- ZAR heads for fourth days of gains Vs USD et al

- But outlook marred by energy prices & Fed risks

- Could limit ZAR’s recovery as budget approaches

Image © Pound Sterling Live

- GBP/ZAR reference rates at publication:

- Spot: 20.24

- Bank transfer rates (indicative guide): 19.53-19.68

- Transfer specialist rates (indicative): 20.06-20.14

- Get a specialist rate quote, here

- Set up an exchange rate alert, here

The South African Rand pared away some of September’s losses in the opening week of October but a tightrope of risks still litters the currency’s path through the remainder of the month and could serve to limit its recovery over the coming weeks.

South Africa’s Rand remained the biggest faller among major developed and emerging market currencies in the month to Friday even as it headed for a fourth consecutive day of gains over the Dollar, Pound and other large as well as liquid currencies.

This is after a September storm in international markets lifted the USD/ZAR rate by around five percent, with developments in the U.S. economy, Federal Reserve policy and energy markets all playing a role.

Many of those factors will remain potential pitfalls through the remainder of October and in the period leading up to South Africa’s medium-term budget statement in early November, which is the next notable domestic risk event for the Rand.

“Marked upwards pressure on fuel prices is building for November which could lift CPI inflation to 5.3% y/y. Much will depend on the trajectory of the oil price, and that of the rand,” says Annabel Bishop, chief economist at Investec.

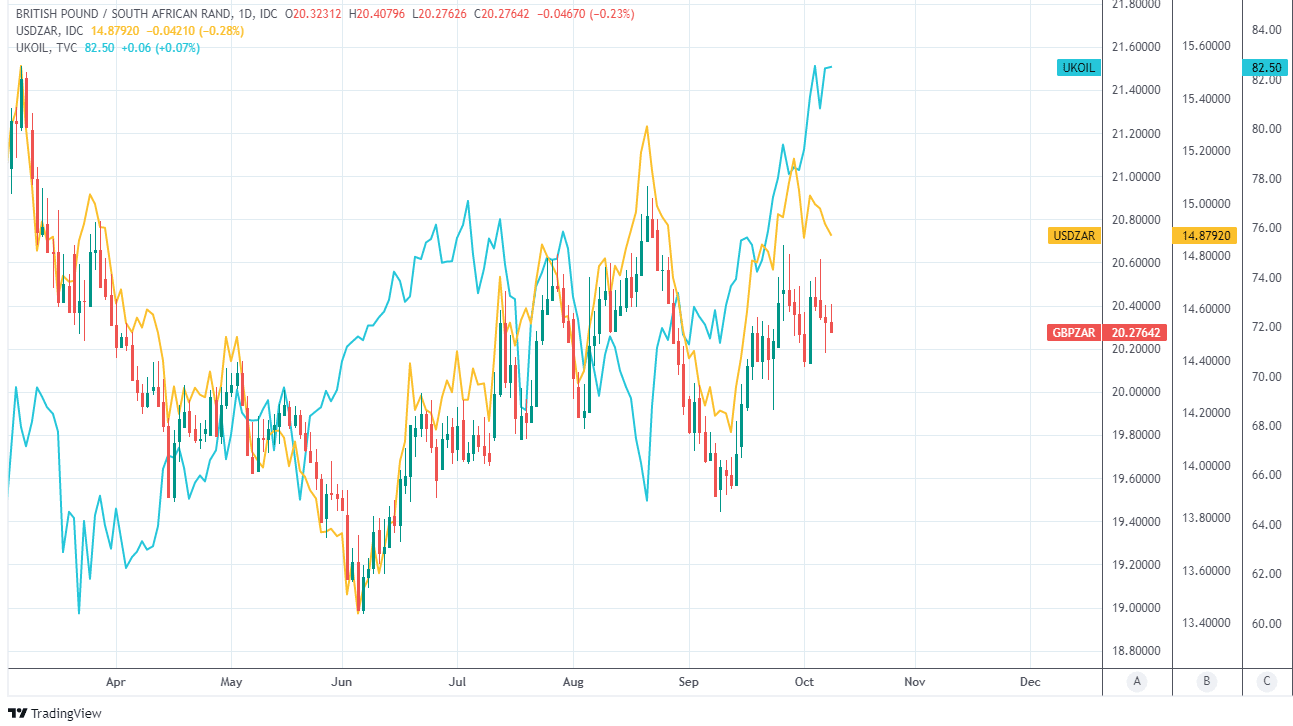

Above: Pound-to-Rand rate shown at daily intervals alongside USD/ZAR and Brent crude oil price.

Along the way, investors and analysts will keep one eye on the twists and turns of international energy prices, though most notably oil, which rose by a double-digit percentage in the month to October 08.

Rising oil prices directly affect domestic fuel costs, the rate of inflation and can have an adverse impact on economic growth, although these burdens are enhanced if and when price increases are large enough to inspire weakness in the Rand.

“Rand weakness has been one driver of high domestic fuel prices, and in turn higher fuel prices are a key driver of inflation in South Africa,” Investec’s Bishop told clients in a Thursday research note.

Oil prices have been buttressed in recent weeks by runaway natural gas prices, which have risen in response to deficiencies in European energy supply chains, with an additional tailwind from October’s Organization of Petroleum Exporting Countries’ decision not to further increase production levels.

Energy price gains have been lifting South African import costs just as recent strength in the Dollar has been weighing on prices of the commodities extracted and exported from South Africa, making for a negative influence on South Africa’s surpluses for internationally traded goods and capital flows.

