The Australian Dollar Tends to Struggle in May

- Written by: Gary Howes

- Reference quotes:

- Australian to US Dollar exchange rate: 0.7472

- Pound to Australian Dollar exchange rate: 1.7313

- Euro to Australian Dollar exchange rate: 1.4570

- Australian to New Zealand Dollar exchange rate: 1.0882

Analysts are anticipating the Australian Dollar’s recent poor run to extend into the month of May based on current momentum, market positioning and seasonal factors.

The Australian Dollar has endured weeks of selling against the Euro, Pound and even the US Dollar which itself hasn’t had a stellar year so far.

Analyst Saktiandi Supaat at Maybank in Singapore says he believes the Australian currency will remain under pressure over coming weeks based on the following three observations:

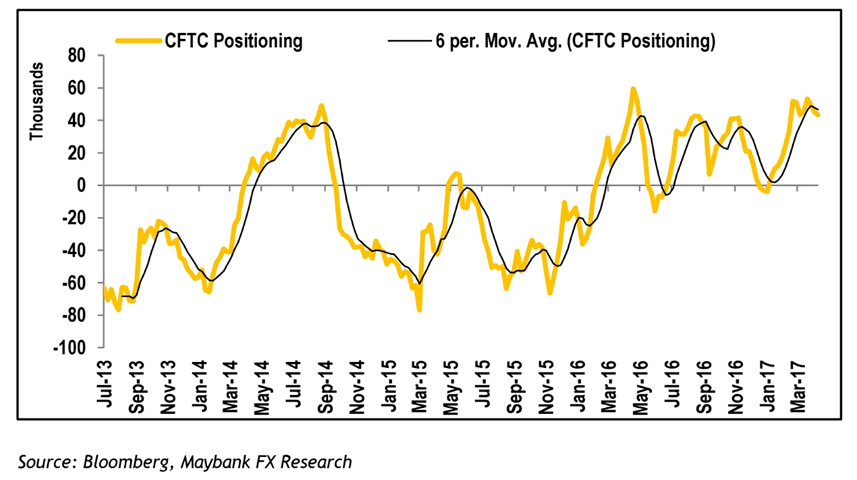

1) Markets have Stretched their Positioning on AUD

Latest data from the CFTC suggests speculative traders continue to hold bets that seek to profit on the Australian Dollar rising.

In fact, so many traders are betting this way that the trade is crowded and at risk of a sharp reversal as is often the case when a crowded trade runs into reality and traders have to bail out.

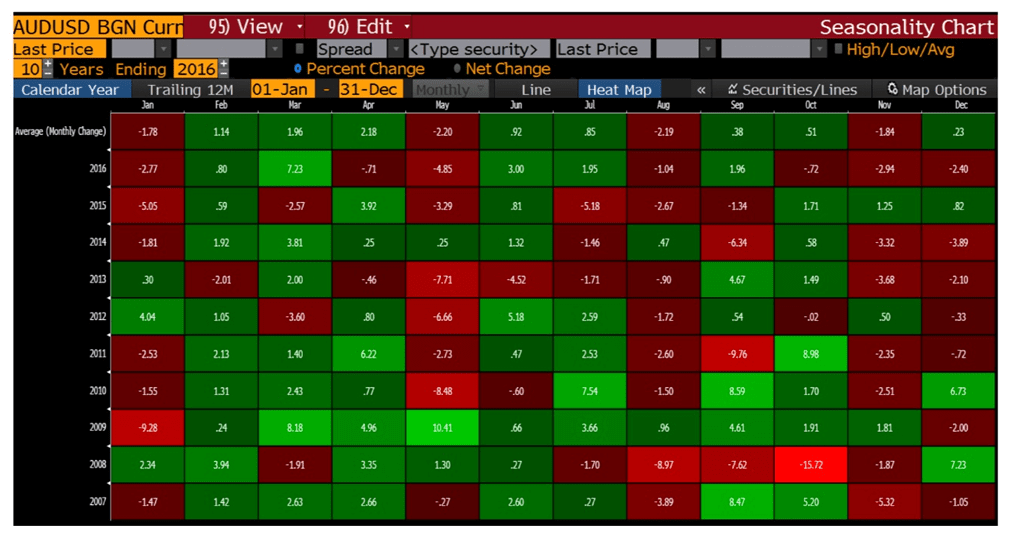

2) May Doesn’t Like the Aussie Dollar

“We move into a seasonally bearish month of May where AUDUSD has recorded steep declines in 7 out of 10 Mays in the past 10 years,” notes Supaat.

Odds are therefore in favour of another May of losses.

As we have noted here, May tends to be a good month for the US Dollar, and this adds to the weight of potential downside to AUD/USD. Seasonality is a useful guide on future performance we believe.

Indeed, witness the Pound rising in April as it has done for the past decade.

Supaat expects, “a potential USD resurgence into the next month given strong seasonality factor, some support to the greenback from potential EUR selling after a Macron-victory and a possible disappointment for those who expects ECB to taper/tighten soon.”

3) The Risks Ahead

Supaat also believes risk events lie ahead, like Australia’s Federal Budget on 9 May that could trigger a credit rating downgrade threatened repeatedly by S&P.

Meanwhile, it is unlikely the Reserve Bank of Australia will show any appetite for raising interest rates soon, particularly as Australian inflation continues to underwhelm.

For the second time (in a row), Australia’s inflation missed expectations this month.

The headline CPI came in at 0.5%q/q, steady from the previous quarter, driven mostly by fuel, housing, health, transport and education. Year-on-year, CPI narrowly missed the median forecast of 2.2% with a print of 2.1%, albeit still an acceleration from the previous 1.5%.

Nonetheless, inflation is finally back within RBA’s target range of 2-3%. Underlying inflation rose to 1.80%y/y from the previous 1.55%.

“While price pressure saw a general rise for the first quarter, in tandem with a modest pick-up observed in the rest of the World, we have written before in our notes that the inflation trajectory is neither compelling enough for RBA to hike nor weak enough for the central bank to drop the cash target rate from the current 1.5%. The central bank remains caught between a rock and a hard place given soft labour conditions and lofty housing prices,” says Supaat.