- EUR/USD sags amid widespread USD declines post-ECB

- New guidance confirms an age of zero rates looms in EZ

- After strategy review lifts long-undershot inflation target

- EZ recovery seen "on track" with risks "broadly balanced"

Above: President Lagarde. Photo: Martin Lamberts/ECB.

- EUR/USD reference rates at publication:

- Spot: 1.1790

- Bank transfers (indicative guide): 1.1377-1.1460

- Money transfer specialist rates (indicative): 1.1684-1.1707

- More information on securing specialist rates, here

- Set up an exchange rate alert, here

The Euro-Dollar rate saw only a tepid rebound on Thursday as the Euro lagged other comparable currencies in capitalising on widespread declines by the Dollar following new ‘dovish’ guidance from the European Central Bank (ECB), which confirmed that an age of near-zero interest rates continues to loom over the path ahead for the Eurozone.

Almost nobody will have been surprised on Thursday when the ECB said its main interest rate, marginal lending rate and commercial bank deposit rate were left unchanged at 0%, 0.25% and -0.50% respectively this month, and bond purchases under its €1.85 trillion Pandemic Emergency Purchase Programme are set to continue at their recently increased weekly pace alongside those of the original €20bn per month Asset Purchase Programme.

But Frankfurt did appear to temper appetite for the Euro when unveiling new guidance for borrowing costs, which are now likely to remain at historically low levels for close to an age as the bank pursues a new and recently-increased inflation target.

“In our view, the implication of this new guidance is consistent with a much more prolonged period of policy accommodation than currently priced in by financial markets,” says Nick Kounis, head of financial markets research at ABN Amro.

The bank said Eurozone interest rates will remain near zero until the Governing Council “sees inflation reaching two per cent well ahead of the end of its projection horizon and durably for the rest of the projection horizon, and it judges that realised progress in underlying inflation is sufficiently advanced to be consistent with inflation stabilising at two per cent over the medium term.”

“No one expected the ECB to raise rates anytime soon, but this new CPI target and associated forward guidance has pushed out the first deposit rate hike even further in our view,” says Claus Vistesen, chief Eurozone economist at Pantheon Macroeconomics. “Elsewhere, and as widely expected, the ECB is sticking with the message on QE.”

The ECB also warned that its new guidance “may also imply a transitory period in which inflation is moderately above target,” which comes after policymakers recently agreed to lift their inflation target from an ambiguous “below but close to 2%,” to a rounded and symmetric 2%.

