Australian Dollar at Risk as Storm Clouds Gather Over China

The global reflation story which has powered equity markets higher, driven Commodity prices up and led to a resurgence in risk appetite may soon reach a climactic end.

This is the view of Aurelia Augulyte, a foreign exchange analyst at Nordea Markets, the scandanavian financial services giant.

And if correct, this will have some very real implications for the star performer of currency markets thus far in 2017 - the Australian Dollar.

“While the world is cheering and the pro-risk environment persists, I retain my sobering view that we will face a reality check within a few months,” says Augulyte in a research note to clients seen by Pound Sterling Live. “One big part of it is China, which not only will precede a global reflation fade from March onwards, but also lead a slowdown in global demand.”

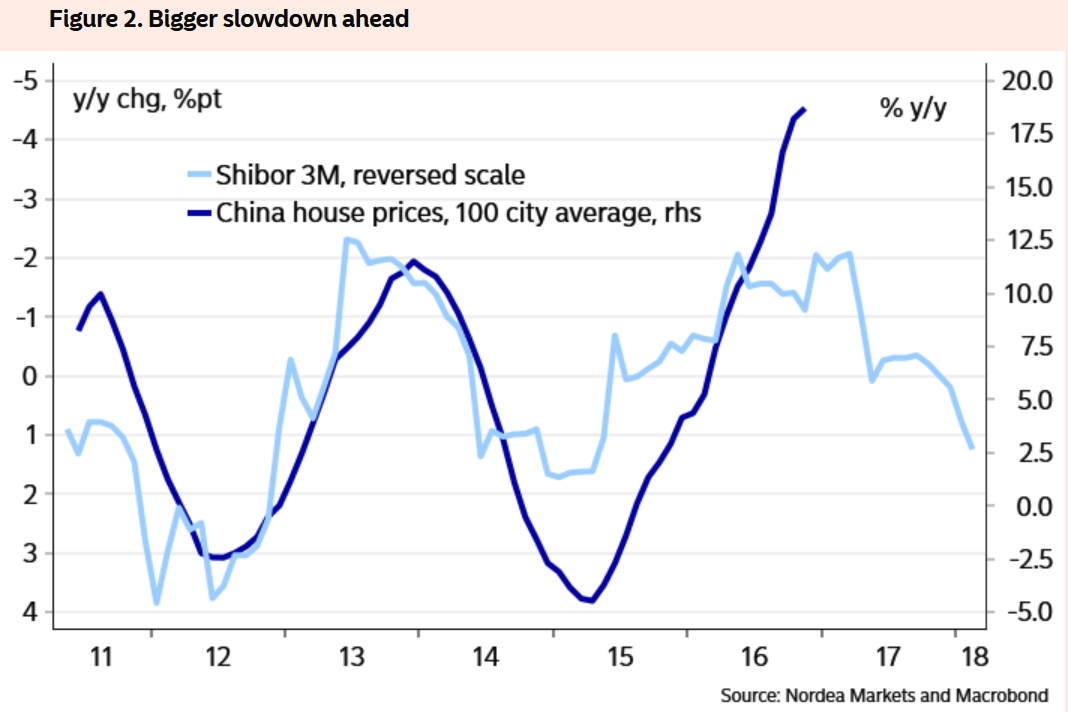

By end-2016, the nation’s debt to GDP ratio swelled to 270% from 150% in 2008 and the big problem with China now appears to the rising cost of borrowing.

Note the disturbing widening jaws of dislocation between House Prices in China and the increasingly expensive costs of borrowing, as measured by Shibor, or the Shanghai Interbank Offered (Lending) Rate:

The assumption is that the disconnect cannot go on for too long before the two snap shut to a closer correlation – the cost of borrowing will eventually start to limit demand for property, which in turn will impact on house prices.