These had been instrumental earlier this year in making the Rand the best performing currency on the market for 2021 and a possible erosion of them is one of many risks on the tightrope that the Rand could have to walk through the rest of October.

“A sharp correction lower in SA’s exporting commodities can have significant downside ramifications, especially if it comes amid higher oil prices," says Daria Parkhomenko, a strategist at RBC Capital Markets, in review of RBC’s forecasts.

"Additionally, if we enter an environment of consistently higher US bond yields and lower US equities, this would accelerate USD gains beyond even our current expectations, posing an upside risk to USD/ZAR," she adds.

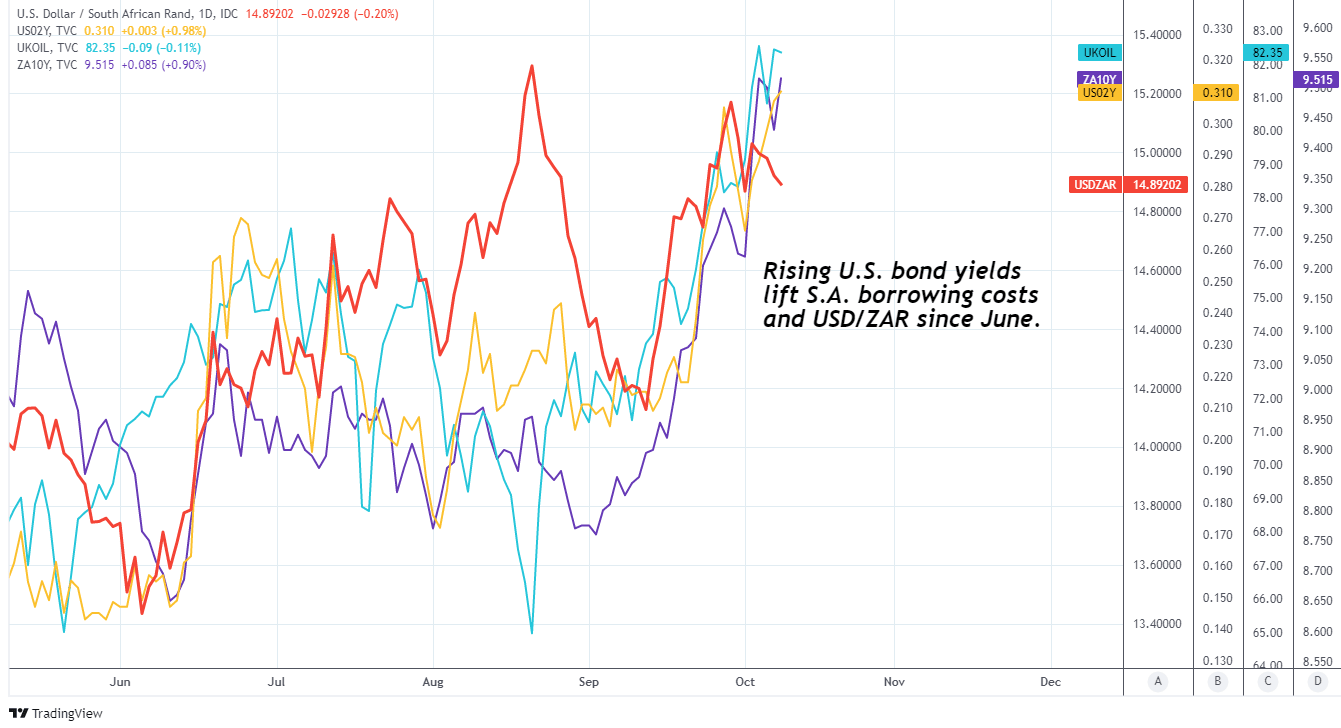

Energy prices could be an important determinant of the extent to which the Rand can recover from September’s losses in the weeks ahead, but price action captured in the below chart suggests the U.S. bond market may have been an equally powerful influence on the South African currency of late and this brings the Federal Reserve policy outlook into the picture.

Above: USD/ZAR shown at daily intervals alongside U.S. 02 year bond yield and South African 10-year bond yield.

While changes in energy costs and the Fed’s policy are not completely unrelated, the policy outlook is primarily a reflection of developments in the U.S. labour market and the prospects for inflation over the medium-term.

Both of which led the Fed to suggest in September that it could wind up its $120BN per month quantitative easing programme fully by the middle of 2022 and perhaps even lift interest rates late next year.

“ZAR is better insulated against external shocks vs. 2013 as external financing needs have been reduced by the [current account] surplus. However, ZAR depreciation during the past decade appears to be one reason why the [balance of payments] is not in worse shape,” says Greg Anderson, global head of FX strategy at BMO Capital Markets.

Anderson warned in early October that the Rand is likely to be among the most susceptible to any further increase in global bond yields that could materialise as a result of the Fed’s steady shift toward a normalisation of its interest rate settings.

This could come into sharper focus for investors through the remainder of October given the bank suggested last month that it could begin winding down the QE programme in November.

These will be prominent considerations for financial markets generally as new South African Finance Minister Enoch Godongwana prepares to deliver his first medium-term budget statement as minister in early November.

“In the medium-term, the focus is on fiscal consolidation and the implementation of pro-growth reforms, especially in the energy sector, with energy supply constraints an important hindrance for growth amid also high unemployment and the need for more investment,” RBC’s Parkhomenko says.