Above: RBNZ Governor Adrian Orr. File image of previous RBNZ statement and press conference © Pound Sterling, Still Courtesy of RBNZ

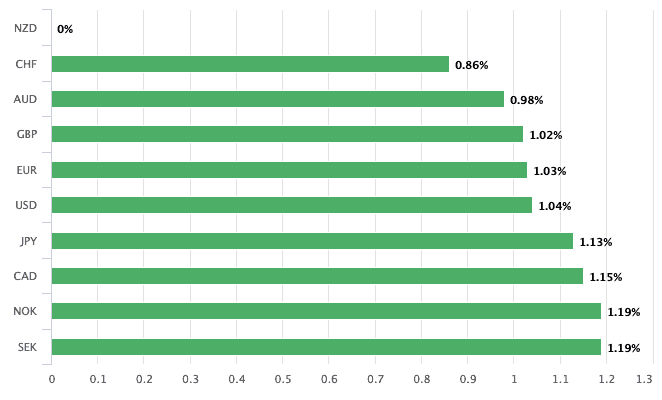

- NZD outperforms peers

- RBNZ signals 50/50 chance of further rate cuts

- Markets convinced themselves a rate cut was coming today

- However, a 2020 rate cut highly likely

- Expect NZD gains to be limited say analysts

The New Zealand Dollar outperformed its peers on global currency markets in mid-week trade after the Reserve Bank of New Zealand (RBNZ) surprised markets by opting to leave interest rates unchanged.

There had been a growing expectation in markets, and amongst analysts, that the RBNZ was due to cut the basic interest rate in New Zealand from 1.0% to 0.75%. However, it appears that the market and analysts have been found guilty of talking themselves into believing such an outcome was set in stone.

"Markets were shocked, but we are less surprised," says Dominick Stephens, an analyst with Westpac. "But we recognised that it would be a close call."

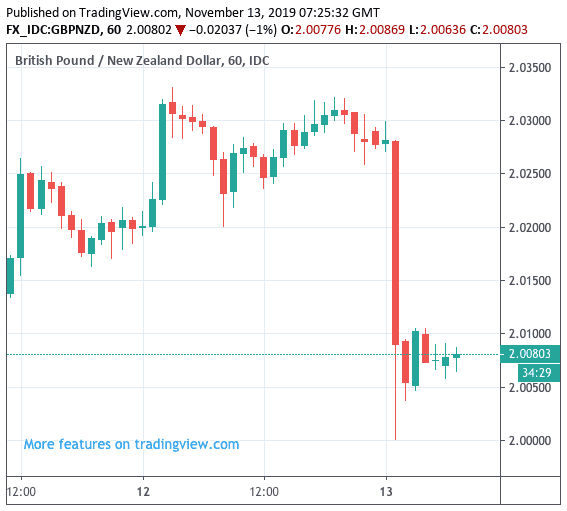

The Pound-to-New Zealand Dollar exchange rate has fallen a full percentage point to trade at 2.007 on the back of the NZ Dollar's rally. Currencies tend to embark on sizeable moves when hit by an element of surprise, and today's decision by the RBNZ certainly counts as that.

The New Zealand-to-U.S. Dollar exchange rate has risen by a similar amount to trade at 0.6401. "We could see this NZD/USD rally extend towards 0.6450 if there are further rates positions to unwind," says a note from JP Morgan's London institutional FX sales desk. "However, when you look at what happened in May where the message was ‘one and done’ and then they cut 50bps three months later, this doesn’t change my medium term sell rallies approach in this currency."

Above: The NZD is outperforming its major peers in the wake of the RBNZ decision to keep interest rates unchanged.

The RBNZ kept the OCR on hold at 1.00%, although the final sentence of the press release said: "We will add further monetary stimulus if needed."

The RBNZ’s OCR forecast reached a trough of 0.9%, which implies that it thinks there is a 50/50 chance that it will have to reduce the OCR again at some point.

"Financial markets were shocked, but we are less surprised. In October we pointed out that the RBNZ had never signalled a November cut, and the information available up to that time did not justify a change in stance. At that time, we predicted that the RBNZ would leave the OCR on hold and issue a 0.9% OCR forecast," says Westpac's Stephens.

The RBNZ hinted that the decision was a close one, saying the Monetary Policy Committee (MPC) debated the costs and benefits of cutting or remaining on hold, noting that "both actions were broadly consistent with the current OCR projection."

Analysts at ASB in Aukland say the RBNZ’s growth outlook remains on the optimistic side, and it has yet to factor in the economic impact of its looming bank capital increases.

ASB had been expecting an interest rate cut, and are still expect the RBNZ will eventually need to cut the OCR twice further in 2020, and still expect a 0.5% low.

"Moreover, the RBNZ has yet to factor in the economic impact of its impending bank capital increases, for which we expect a bigger economic impact than the RBNZ," says Nick Tuffley, Chief Economist at ASB.

Tuffley says the RBNZ could have taken a different tactical path today and cut anyway, particularly given that the risks will remain tilted towards the need for a lower OCR at some stage. A cut would at least have kept interest rates anchored low.

"In contrast, the market has pushed wholesale interest rates substantially higher in the immediate aftermath of the decision. To put things into context, the 2-year swap rate is now 1.23% and it was 1.25% before the RBNZ’s surprise 50bp OCR cut back in August. From a low of 0.82%, the 2-year rate (and the entire interest rate curve) have ground higher as global optimism around trade tensions and Brexit has improved. But around half of that rates rebound has occurred in response to the RBNZ’s OCR decision," says Tuffley.

In short, the RBNZ's decision to not cut rates has actually had the adverse effect of tightening monetary conditions in New Zealand, which could well weigh on growth going forward.

The reaction of the New Zealand Dollar will also unlikely be welcomed, as a strengthening currency tends to add a dampening effect on demand for New Zealand exports.

"The RBNZ now enters a 3-month decision-making hiatus. That hiatus starts with wholesale interest rates up markedly, with the risk that mortgage rates start to lift (and fuel FOMO) just as the seasonal spring upswing in housing activity hits its straps. Crucially, a lot of mortgage rate re-fixing will be happening in coming months. The associated balance sheet risk management of that re-fixing will in itself put upward pressure on wholesale swap rates, compounding the recent wholesale market pressures. Keeping the OCR on hold is not without its risks," says Tuffley.

It appears that the RBNZ might have given itself reason to cut interest rates in 2020, and therefore any strength in the New Zealand Dollar might not be sustained as markets start to gradually price such an eventuality once more.

"Despite the strong rebound following the decision, kiwi gains should be limited as the RBNZ appears to base its decision on too optimistic fundaments while uncertainties over the completion and timing of a US – China phase-one trade deal is still questioned," says Vincent Mivelaz, an analyst with Swissquote Bank, adding:

"There is therefore good reasons to consider that a deterioration of current economic conditions should force the RBNZ to cut rates by 2 February 2020 monetary policy meeting latest. In this context, we see potential for further NZD appreciation as scarce for the time being."

Time to move your money? Get 3-5% more currency than your bank would offer by using the services of a specialist foreign exchange specialist. A payments provider can deliver you an exchange rate closer to the real market rate than your bank would, thereby saving you substantial quantities of currency. Find out more here.

* Advertisement