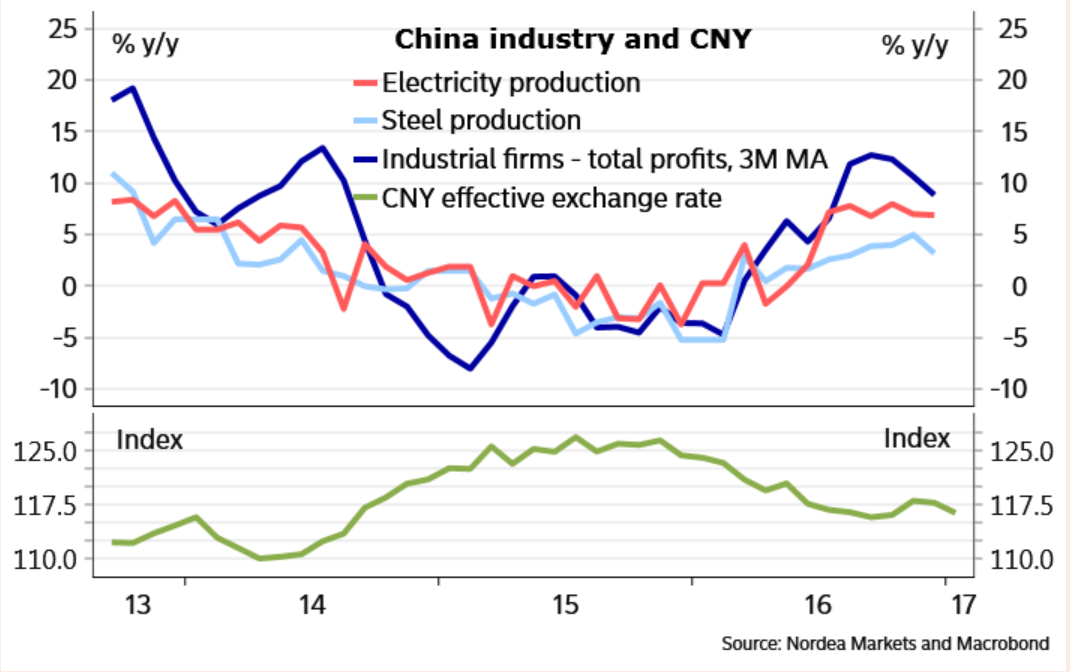

But the possibility of a property bubble popping is not the only reason Augulyte is cynical about China and the global reflation story, she also notes a softening in other key metrics, too, in particular the profits of Industrial firms.

The steady devaluation of the exchange rate is not helping matters as it has led to record outflows and the Peoples Bank of China (PboC) has responded by increasing interest rates in the hope of stemming outflows and retaining capital inside China.

But if the policy continues and interest rates continue to rise it will eventually probably cause a recessionary slowdown

To trim excessive leverage, PBoC started introducing more volatility into funding costs in 4Q16.

That, alongside rumours of defaults and expectations for faster US rate hikes triggered a selloff in the domestic bond market in December. The latest tightening has further impacted the bond market and pushed up the cost of borrowing.

Yields on 10-year treasury rose to 3.497% on February 6, the highest since August 2015.

"A major challenge for Beijing is how to contain leverage without turning the ongoing bond selloff into a broader market rout," says a note from DBS Group Research.

Lending Increases, Pushes up Iron Ore Prices

But while interest rates are rising, paradoxically so too is the amount of money being lent.

Incremental Total Social Financing (TSF) was RMB 3.74 Trillion in January.

"Think about that for a second… That is USD 545bn of new lending – in a single month," says Ben Powell at UBS in a note to clients dated February 17. "Even in China, this is a large number, around 5% of GDP."

Indeed it was the biggest single month of TSF growth ever.

"Given this backdrop, it perhaps isn’t surprising that iron ore prices are up 60% in 5 months," says Powell.

And recall, iron ore is Australia's prime export and therefore a key determinant of the value of the Aussie Dollar. Should the price of iron ore reverse we could see the support to the currency fade.

China the Cause of the Reflation Trade, Not Trump!

Powell and his team at UBS have come to an interesting conclusion when it comes to the reflation trade that characterised the latter half of 2016.

Most agree that it is the electoral victory of Donald Trump that is responsible. Not necessarily says Powell who believes following the money trail leads to some interesting conclusions.

