- GBP/USD awaits Fed policy update

- Markets wary of another 'hawkish' tilt

- But bar for such a tilt is set very high now

Image © Adobe Stock

The midweek Federal Reserve announcement will be critical in determining whether a recent slump in equity prices and appreciation in the Dollar can continue, or whether a near-term rebound for 'risk on' assets transpires.

For the Pound to Dollar exchange rate it will determine whether levels last seen in December are tested and if an extension of a medium-term downtrend commences in earnest.

With major global stock markets plummeting in early 2022 and the Dollar rising again it is apparent investors are keenly aware that this year the Fed will raise interest rates and reverse its quantitative easing programme.

The sheer scale of the fall in U.S. equities and crypto assets hints at just how seriously the issue is now seen by investors.

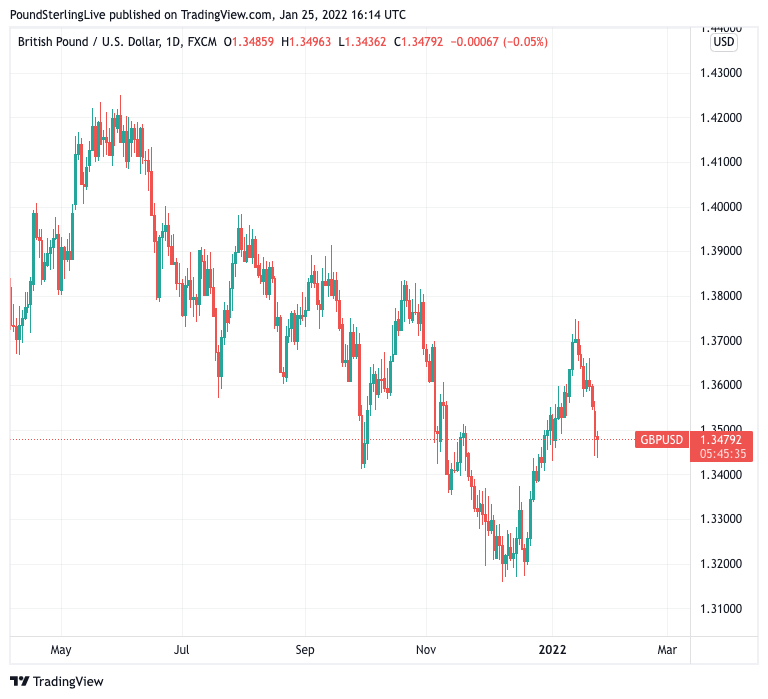

The Dollar has reengaged appreciation mode too with the Pound to Dollar rate falling back to 1.3437, erasing 2022's rally in the process.

Above: GBP/USD price action since May 2021 has favoured the Dollar.

- GBP/USD reference rates at publication:

Spot: 1.3507 - High street bank rates (indicative band): 1.3134-1.3230

- Payment specialist rates (indicative band): 1.3385-1.3439

- Find out about specialist rates and service, here

- Set up an exchange rate alert, here

Investors are now acutely aware that the days of easy money are over: the market presently expects the Fed to announce it will raise interest rates as soon as March with a an end to quantitative easing falling in the same month.

Quantitative tightening - whereby the Fed shrinks its balance sheet by selling bonds accumulated during quantitative easing - is anticipated to be engaged by the end of the year.

But just how much more hawkish can the Fed get? If the Fed communicates a desire to tighten conditions faster and further then the stock market sell off and Dollar appreciation can continue.

"There are some potential hawkish surprises that the FOMC could spring upon us," says John Velis, FX and Macro Strategist at BNY Mellon..

"One possible such move could be for the Fed to announce the end of its asset purchases as soon as February, rather than the currently expected March date," he says. "The communications from the central bank since the last FOMC have been both abundant and consistent, so much so that even this small tweak would be a major shock."

A hawkish surprise would pressure the Pound-Dollar rate lower towards levels last seen in December.

"We see risk for a further hawkish pivot," says Mark Cabana, Rates Strategist at Bank of America. "Chair Powell is likely to signal the first hike at the March meeting and note that every meeting is live".

