Despite the Dollar's September renaissance an amalgamation of current strategist forecasts and opinions makes grim reading for Dollar-bulls.

In fact, whether the timeframe in question is the short-, medium- or longer-term, the arguments around the greenback are decidedly bearish at present.

But it is the case for a more marked and longer-term depreciation that is the most compelling, which suggests that companies and consumers who have a long term requirement to buy the US currency could be quids in.

Short-Term: The Threat of Tax and Rate Disappointments Is High

The US Dollar has rebounded sharply during the last month after the Federal Reserve quashed fears it would abandon its push to keep raising interest rates and the Trump administration released plans for sweeping tax cuts and some reforms of the tax system.

“The odds of a December rate hike are now close to 80%, going into today's release of Fed Minutes for the 20 September meeting,” says Shahab Jalinoos, a strategist at Credit Suisse. “Nonetheless, we have made no changes to our bearish USD view versus EUR and most other major G10 currencies.”

With markets now pricing in almost as many interest rate hikes as is possible from the Fed over the coming quarters, at a time when the Fed leadership and the future composition of the rate setting panel is uncertain, the risk of market disappointment on US rates is high.

“The next key catalyst for the foreign exchange market will be the highly anticipated announcement of who President Trump will nominate to become the next Fed Chair,” says Lee Hardman, a currency analyst at Japan’s MUFG. “It has the potential to materially alter expectations for Fed policy in the coming years.”

President Trump will nominate his choice for Fed chair over the coming weeks although any changeover at the top will not actually take place until February when the incumbent Janet Yellen's term expires. There are a number of other vacant seat on the FOMC panel of US rate setters which are expected to be filled over the coming months.

Fed Chair Janet Yellen (Above). Source: Federal Reserve Gallery.

“The current combination of low inflation and Trump’s desire to boost growth should favour a continuation of gradual monetary tightening. As a result, it should remain difficult for the US Dollar to strengthen on a sustained basis,” says Hardman.

Donald Trump was elected on a Make-America-Great-Again ticket which, with the various geopolitical issues aside, leaves the current administration in Washington under pressure to drive an acceleration of US growth ahead of the next election.

Higher interest rates and a stronger US Dollar could pose substantial headwinds to accelerating growth, which means the White House is incentivised to use its influence over the composition of the FOMC to ensure a panel that may favour a slower pace of interest rate hikes.

For an overview of who the Fed Chair candidates are and an explainer of what each might mean for the Dollar, see our report; Change at the Fed: What Each of the Candidates Could Mean for the US Dollar's Outlook.

Meanwhile, the market remains sceptical of whether the mooted tax reform plan will have any lasting effect on the economy or on the Fed funds rate.

“Our view on the tax reform story as a USD driver was skeptical from the outset, as we saw both the lack of details and the crux of some of the ideas mentioned as problematic,” says Credit Suisse’s Jalinoos, a near-consensus view among economists.

Medium-Term: Portfolio Rebalancing Poses Downside Risks

The firming, albeit slow, economic recovery of the Euro area has propelled the common currency to the top of the G10 basket in 2017.

Concurrent with this recovery and ascent of the currency, investor perceptions of the relative risk attached to Euro area assets have softened, driving an influx of real money back into equity, fixed income and real asset markets on the continent.

“The FX market is undergoing a fundamental shift in drivers. It is no longer been driven by relative monetary policy expectations but an adjustment to flow imbalances that have built up through the implementation of highly unconventional global monetary policy,” writes George Saravelos, a strategist at Deutsche Bank, in a September note.

Unhedged portfolio flows out of American capital markets and into Euro area assets were as much a driver of the Euro’s 2017 appreciation as speculation the European Central Bank may soon begin to unwind its quantitative easing program.

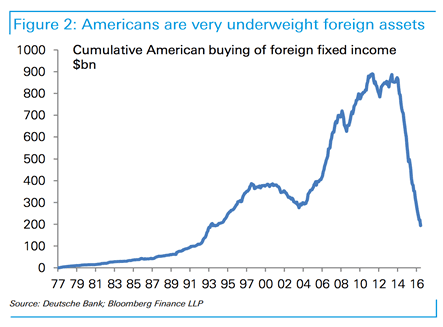

“Part of this imbalance is a structural underweight in European assets which we have written about in the past. More broadly however, Americans are hugely underweight in their investment allocations to the rest of the world,” says Saravelos.

