 27/07/2016

Following the bleak PMI data, investors are now facing the prospect of the first interest rate cut by the Bank of England since the financial crisis in March 2009.

The Bank of England kept monetary policy unchanged and failed to explicitly commit to further stimulus despite the furore caused by June’s shock Brexit vote.

However, expectations that the Bank of England will cut rates has grown since the weak PMI data. Financial markets are now placing more than 95% probability of a rate cut at next week’s meeting, up from 75% before the July meeting.

Martin Weale, who is one of the more hawkish members of the monetary policy committee, recently suggested that he will join Gertjan Vlieghe and vote for an immediate cut in August.

Chief economist Andy Haldane, a staunch advocate of loosening monetary policy, is also almost certain to vote for a cut.

In fact, of all the policymakers to speak since the Brexit vote only Kristin Forbes has failed to throw support behind immediate action.

We think that the dismal economic data since the Brexit vote will force the central bank’s hand when it next meets on 4 August.

We expect at least a 25 basis point cut in the benchmark interest rate and, at the very least, an explicit hint that an expansion in the central bank’s quantitative easing programme might be on the way later in the year.

How Sterling will react to this is unclear, however, we believe that a rate cut is largely priced into the Pound already.

During the remainder of 2016, we would expect Sterling to be able to hold its own against the US Dollar. Should the European Central Bank expand its own quantitative easing programme in the last quarter of 2016, we should see Sterling retrace at least some of its recent losses against the Euro.