- Euro struggles to find a strong bid

- Markets worry about political unity

- Macron warns bloc's future at risk

Image © European Union.

- EUR/USD spot at time of writing: 1.0820

- Bank transfer rates (indicative): 1.0333-1.0408

- FX specialist rates (indicative): 1.0673-1.0739 >> More information

The Euro-to-Dollar rate was steadying Friday following an earlier sell-off although forecasters are increasingly focused on the downside ahead of a European Council meeting that could exacerbate a growing rift in the bloc.

President Emmanuel Macron ignited fresh political uncertainty after saying in a Financial Times interview that the European Union could find itself collapsing if a common mechanism through which an economic recovery from the coronavirus crisis can funded is not agreed imminently.

Macron said there was “no choice” but to set up a fund that “could issue common debt with a common guarantee” to finance member states according to their needs rather than the size of their economies. This is an idea that Germany, the Netherlands and others have opposed.

The initiative - colloquially referred to as a coronabond - has been promoted by the weaker and more financially vulnerable Eurozone members such as Italy and Spain. But some countries have opposed it out of reluctance to fund the borrowing of other Eurozone nations who're often painted and perceived as being profligate in their spending habits.

"It is right to assert that there should be federal capital raising capacity but we need to find a way for both state and EU funding to operate alongside each other in markets under strict budgetary rules. In the highly unlikely event that the EU unravels, the first step regardless would be the reintroduction of legacy currencies and this would be more disruptive," says David Clark, chairman of the European Venues and Intermediaries Association.

Discerning bond markets have baulked at aiding an expansion of Italy's long overstretched balance sheet, at a point when the government has had little choice but to write unprecedented cheques to companies and households amid a coronavirus-induced 'lockdown' of the Mediterranean country. Cheques that won't clear without financing from the markets, which are demanding increasingly unsustainable levels of interest to fund Italy.

This problem was instrumental in inspiring nine Eurozone leaders to pitch for 'corona bonds' on March 25 - a mutualised form of debt that would sit alongside the mutualised Euro currency - and enable fiscally challenged countries to raise capital cheaply as investors would be more willing to lend if richer northern European nations acting as guarantors.

"Support will still likely have to emanate from the eurogroup advancing with a plan to create a “Recovery Fund” as hinted at in the last statement," says Derek Halpenny, head of research, global markets EMEA and international securities at MUFG. "We see the lack of progress at a government policy level as a factor in building downside risks for EUR/USD. 1.0769 is the EUR/USD low from earlier this month and is the first level in focus on the downside. The sudden turnaround in risk appetite overnight has helped stabilise EUR/USD but we still believe the underwhelming level of fiscal support in Europe could see the March EUR/USD low of 1.0636 tested at some stage soon."

Above: Euro-to-Dollar rate shown at daily intervals.

So far a €540bn rescue package has been put together in place of joint debt issuance but for the most part it requires struggling countries to tap the crisis era bailout fund that foisted humiliating doses of austerity and supervision on many during the debt crisis. Prime Minister Guiseppe Conte initially indicated he'd vote down the agreement in the European Council on April 23 which would, in the process, sink it because the package requires unanimous endorsement.

Conte has since been reported to have said the country should "look at the ESM proposal after approval." Those remarks came after European Council President Mario Centeno told Corriere della Sera that so-called corona bonds have not been ruled out by the European Council, which is expected to contemplate a "recovery fund" and "innovative new financial instruments" next week.

"Even if the USD weren't on the front foot (as it currently is), steering clear of the EUR would be justified. Soft conditions or hard conditions, bailouts or no bailouts, the broad image of the Eurozone looks particularly unattractive. Importantly, "Coronabonds" or some other form of jointly backed debt obligations would not serve as an elixir of sorts, since issuance would be stringently controlled, and many legacy issues would still be left outstanding. In fact, jointly backed debt could potentially exacerbate the dividing lines. We would currently expect the 1.10 area in the pair to act as stiffer resistance going forward," says Stephen Gallo, European head of FX strategy at BMO Capital Markets.

Conte and Centeno's comments suggest the bare bones of a deal may be coming together behind the scenes ahead of next week's meeting, although anti-Euro sentiments have already been lifted in Italy while the fractious debate over corona bonds has meant the EU is yet to provide a fiscal response when national governments moved more than a month ago.