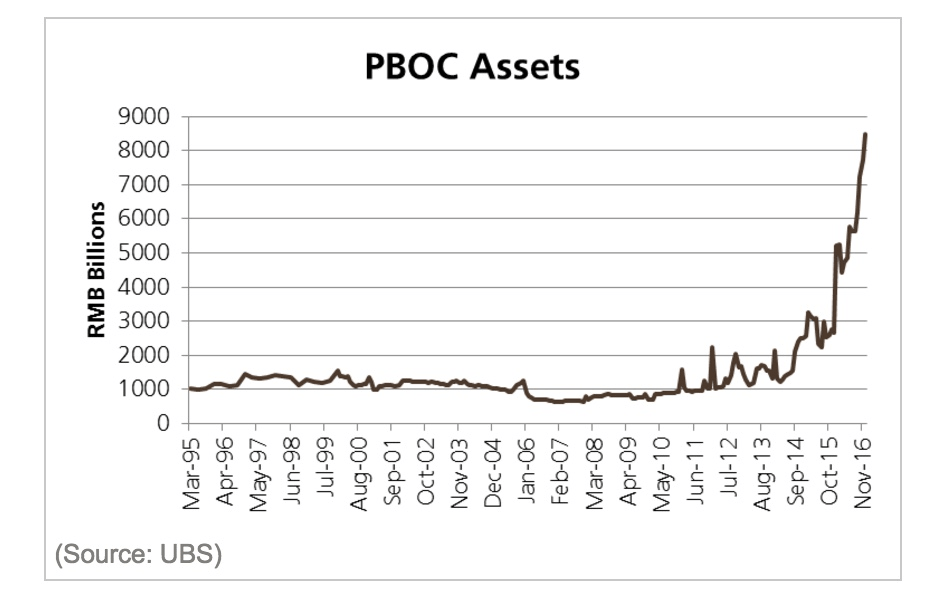

The above shows that the PBoC has been accumulating assets and therefore expanding the money supply to the economy.

"In 2014/15, it appears something changed, and a decision was made. Since then around a Trillion dollars of money has been printed and sent in the direction of the Chinese commercial banking sector," says Powell.

What changed? Powell notes:

Firstly the context. By 2015 QE had moved from the lunatic fringe to global mainstream orthodoxy.

Secondly, in China the SHIBOR spikes of 2013 perhaps led the authorities to decide that the market was failing to fund banks at socially harmonious rates of interest. So the PBoC got the call.

What does this all mean?

"At the global level I think it means that the world has misdiagnosed the reflation trade causes almost entirely. It has very little to do with the new US President. The reflation trade started to work in July of 2016. I would accept that the election of President Trump acted as a sentiment accelerant. But Trump wasn’t causal. The cause was the Chinese printing press," says Powell.

Australian, New Zealand Dollars in the Firing Line

As mentioned, Nordea's Augulyte believes there is a problem brewing as questions must surely be asked about the sustainability of China's increasingly debt-fuelled economic growth model.

SHIBOR is rising and so too is the vast amount of money being lent to the economy.

A sudden crisis in China would lead to a fall in risk appetite which would help safe-haven and funding currencies such as the Yen, the Swiss Franc and the Euro.

In contrast, emerging market currencies, the Rand and Asian currencies such as the Korean Wan would depreciate somewhat.

A slowdown in China, especially if it is centred on the property market, would hit the Australian Dollar very heavily.

Not only are a high (42%) proportion of Australian exports destined for the shores of China but they mostly consist of materials used in construction.

The other commodity currencies would also be hit, but not as much.

The New Zealand Dollar would depreciate but less than the Aussie as although it exports a high proportion of its goods to China too, they are generally of the soft variety, and include foodstuffs which are not as sensitive to a slowdown as building materials.

The right pair to speculate a March crisis in China with, therefore might be either the AUD/JPY cross or AUD/CHF.

Selling either of these would probably see the greatest return due to the two way volatility from rapid appreciation and depreciation at the same time.

But, UBS' Powell takes another view on the matter and says instead of avoiding the Aussie Dollar incase the Chiense bubble pops, investors should look to take advantage of further upside:

"In FX I think the simple thought is the right thought. AUD still looks cheap to me versus the positive terms of trade shock Australia has enjoyed in the past several months. I can't see any real need to complicate this. I would continue to buy AUDSGD which has worked year to date, and I think continues to work.

"Fade Trump / Buy China printing press."

Who is right, who is wrong? We can't say, but can say with certainty that the stakes are high.