Image © Adobe Stock

What a difference a week can make: when we published our previous week ahead forecast last Monday, the Pound to New Zealand Dollar setup was distinctly bearish.

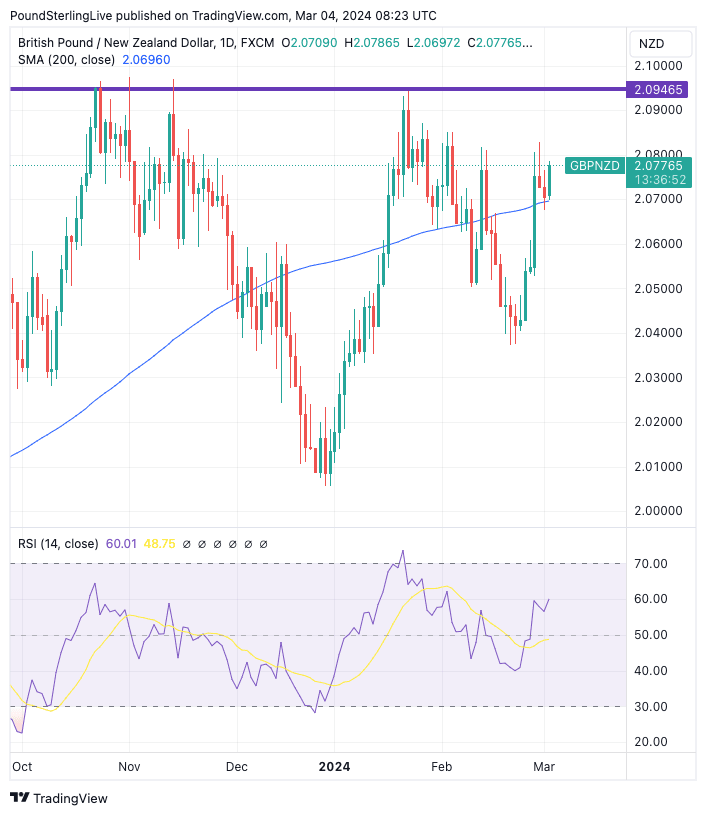

Now, the opposite is true with the exchange rate having broken above a whole host of short- to medium-term moving averages.

We did warn in last week's publication that the NZD was facing a 'make or break' week, and the subsequent developments and price action vindicated this prediction as the Kiwi fell flat on its face after the Reserve Bank of New Zealand (RBNZ) kept interest rates unchanged. This disappointed a large portion of the market on alert for another rate hike or strong guidance that another hike was likely.

Above: GBPNZD at daily intervals. Track GBP/NZD with your own custom rate alerts. Set Up Here

The Pound to New Zealand Dollar's 1.35% gain to 2.0709 takes it back above the nine-day simple daily moving average, which suggests the near-term picture is constructive at the start of the new week. But last week's gain also saw the pair break through the 50-, 100- and 200-day DMAs, which amounts to a suite of constructive developments.

Support for this coming week is now seen at the 200 DMA at 2.0696 (blue line in the chart).

A test of the 2024 high at 2.0946 (which marks the approximate highs of the October-November 2023 rallies) is favoured owing to the broadly supportive technical setup.

Downside risks emanating from New Zealand are limited owing to the clear event calendar, which means global factors will be important.

This is a big week for global markets as the U.S. jobs report lands on Friday. For context, the market has pushed back expectations for a Federal Reserve rate cut owing to the strong U.S. economy, and Friday's report could provide further evidence that cuts are not needed.

This pushback against rate cuts has tended to weigh on the NZ dollar in 2024, as this currency tends to underperform when U.S. and global bond yields are rising (rising bond yields reflect fading expectations for a rate cut and raise the cost of money, acting as a handbrake to global growth).

Another strong U.S. jobs report could reinvigorate this setup and trigger further NZD weakness. (See our USD week ahead report for a preview of what to expect from the payrolls report).

"The market came into 2023 expecting a recession. The reality is that the US economy is simply not slowing down, and the Fed pivot has provided a strong tailwind to growth since December," says Torsten Sløk, Chief Economist at Apollo Global Management

"As a result, the Fed will not cut rates this year, and rates are going to stay higher for longer," he warns.

Track GBP/NZD with your own custom rate alerts. Set Up Here

A potential trigger for GBP moves would be Wednesday's UK budget announcement, the only event worth speaking of on the UK calendar.

We reported recently that if Chancellor Jeremy Hunt gets the March 06 budget wrong, the Pound could fall by as much as 2%, but analysts say the Pound would find some positives if a credible fiscal easing is announced.

Furthermore, any efforts to boost UK productivity, such as business investment tax breaks, can also result in a stronger Pound.

The big risk for the Pound is if the Chancellor announces big tax cuts deemed unaffordable by bond market players, as was the case with Liz Truss' botched budget of September 2022.

ING estimates a 40 basis point risk premium in 10-year gilt yields, "suggesting markets aren't totally immune to UK fiscal risk".

"Were Chancellor Hunt to misread the mood of gilt investors and cause another upset, sterling would again come under pressure," says Chris Turner, Global Head of Markets at ING. "Short-term models suggest a 2% sell-off in sterling could happen quite easily were investors again to demand a risk premium of sterling asset markets."