- ZAR tests July 2019 highs as Renminbi climbs to 3-yr highs

- But further CNH gains could whip up rising global tide Vs USD

- Lifting other currencies from Asia & Europe to Africa inc ZAR

Image © Adobe Images

- GBP/ZAR reference rates at publication:

- Spot: 19.61

- Bank transfer rates (indicative guide): 18.90-19.00

- Transfer specialist rates (indicative): 19.43-19.47

- Get a specialist rate quote, here

- Set up an exchange rate alert, here

The Rand tested new multi-year highs against the Dollar and weighed on GBP/ZAR this Tuesday as China’s Renminbi pushed USD/CNH to its lowest level since June 2018 in developments that could be indicative of further gains ahead for South African exchange rates.

South Africa’s Rand pushed the USD/ZAR exchange rate into a retest of the 13.80 level on the downside Tuesday, its lowest since July 2019, while weighing heavily on the Pound-to-Rand exchange rate in the process.

Rand gains came alongside building strength in the Euro and widespread weakness in Dollar exchange rates, with all building as and after the Renminbi pushed the USD/CNH exchange rate below the landmark 6.40 level which had previously and three times this year proved to be an insurmountable hurdle for the Chinese currency.

“China’s State Council said last week in its weekly meeting that China will work to ensure the supply of commodities and keep their prices stable. It has been the second consecutive week that China’s State Council flagged their concern about the recent rally of commodity prices,” says Tommy Xie, head of Greater China research at OCBC Bank in Singapore.

Above: GBP/ZAR, USD/ZAR, & USD/CNH falling together at hourly intervals.

There was no obvious catalyst for Tuesday’s move below 6.40, although it does come amid rising concern in Beijing about the impact that rising Dollar-denominated commodity prices are having on the production costs of Chinese firms.

It also follows hard on the heels of a suggestion last Friday by a senior researcher at the Peoples’ Bank of China (PBOC) that the bank’s State Administration of Foreign Exchange (SAFE) “appropriately appreciate the RMB” via a lower USD/CNH exchange rate in order to curb the impact that rising commodity prices have on firms and society at large.

“Let’s see whether USD/CNY can break under the 6.40/41 area over coming weeks (we do in general like a soft dollar environment this summer),” says Chris Turner, global head of markets and head of EMEA research at ING, in a resulting note to clients last Friday.

The Rand has always had a positive correlation with China’s Yuan, the currency of South Africa’s largest trade partner, although the relationship has strengthened this year with the Rand often rising alongside but further and faster than the Renminbi.

Above: USD/ZAR, GBP/ZAR & USD/CNH fall together beneath a key USD/ZAR trenrendline. ZAR/USD and CNH/USD also pictured.

As a result of this correlation any strength in the Renminbi tends to be a positive influence on the Rand anyhow, although it may also be highly pertinent here that current PBoC policy in relation to the Renminbi is to “maintain the basic stability of the RMB exchange rate at a reasonable and balanced level.”

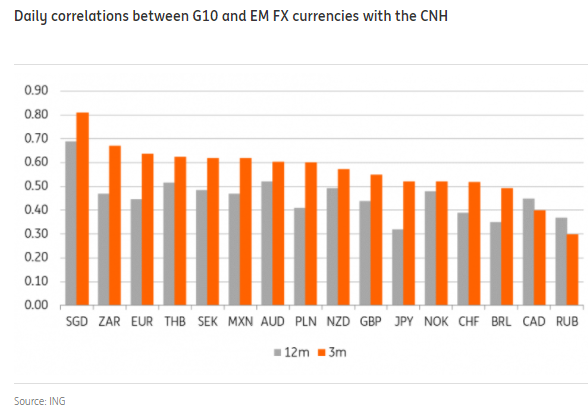

“Our chart [below] shows the highest correlations with the Singapore dollar – which is because the Monetary Authority of Singapore formally manages the SGD against a basket of currencies in which the CNY will have a large weight. The South African rand also pays quite a lot of attention to the path of USD/CNH,” ING’s Turner adds.

The PBoC’s exchange rate policy could have significant implications for the Rand and a range of other currencies and due to more than just correlation in the event of any decision to go ahead and “appropriately appreciate” the China-U.S. exchange rate.

Above: ING Group graph showing various currencies’ correlations with the Renminbi.

This is because any steep USD/CNH decline would lead the trade-weighted Yuan exchange rate to rise sharply, - that is the Renminbi measured against currencies of China’s major trade partners otherwise known as the China Foreign Exchange Trade System (CFETS) basket.

“The People's Bank of China has perfected a managed floating exchange rate system based on market supply and demand and adjusted with reference to a basket of currencies,” says Liu Guoqiang, Vice President of the PBoC, in response to media questions on Sunday.

“The People's Bank of China will focus on expected guidance, play the role of exchange rate adjustment macroeconomic and automatic balance of payments stabilizer, and maintain the basic stability of the RMB exchange rate at a reasonable and balanced level,” Guoqiang adds.

{wbamp-hide start}{wbamp-hide end}{wbamp-show start}{wbamp-show end}

The trade-weighted Yuan, or Renminbi measured against the CFETS basket, was already at three-year highs even before USD/CNH began to break below the 6.40 handle although this latter move would now lift other Renminbi exchange rates unless the PBoC takes action to stabilise or otherwise reduce them.

Achieving stability in the other Renminbi exchange rates - more so if an offsetting reduction in the other exchange rates is sought - would necessitate a PBoC bid for other components of the overall CFETs basket which covers currencies from Europe and Asia all the way to Africa including the South African Rand.

Encouraging other parts of the CFETS basket to outperform the Renminbi would in effect lead the Yuan to decline against those other currencies and in the process could help to keep the overall Renminbi stable “at a reasonable and balanced level.”

In other words it’s certainly very possible to say the least that the recent downturn in USD/ZAR and uptrend in South African exchange rates could find itself supported by a PBoC bid for the length of time that such a thing is mutually beneficial for the two economies concerned.

“It is also interesting to see the high correlation between the EUR and CNH. Yes, you may say that the PBoC is also managing the CNY against a basket of trading partners where the EUR has a large weight. But if we do see an independent move lower in USD/CNH as the market does the PBoC’s bidding of delivering a stronger currency to fight import prices – stable correlations suggest EUR/USD would be rallying at the same time. Such a move would support our end year EUR/USD forecast of 1.28,” ING’s Turner says.

Above: USD/ZAR at weekly intervals with Fibonacci retracements of 2018 uptrend, 2011 trendline and GBP/ZAR (blue), USD/CNH (green).