Above: File image of Jerome Powell. Source: Federal Reserve.

Federal Reserve Chair Jerome Powell sent a lighting rod through financial markets on the final day of November when he said he no longer expects inflation to be temporary.

His view that inflation will be a stubborn feature of the coming year is a 'hawkish' turn that stands to benefit the Dollar going forward, meaning December could spell more losses for the Euro-Dollar exchange rate.

Powell told U.S. lawmakers Covid-19 outbreaks are inflationary and that it is time to "retire" the word transitory and that the Fed can consider ending QE bond buying "a few months" earlier.

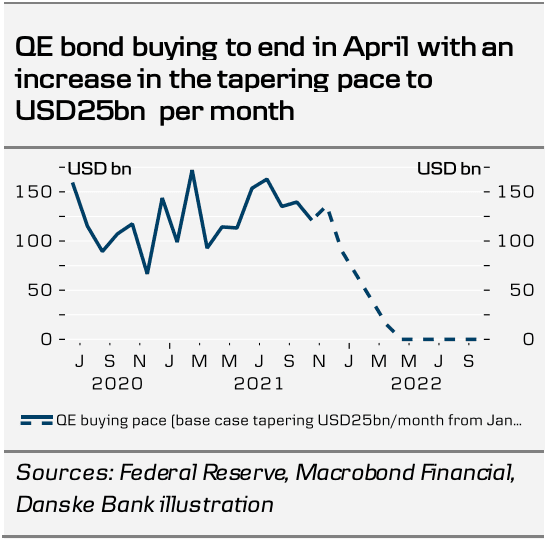

"We now expect the Fed to increase the tapering pace from $15BN per month to $25BN so that the tapering is concluded in April," says Mikael Olai Milhøj, Chief Analyst at Danske Bank.

Danske Bank now expect three 25bp rate hikes in 2022 in June, September and December. By

ending quantitative easing bond buying in April, the door is open for the first rate hike in May. They still expect four rate hikes in 2023.

"Being long dollar will remain an integral part of that cross asset rotation. Thus, we recommend selling the rally in EUR/USD," says Lars Merklin," Senior Analyst at Danske.

Image courtesy of Danske Bank.

- EUR/USD reference rates at publication:

Spot: 1.1328 - High street bank rates (indicative band): 1.0930-1.1011

- Payment specialist rates (indicative band): 1.1226-1.1270

- Find out about specialist rates, here

- Set up an exchange rate alert, here

- Book your ideal rate, here

The Euro has staged a recovery against the Dollar over the course of the past week but some analysts are of the view any rebound is likely to be temporary and there is more Dollar dominance to come.

The Euro to Dollar exchange rate rose to a high of 1.1383 on November 30, having bene as low as 1.1186 on November 24, with market fears over the Omicron variant helping to unwind some investor positioning.

But the sense is that the Dollar's retreat is more a symptom of markets paring back on popular trades: i.e. being long the Dollar and short the Euro.

Foreign exchange analysts at Commerzbank have lowered their Euro-Dollar exchange rate forecasts, saying the Federal Reserve will raise interest rates in 2022 in an environment of falling inflation.

This would imply materially higher U.S. 'real' yields relative to the Eurozone.

"The Fed should seem more hawkish next year than the market is currently assuming," says Ulrich Leuchtmann, Head of FX and Commodity Research at Commerzbank.

"We therefore consider the rate hikes we are expecting to be USD-positive and think that the dollar is likely to trend firmer next year," says Leuchtmann.

Commerzbank in November lowered their Euro-Dollar forecasts and now see levels below 1.10 as possible.

Ima Sammani, FX Market Analyst at Monex, says the current pressures on the Euro are likely to extend into December.

"We have downgraded our EURUSD forecasts," says Sammani, "we have downgraded our EURUSD forecast over the whole horizon to account for the risk of more aggressive Fed normalisation in 2022."

{wbamp-hide start} {wbamp-hide end}{wbamp-show start}{wbamp-show end}

Sammani says during November markets became increasingly sceptical that the current elevated prices in the U.S. are transitory and continued to push back on the Fed’s mantra that price increases will fade.

This mantra was all but abandoned on November 30 when U.S. Federal Reserve Chair Jerome Powell dropped his guidance that inflation was transitory.

He said the Fed would need to consider accelerating the withdrawal of its quantitative easing programme (tapering) at its December meeting, a move that would invite interest rate hikes to come forward in 2022.

Stocks fell and the Dollar rose on the back of the developments.

Monex forecast EUR/USD at 1.11 by the end of 2021, 1.12 by February 2022 and 1.14 by the end of May.

Sammani says the Euro is also likely to be hampered by slowing growth rates as the region grapples with surging Covid cases and high fuel prices.

"Beyond the current pressures on the euro that are likely to extend into December, year-end flows into the dollar and the recent blowout in cross currency swaps is another

reason we are bearish on EURUSD towards year-end," says Sammani.

Monex do however see levels below 1.10 as being unlikely under current circumstances and think EUR/USD needs a more hawkish Fed to break meaningfully below the 1.11 handle.

"With expectations for the Fed’s December meeting being high and market bets being aggressive already, the Fed is more likely than not to disappoint relative to current pricing, which makes us believe 1.10 is a stretch at present," says Sammani.

Asmara Jamaleh, an economist with Intesa Sanpaolo, the Italian lender, says the comparison between the prospected evolution of Fed and ECB monetary policies will be the main driver of the EUR/USD exchange rate in the near-term.

"The Fed is rather clearly letting on that it is increasingly concerned by upside risks to inflation, and the market," says Jamaleh.

By contrast the ECB is has been keen to convey over recent weeks is that rates will

not be hiked next year, as euro area inflation will drop in the course of 2021 from its current peaks, considered temporary.

Jameleh is however cautious on forecasting too great a decline in the Euro, saying that much is already in the price and a recovery is likely in 2022.

"Due to the size of the correction already observed of late, as the market is already pricing in an early start to the Fed’s rate hike cycle, and the ECB is expected to revise upwards its inflation forecasts in December," says the analyst.

"In the course of next year the euro is expected to start rising back gradually, in function of the progressive reduction of the distance between the ECB and the Fed, that will be at its greatest in the near term," he adds.

The Euro to Dollar exchange rate is forecast at 1.12 in one-month, 1.14 in three months, 1.18 in six months and 1.21 in twelve months by Intesa Sanpaolo.