The simple, if not inconvenient, fact is that American money managers have underweighted Euro area assets, as well as other assets, ever since the onset of the debt crisis.

And with this underweight now in reverse, there is scope for portfolio flows to place sustained downward pressure on the Dollar over the medium term.

For a detailed overview of the gargantuan shift in asset allocation that is now underway, see our report; US Dollar "in Trouble" say Deutsche Bank....Massive Global Asset Reallocation Underway.

Longer-Term: Central Bank Reserve Managers are the Biggest Risk

As if the short- and medium-term risks were not grim enough reading for Dollar bulls alone, the longer term outlook for the greenback is no less dire - or so it would seem according to the latest International Monetary Fund central bank reserves data.

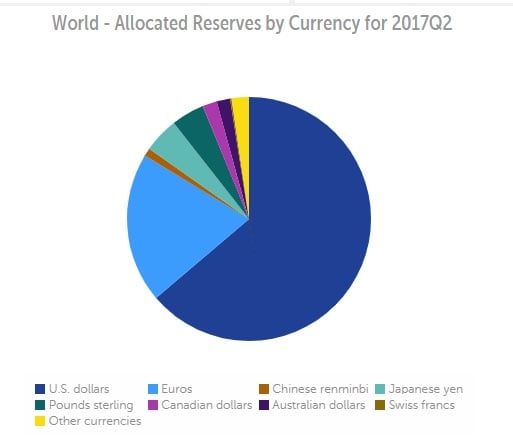

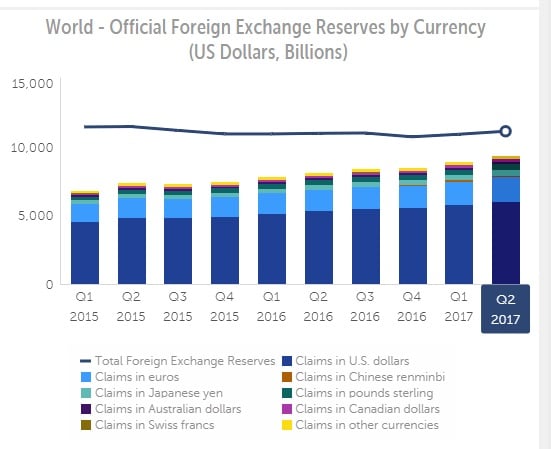

During the five years to 2015 the US Dollar’s share of global central bank foreign exchange reserves rose from 60% to 66%, a symptom of its reserve currency status and the perpetual state of crisis that gripped much of Europe and some other parts of the world.

In the first half of 2017, reserves managers bought more than $400 billion of the US currency but despite this, its overall share of global central bank reserves has declined to 63.8%.

“While the Dollar proportion has declined this year, the euro seems to be gaining new ground among global reserve managers,” says Richard Falkenhall, a macro strategist at Swedish bank Skandinaviska Enskilda Banken (SEB).

The drop in the greenback’s share of the reserves pie is as much a symptom of the evolving composition of the global economy as it is reserves managers becoming less sceptical of the Euro’s ability to see out the end of the year.

“Considering that US GDP today is roughly 25% of world GDP, we suspect that the proportion of dollar holdings among global reserve managers should continue to decline structurally in coming years,” says Falkenhall.

Another simple, if not inconvenient fact, is that for all its growth and continued might as an economic power, America’s relative share of the global pie faces precipitous shrinkage over the coming years as emerging markets such as China and India forge ahead with faster rates of growth.

“The proportion will probably fall below previous lows of around 60%, not least since the yuan is slowly becoming a more relevant alternative reserve currency,” Falkenhall adds.

For the sake of prudence, if not for any other reason, central bank reserves managers must keep pace with this evolution in composition of the global economy. By doing this, they may present themselves as a perennial source of downside risk for Dollar bulls.

“Therefore we expect that structural rebalancing flows out of the Dollar will remain a negative factor for the Dollar for years to come, just as they did prior to the financial crisis,” Falkenhall concludes.

None of this is good news for those piling into speculative US Dollar long positions. However, for companies, consumers and investors from across the UK and Europe who have a requirement to buy Dollars on an ongoing basis, it may be a welcome development.

Even if only to break the monotony of sifting through the noise around Brexit and continental European politics.