- EUR/USD consolidates ahead of next big move

- Analysts say downside most likely

- As Eurozone hit by gas price instability

- And rapidly declining consumer confidence

Image © Adobe Images

The Euro to Dollar exchange rate is expected to remain under pressure by analysts who say Russia's demand for gas payments to be made in Rubles underscores the prospect for further gas price rises.

Surging gas prices are meanwhile reflecting in a deterioration in Eurozone consumer confidence that warns of a slowdown in economic activity over coming months, which could invariably weigh further on the bloc's single currency.

"Russia can drive up the price of energy and hurt the EU economy badly, even if it continues to supply gas. I would therefore think that with each new sanction, the risk of an energy price shock increases, which, as we have explained many times, would hit the EU economy and thus the euro harder," Antje Praefcke, FX and EM Analyst at Commerzbank.

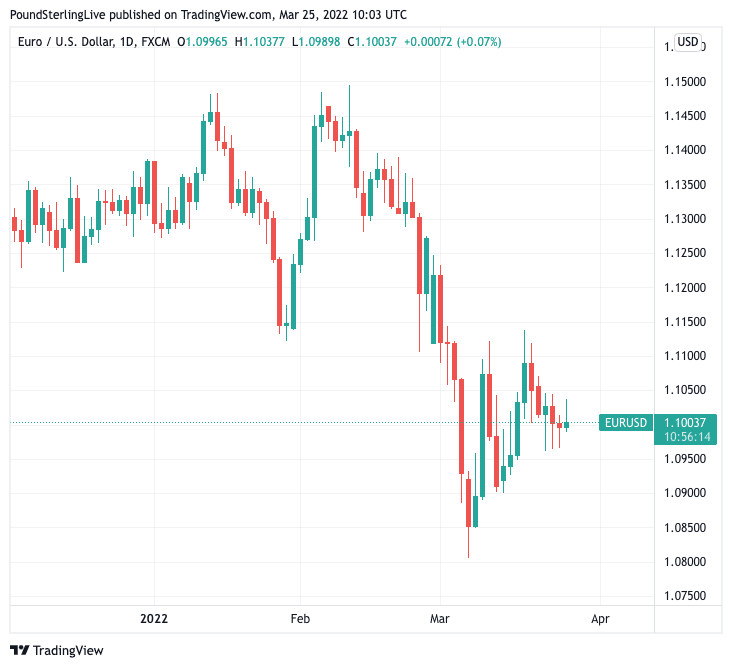

The Euro to Dollar exchange rate (EUR/USD) is seen consolidating in the region of 1.10 at present, having been as low as 1.0806 on March 07 but as high as 1.1137 on March 17.

The consolidation implies a market that is awaiting fresh information before making another sizeable directional move.

"In my view, the risks remain on the downside for the euro for now," says Praefcke.

Above: EUR/USD daily chart showing near-term consolidation, but with the larger trend remaining to the downside.

- EUR/USD reference rates at publication:

- Spot: 1.1005

- High street bank rates (indicative band): 1.0620-1.0697

- Payment specialist rates (indicative band): 1.0906-1.0950

- Find out more about market-beating rates and service, here

- Set up an exchange rate alert, here

Praefcke says Putin's announcement that in the future only ruble payments will be allowed for exports of Russian gas to "unfriendly" states was surprising.

Her colleague at Commerzbank, Ulrich Leuchtmann, says in a research note out this week Putin still command a significant influence on European gas prices.

The sanctioning of Russian entities by Western nations means previous long-term supply contracts - that offer a form of price stability in the market - must invariably be replaced.

"The supply contracts that can now no longer be honored must be rewritten. It depends on which RUB amounts are used to replace the EUR amounts previously noted in the contracts," says Leuchtmann.

European importers, who were previously protected from the rise in gas prices by means of longer-term supply contracts, could find themselves exposed to worsening conditions.

"No wonder that the gas price increased significantly," says Leuchtmann. "Russia is not (yet) turning off the gas tap. But it could significantly increase the price we pay for it."

{wbamp-hide start} {wbamp-hide end}{wbamp-show start}{wbamp-show end}

Eurozone PMI's for March showed the Eurozone economy continued to recover at a decent clip but forward looking aspects of the survey showed significant headwinds ahead.

S&P Global - compilers of the PMI data - summed up the situation facing the Eurozone as such: "Eurozone growth slows, exports fall, business sentiment slumps and prices rise at record rates as Russia invades Ukraine.

Business sentiment as tracked by the PMI's future output expectations index fell in March to its lowest since October 2020.

"Eurozone PMIs fell more moderately than expected in March but the underlying trends were worse than the headlines suggested," says Aline Schuiling, Senior Economist for the Eurozone at ABN AMRO.

"The escalation of the Russia-Ukraine conflict and the related energy and other commodity supply shocks, has clearly hit the eurozone economy," she adds.

Additional data out Thursday shows Eurozone consumer confidence dropped by almost 10 points in March (to -18.7, down from -8.8 in February) and fell almost to the low point that was registered during the first wave of the pandemic.

The details of the consumer confidence survey have not yet been published, but Schuiling says it is likely the assessment of (future) economic conditions and households’ financial situation plummeted, while the expected labour market conditions probably also deteriorated.

ABN AMRO expects soaring energy prices to result in only moderate consumption growth in the first half of this year, despite the post-lockdown rebound in services consumption.

Schuiling's colleague Georgette Boele, Senior FX Strategist at ABN AMRO, says she maintains a view the Euro will continue to extend lower against the Dollar in 2022.

Boele had predicted the Euro was on course to fall to parity against the Dollar in 2022, but has since acknowledged recent developments make this target too low.

"We reviewed our base case scenario and indicated that EUR/USD could drop to parity on safe haven buying for the US dollar. Since then, a lot has changed, and investor sentiment has improved as well," she says.

In a 'fine tuning' of their expectations for global markets ABN AMRO says they now expect investor sentiment to be "cautious as opposed to negative", and as a result now think that there is less upside for the dollar versus the euro.

But central bank policy expectations meanwhile argue for further Dollar strength says ABN AMRO as the Federal Reserve will still outpace the European Central Bank in the hiking stakes.

Boele finds financial markets now expect a total of 185 basis points of rate hikes by the Fed and 40 basis points of rate hikes by the ECB.

"This is more than we have forecast for the Fed and the ECB. The repricing to our views could weigh on both the US dollar and the euro. But the widening rate spread should still support the dollar versus the euro," says Boele.

"We are still positive on the US dollar versus the euro, but we see less upside than the parity we indicated a few weeks ago. Our new year-end forecast for EUR/USD is 1.05," she adds.