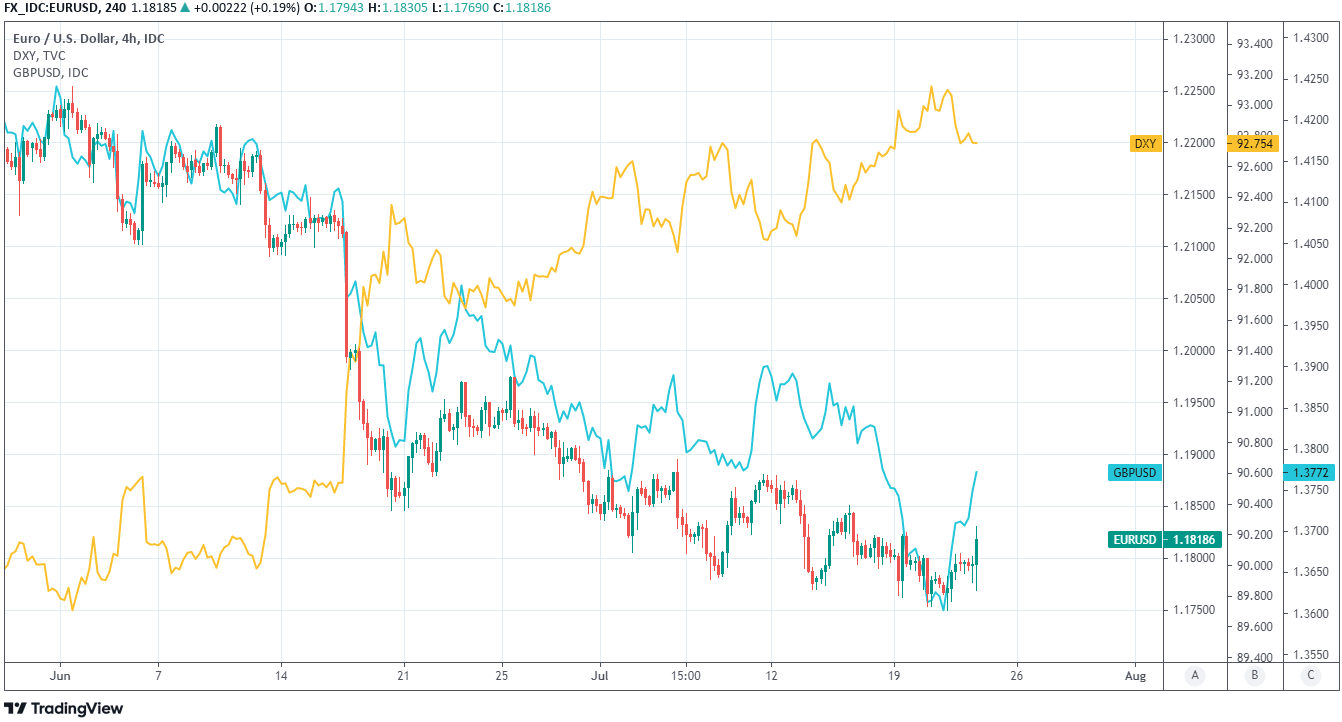

Above: Euro-Dollar rate at 4-hour intervals with GBP/USD and U.S. Dollar Index.

The ECB’s inflation target was raised following a strategic review, despite it not having met the earlier and lower target for more than a fleeting moment in the last decade, and means the bank will have to continue supporting the Eurozone economy with zero interest rates and other policy tools such as quantitative easing for even longer than the already-lengthy period that was anticipated by the market previously.

“The recovery in the euro area economy is on track. More and more people are getting vaccinated, and lockdown restrictions have been eased in most euro area countries. But the pandemic continues to cast a shadow,” President Christine Lagarde told a press conference following the decision.

“We see the risks to the economic outlook as broadly balanced,” Lagarde later said.

{wbamp-hide start} {wbamp-hide end}{wbamp-show start}{wbamp-show end}

Euro-Dollar was choppy around the 1.18 level following the announcement and press conference from President Christine Lagarde, and although it carried an intraday gain by the time the press conference was over, the Euro was still lower against most counterparts in the G10 segment of the major currency space.

The few exceptions to the Euro trend were against currencies like the Japanese Yen and Swiss Franc, whose central banks have had equal if-not greater difficulty than the ECB in meeting inflation targets, in a trading session where most currencies were lifted by a relenting U.S. Dollar that fell almost across the board on Thursday following a week of almost unbroken gains.

“The Meeting reinforces the ECB’s position as one of the most dovish central banks, which points to EUR weakness against high-beta currencies should global risk sentiment return, and a dovish ECB also should help broader sentiment at the margin,” says Rui Ding, content lead at CitiFX Wire.