For Bank of America a hawkish pivot could involve the acknowledgement by the Fed they have hit maximum employment, signal omicron is at least as much a supply as demand shock, suggest optimism about the growth outlook despite omicron, or note price pressures have continued for longer than expected and could still have room.

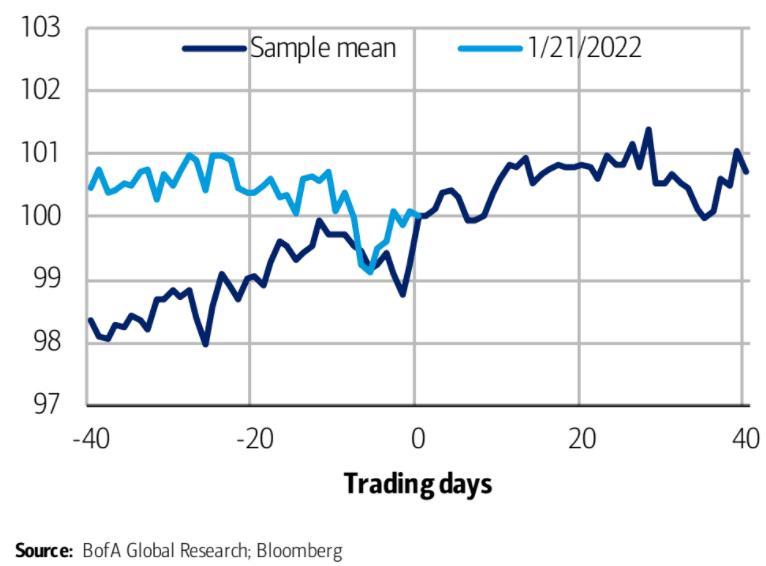

Bank of America are bullish on the Dollar as a result. Their analysis shows the dip in the Dollar in late-December to early-January is consistent with historical pattern approximately 40 trading days preceding the first Fed hike in a cycle.

Above: "DXY performance 40 days before a 1st Fed hike. USD a buy-on-dip into Fed liftoff" - BofA.

But the bar to an ever more hawkish Fed is surely now elevated given the speed of recent market moves, meaning the prospect of a relief rally in equities and a retreat in the Dollar is relatively high: the risk-reward ration might not favour chasing the hawkish Fed narrative much further from here in the short-term.

Velis says a hawkish surprise via announcing a February end to quantitative easing is unlikely.

"We think that at this point, it would be very much against character for the Fed to pull a surprise like that out of its hat," he says.

Bank of America meanwhile views as unlikely a "cold turkey taper stop" is called at this meeting, or a 50 basis point hike will follow in March.

If the market is heading into the announcement with frayed nerves then avoiding a 'hawkish-max' scenario could offer some relief.

Look for the Pound-Dollar exchange rate to rally if this is the case.

"It is also possible the Fed gives the markets a chance to catch its breath, especially if equity indices broadly enter correction territory heading into the meeting, but it may be a hard message to pull off," says BofA's Cabana.

"If Powell were to simply stay on message that could be enough to give the markets at least some temporary relief," says Derek Halpenny, Head of Research, Global Markets EMEA at MUFG.

{wbamp-hide start} {wbamp-hide end}{wbamp-show start}{wbamp-show end}

The minutes to the Fed's December meeting has proven to be something of a watermark for financial markets whereby stocks have fallen and Dollar weakness ultimately ended.

Released on January 06 the minutes indicated a Fed that was more hawkish than investors were expecting, resulting in up to four rate hikes being 'priced in' for 2022.

But it was talk of the need to engage quantitative tightening in coming Fed meetings that was of particular interest, given the topic was one that investors expected to come months following the commencement of the first rate hike.

Strategist Kenneth Broux at Société Générale says the Fed can't afford to dither as this would surely harm it's inflation-fighting credibility.

"Looking back at how events unfolded in 2015, after the first hike in December of that year it took until the second week of February before stocks hit their nadir. The 13% correction in the S&P back then will probably end up being smaller than today, for the simple reason that the liquidity-fuelled overshoot was significantly higher this time," says Broux.

The signal is clear: this is a central bank greatly concerned with rising inflation and markets must prepare for a world of diminishing 'easy money' availability.

And for the Dollar this is supportive over the medium-term.