- EUR/USD could enjoy short-term relief on French politics

- ECB policy decision also a potential cushion for EUR/USD

- Recovery road shortened by risk of further U.S. yield rally

- As U.S. inflation risks driving a more aggressive Fed pivot

Image © European Central Bank, reproduced under CC licensing.

The Euro to Dollar exchange rate entered the new week close to multi-year lows but French political developments and European Central Bank (ECB) policy could offer a partial offset over the coming days for what is likely to become an increasingly burdensome Federal Reserve (Fed) policy outlook.

Europe’s single currency was one of the biggest fallers from early on last week when market anxiety about the sanctions response to allegations of Russian atrocities in Ukraine weighed most heavily on continental currencies, although it could find itself better supported in the week ahead.

This is after exit polls released following a first round vote in the French presidential election appeared to give a clear lead to the incumbent ahead of the April 24 second round, and in anticipation of a potentially supportive Thursday policy decision from the European Central Bank (ECB).

“As before the probabilities still point to a Macron win but the available data concerning net positioning in EURUSD on the part of leveraged funds do not suggest FX investors were anticipating a vastly different result,” says Stephen Gallo, European head of FX strategy at BMO Capital Markets.

“We continue to think that elevated uncertainty in general is reducing investor participation in EURUSD despite the fact that EUR appreciation is being held back by its trade flow fundamental and relative interest rate changes,” Gallo also said in a note on Sunday.

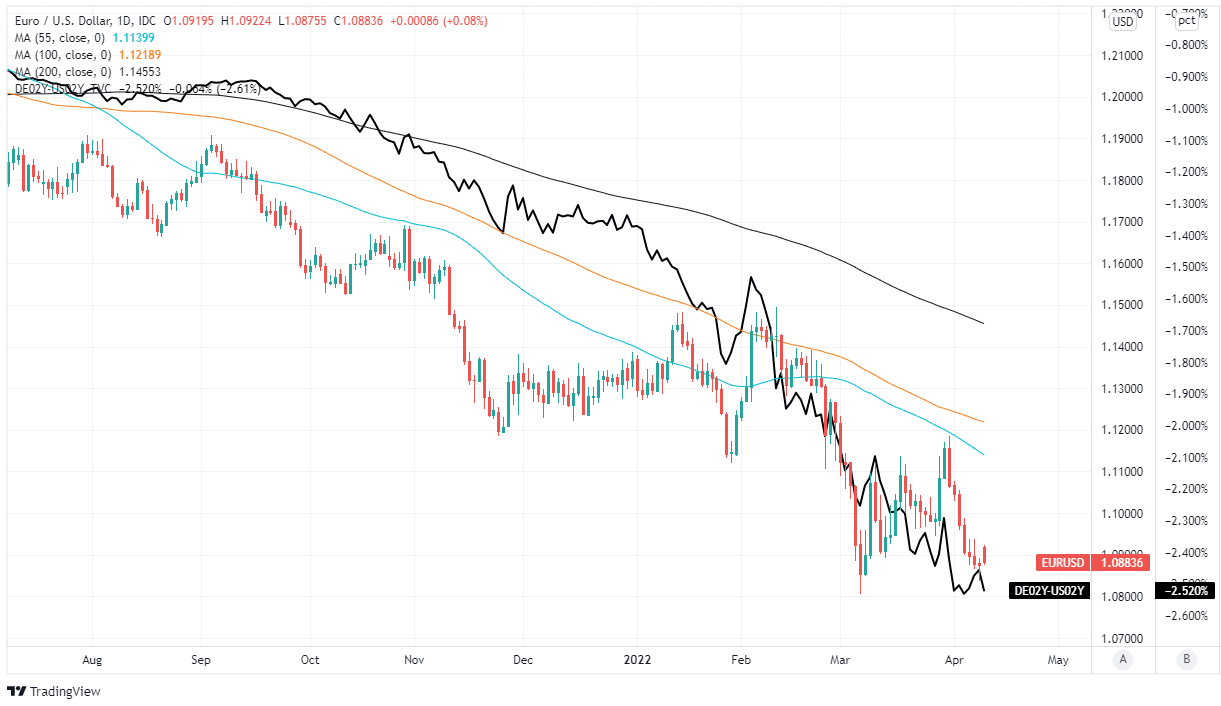

Above: Euro to Dollar rate shown at daily intervals alongside spread - or gap - between - 02-year German and U.S. government bond yields. Includes selected moving-averages.

Uncertainty about the April 24 outcome of the French election had been widely cited as a risk facing the Euro last week and to the extent that this held back the currency’s performance it could be in for some relief over the coming days.

Such relief might be more likely in relation to the likes of the safe-haven Swiss Franc than the U.S. Dollar, however, given that this Tuesday will herald the release of March inflation data and the Fed is becoming increasingly willing to respond to rising price pressures by raising interest rates.

“We expect EUR/USD to consolidate following last week’s weakness. The mid-March low of 1.0806 is likely to be tested in coming weeks. The pandemic of low point of 1.0688 is within reach too,” says Joseph Capurso, head of international economics at Commonwealth Bank of Australia. (Set your EUR/USD exchange rate alert here).

“The ECB is in a difficult place because high energy prices cut disposable income and economic growth. This is in contrast to the US FOMC, where the job of tackling very high inflation is the main focus against the backdrop of a strong economy and a tight labour market,” Capurso also said on Monday.