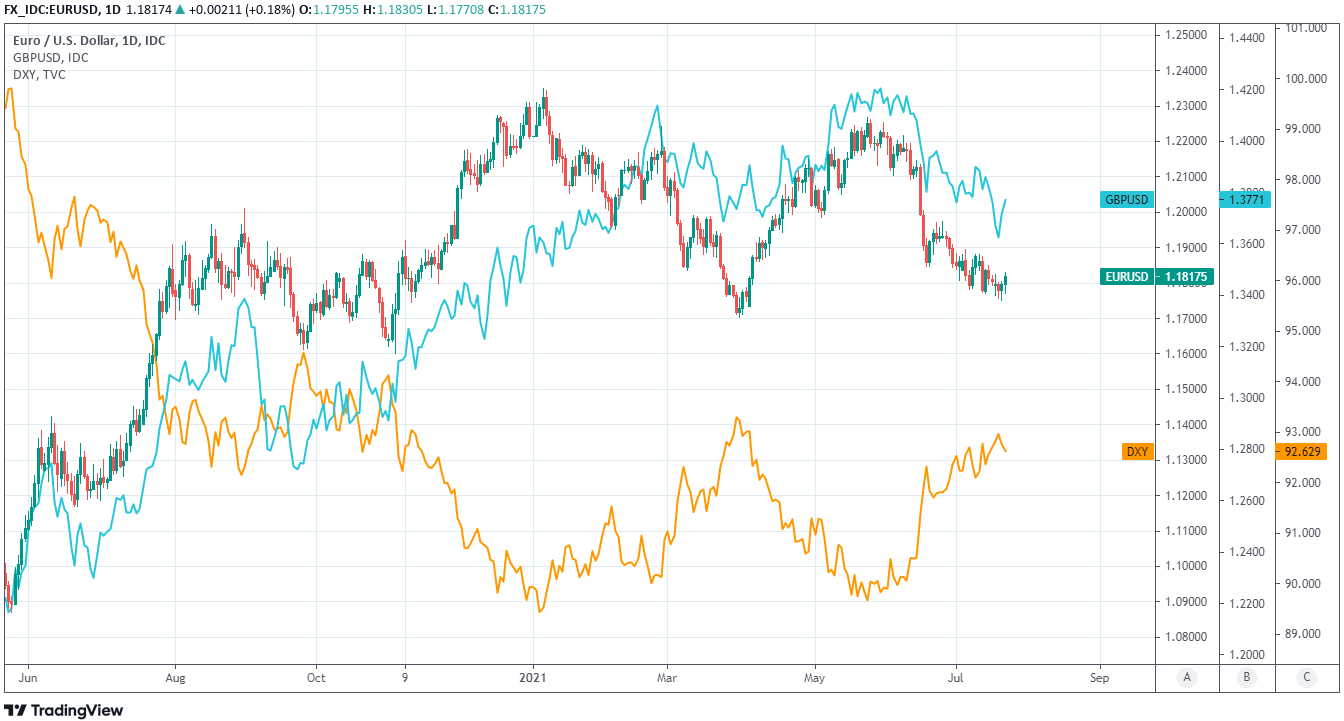

Above: Euro-Dollar rate at daily intervals alongside GBP/USD and U.S. Dollar Index.

“Short term resistance on the topside comes in between 1.1790 and 1.1805 whilst slightly long term resistance can be found at 1.1825,1.1850 and 1.1880/1.1895 all of which have proved hard to break given the recent risk off tone and resulting USD demand,” Ding says in summary of a note from Citi research analysts.

The ECB sets interest rates and the parameters of its quantitative easing programmes with the aim of influencing economic supply and demand in order to lift inflation to predefined target levels, though has struggled to reach its objectives in over the last decade, a period in which many Eurozone economies have been hamstrung by debt and spending rules enforced from Brussels.

Thursday’s guidance is a dampening headwind for the Euro-Dollar exchange rate, which has been weighed down in recent months by a host of international factors including a June indication by the Federal Reserve (Fed) that it could be willing to lift U.S. interest rates from their current near-zero level as soon as the end of next year and likely in any case before the end of 2023.

“There is considerable variation in the approach of the ECB and the Fed. The Fed is using realised inflation, whereas the ECB will use modelled or forecast inflation, which will provide much more flexibility to keep the pedal to the metal when it comes to policy,” says Hinesh Patel, a portfolio manager at Quilter Investors.

“Despite European vaccine rates finally exceeding that of the US, the region remains grappling with rolling lockdowns, another sub-optimal holiday season, and industries not operating at full capacity. Add in disastrous flooding to the mix and this doesn’t paint a positive picture. All in all, there is no room for any appearance of monetary tightening in Europe at this critical juncture,” Patel adds.