- Barclays says GBP to be supported

- But the best part of the rally is done

- Could mean GBP/EUR highs are in

- NatWest says economic outlook bodes well for Sterling

Image © Adobe Images

The British Pound should be "underpinned" in the short-term by expectations for further UK interest rate hikes say analysts at two of the UK's most recognisable banks, although they disagree on how much stronger the Euro can get following last week's European Central Bank pivot.

The views therefore pose differing paths for the Pound to Euro exchange rate; with NatWest Markets saying the pair can go higher while analysts at Barclays see downside in 2022.

Eimear Daly, a FX & EM Macro Strategist at Barclays, says the Bank of England's commitment to "the primacy of price stability in the UK" means the Pound should remain supported on real interest rate differentials.

The Pound rallied to its highest level against the Euro in two years last week after the Bank of England hiked interest rates 25 basis points, although those gains were soon erased by the cautious guidance regarding the UK economic outlook delivered by Governor Andrew Bailey.

The decision caused rates markets to price in an additional 16bp of tightening over the next 12 months, this after the Bank revealed the Monetary Policy Committee was a mere single vote away from raising rates by a more substantive 50 basis points, according to Barclays.

"Two of the dissenters were previously considered doves, underlining broadening inflation concern within the committee. However, the economic projections showed slowing domestic growth and the tough policy choices the Bank faces," says Daly.

"Its clear determination to hike rates to contain inflation and the fact that it has arguably over-delivered at its last two meetings should keep rate expectations elevated and sterling underpinned," she adds.

- Reference rates at publication:

GBP to EUR: 1.1844 - High street bank rates (indicative): 1.1530 - 1.1612

- Payment specialist rates (indicative: 1.1740 - 1.1785

- Find out more about specialist rates and service, here

- Set up an exchange rate alert, here

Barclays now forecast for the Bank to hike 25bp back-to-back in both March and May, before pausing with the Bank Rate at 1%.

Daly does however caution that Pound Sterling "has come a long way since the start of Q4-2021" and as such "the extent of recent GBP appreciation and the negative economic backdrop against which the BoE is tightening means sterling's gains are likely to be limited."

Barclays forecast the Pound to appreciate against the Dollar, targeting 1.37 by mid-2022 but they forecast underperformance against the Euro, holding a mid-2022 EUR/GBP target of 0.86.

This gives a GBP/EUR point forecast of 1.1630.

Paul Robson, Head of G10 FX Strategy, EMEA, at NatWest Markets says there’s "more to Sterling than monetary policy" and this should offer protection against the Bank of England story becoming stale.

NatWest describes the Bank's February decision as a "hawkish hike" and see risks of an additional hike as early as March.

Economists believe guidance points to a front loading of tightening to limit that amplitude of the policy cycle.

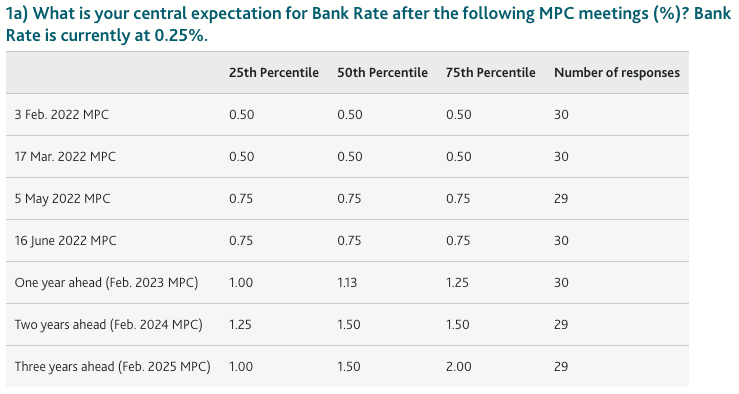

Above: The Bank of England's Market Participants Survey results for February 2022.

A concern for some foreign exchange market participants is that the Bank's hiking cycle is now fully accounted for, and "in the price" of the currency, therefore should any disappointment against expectations could result in weakness.

"The monetary policy cycle in the UK has become a lot more fully priced, and additional Sterling gains look increasingly like they’ll have to be driven by equity flows," says Robson.

Economic performance could therefore be key.

"A few things were lost in the excitement on Thursday, not least the upward revisions to the January UK PMIs that hint that there was a decent pick-up in activity in the last week of January. The government also announced a package of fiscal measures to lean against the cost of living rise," says Robson.

He notes travel restrictions have also been removed in recent weeks and this will further help the parts of the economy that remain the hardest hit by the pandemic.

"This all bodes well for the economic outlook, and therefore Sterling," says Robson.