Like many other U.S.-facing exchange rates, the Euro-Dollar rate has been under mounting pressure in recent weeks with the Federal Reserve having made increasingly clear that U.S. policymakers could yet move faster than even financial markets have been willing to give credit for.

This scenario would become more likely on Tuesday if it transpires that U.S. inflation pressures built further last month, which might be likely to constrain any rebound in EUR/USD ahead of Thursday’s all-important European Central Bank monetary policy decision.

“Inflation is now seen as more persistent rather than transient and markets have been repricing potential ECB policy into next week’s meeting,” says Tim Riddell, a London-based macro strategist at Westpac.

“The sharp slide from tests of 1.1175 leaves EUR/USD vulnerable to a retest of 1.0800 or even towards 1.0650, unless it can close back above 1.1050,” Riddell and colleagues also wrote in a research briefing on Friday.

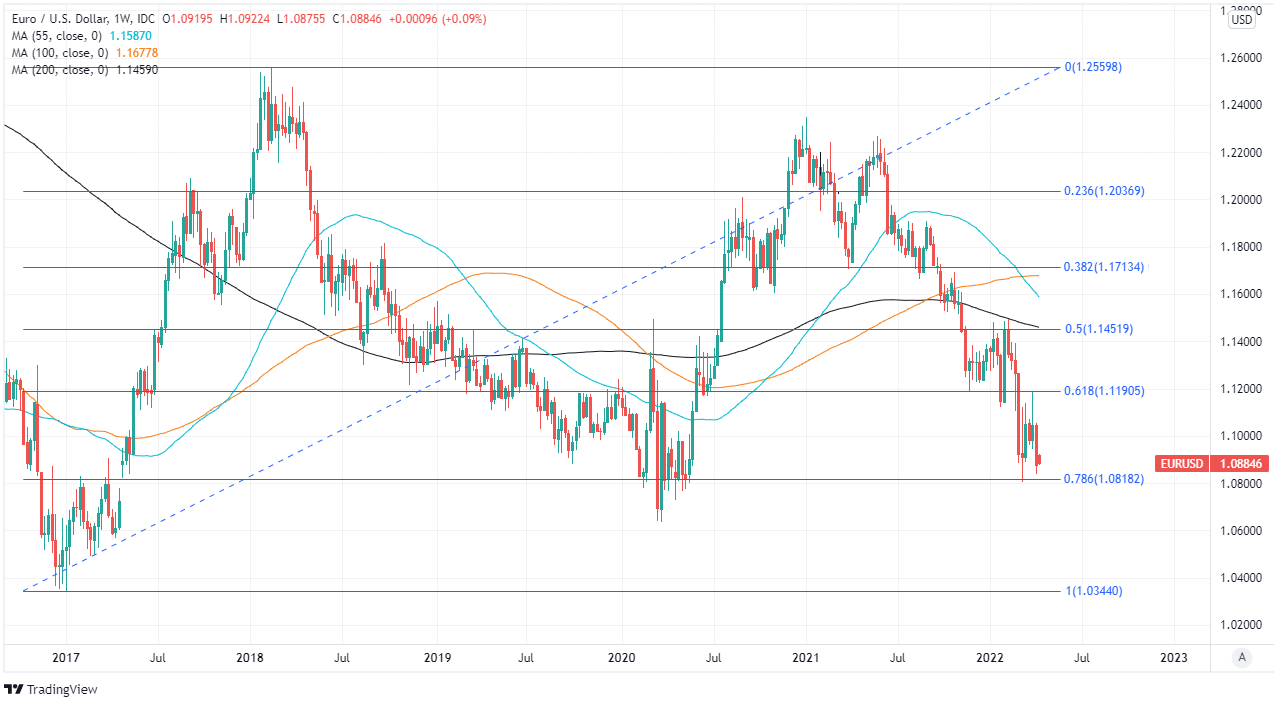

Above: Euro to Dollar rate at weekly intervals with Fibonacci retracements of 2017 rally indicating possible medium-term areas of technical support for Euro and shown alongside selected moving-averages. Click image for closer inspection. Click image for closer inspection.

Minutes of the ECB’s March policy meeting confirmed that, for the time being at least, the bank has all but secured a sustainable medium-term attainment of its long elusive two percent annual inflation target.

This is facilitating a sooner than otherwise end to the bank’s two different quantitative easing programmes and could even see Frankfurt’s negative and near-zero interest rates lifted at some stage in the near future, which would mark the end of an era for European monetary policy.

“The money market remains more hawkish than economists. The Bloomberg survey of economists points to a 25 bps rate hike from the ECB in December 2022 and further progressive tightening through 2023,” says Jane Foley, head of FX strategy at Rabobank.

“Our 3 month forecast of EUR/USD1.10 assumes that Macron keeps the presidency in France and that growth sustains in the Eurozone this year leaving market expectations for an ECB rate hike around year end intact,” Foley said following a review of the outlook for the Euro last week.

The ECB ended its near-€2 trillion Pandemic Emergency Purchase Programme (PEPP) last month and announced at the March meeting that a temporary increase in the size of Frankfurt’s original Asset Purchase Programme (APP) would be scaled back faster than previously planned.

While the ECB hasn’t actually committed to any kind of “normalisation” at all, the bank has manoeuvred itself into a position where its practice of quantitative easing could be ended at any point after June this year and has not ruled out a change in its interest rate settings for the near future.