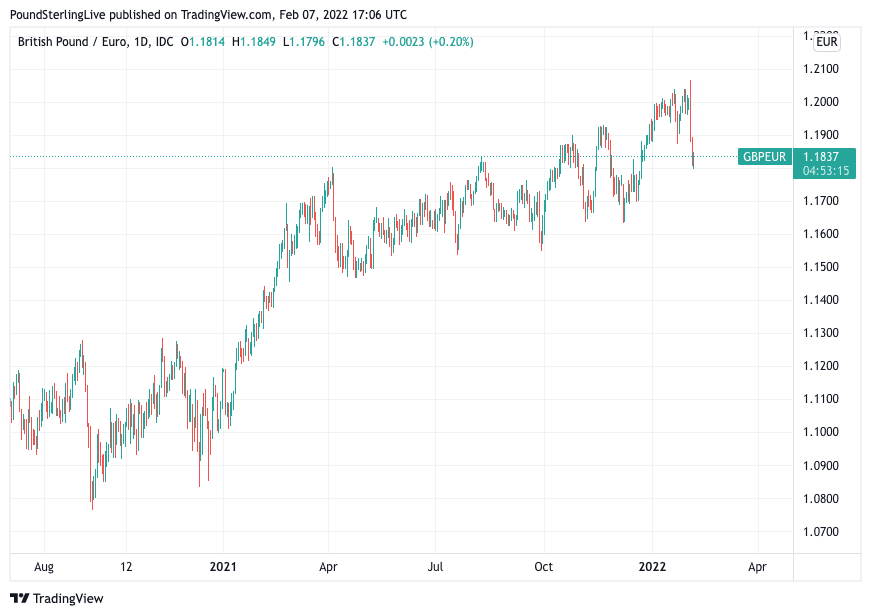

Above: GBP/EUR has been trending higher since September 2020.

But for the Pound-Euro exchange rate much of course depends on the European side of the equation, particularly as it relates to the European Central Bank (ECB).

The ECB lit a fire under Euro exchange rates last week when it dropped guidance saying there would be no interest rate rise in 2022, ultimately validating market pricing for at least one 25 basis point hike by December.

The ECB also said all members of the governing council were now concerned about the trajectory of Eurozone inflation, underpinning a view that the ECB would fall in line with other central banks to begin tightening monetary policy.

But strategists at NatWest Markets argue that it could be with regards to the ECB where the market is pricing in too many hikes.

For rates to be hiked in 2022 - the market now expects two hikes - the tapering of quantitative easing will have to accelerated says Robson, given that ECB President Christine Lagarde is adamant that the sequencing (QE, then rates) will be respected.

She also emphasised at the February policy meeting the "gradual" path of tightening.

"With the ECB still buying ~30bn gross per week, getting to zero 6m would be stretching gradual. It suggests that front-end rates are pricing in much too much. As such, we believe it’s too early to call time on EUR weakness vs the USD and Sterling," says Robson.

{wbamp-hide start} {wbamp-hide end}{wbamp-show start}{wbamp-show end}

In response to the ECB decision Barclays has revised its ECB forecast, calling for a March announcement of a faster tapering of asset purchase and 25bp rate hikes in both March and September 2023.

Markets now ultimately expect the ECB to hike and tighten monetary policy with a much smaller lag to the U.S. Federal Reserve and Bank of England.

For the Euro, such a dynamic is supportive.

"The ECB's shift from monetary policy divergence to monetary policy convergence is significant and the EUR faces a grind higher over the coming weeks as the FX markets adjust," says Daly.

Barclays hold a EUR/USD forecast of 1.19 by end-2019, expecting FX markets to adjust to the prospect of higher eurozone rates.

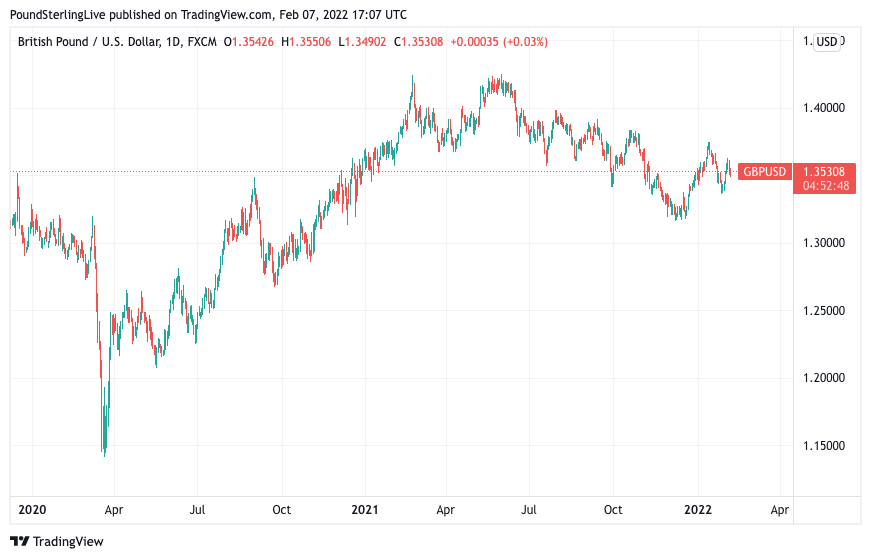

Above: GBP/USD has been trending lower since April 2021.

Should EUR/USD rise faster than GBP/USD rises then it stands the GBP/EUR would fall.

NatWest's Paul Robson says although the Euro has benefited from the ECB's hawkish pivot, it is questionable as to how much further this story can run.

"While the EUR was a clear beneficiary, particularly against the USD, we think the prospect for markets to price more / sooner tightening from here still favours USD and GBP over EUR," says Robson.

NatWest say in a weekly currency briefing they see the Euro's rally soon "fizzling" out.

Money markets showed investors were pricing in a 25bp hike by the ECB ahead of last week's monetary policy update.

Since the meeting the market is now pricing in 50bp, i.e. two increases.

Is it reasonable to expect the traditionally ultra-dovish ECB to end its quantitative easing programme in short enough order as to pave the way for two interest rate hikes in 2022?

The ECB's March policy meeting should provide the answers, but it does seem that there is a now a lot priced into the Euro and this could at least limit some near-term upside.