However, if EU leaders neglect to endorse the rescue package and fail to make progress on healing the rift created by the debate over corona bonds one way or the other, markets could begin to doubt the future of the Euro and European Union. There is an election cycle coming, beginning in France next year and arriving in Italy by 2023, which could see incumbents thrown on the scrap heap and separatists ascend to power in a worst case scenario for the Euro.

"The North/South economic and political divides in Europe will probably worsen from here, and there is ultimately no such thing as an "unconditional" Eurozone rescue package. We prefer to fade instances of EUR strength," Gallo says.

Above: Euro-to-Dollar rate shown at weekly intervals.

Casual observers may not have realised the March 25 corona bond proposal of nine countries and subsequent March 26 rejection of it has stoked debt-crisis-level concerns about the long-term prospect of the currency bloc remaining intact because the response of the bond market has been benign in the historical context. This is thanks largely to a European Central Bank (ECB) that once said "we're not here to close spreads" but which has ultimately sought to do exactly that when the situation called for it.

The ECB has added €850bn to its quantitative easing bond buying programme since the onset of the coronavirus crisis and tilted new purchases heavily toward the two most afflicted countries; Italy and Spain. Those countries are also the Eurozone's two most economically and financially vulnerable at the best of times although the 'spread' - or difference in bond yields between those countries and Germany - is less than 2% in 2020 when between 2011 and 2013 it hit 7.5% and sank the Euro as investors feared the intersection of politics in one part and unsustainable borrowing costs in the other would lead to a break-up of the bloc.

"We expect renewed demand for the dollar and yen, and EUR/USD to move towards 1.05. Speculators hold sizeable net-long euro positions that will probably be squeezed," says Georgette Boele, a strategist at ABN Amro. "We expect another risk-off wave in currency markets in Q2, but it is likely that the upside of the dollar versus Pound sterling, Australian dollar, Canadian dollar and New Zealand dollar is now lower than we originally thought."

ABN Amro cut its Euro forecasts in March and has since tipped a fall to 1.05 by the end of June and a recovery to 1.12 by year-end. The bank reiterated those forecasts this week despite upgrading projections for the Sterling as well as the small Dollars relative to the U.S. greenback, with the catalyst for the Euro's declines being an anticipated inrease in risk aversion that forces institutional investors to abandon earlier bullish wagers on the single currency.

Dollar strength and chronic underperformance of the Eurozone economy are both factors in these forecasts, although renewed concerns over unity are also increasingly relevant to price action for the time being too.

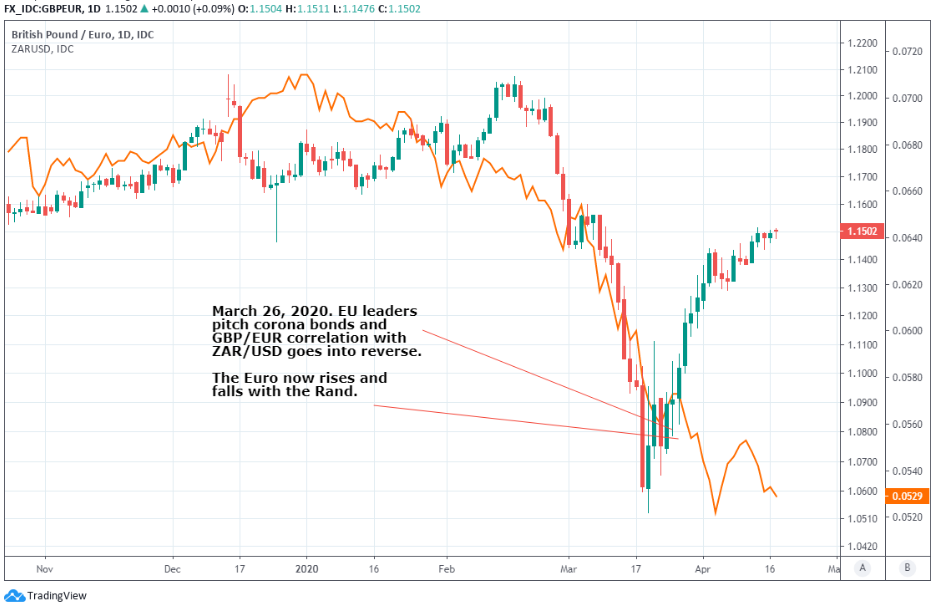

Bond market interventions from the ECB under new President Christine Lagarde have nipped a financial crisis in the bud before it even really began and obscured the true level of concern that exists among investors in the bond market but the signs of stress go beyond the bond market. The Pound-Euro rate had a positive correlation with the South African Rand until recently, which went into reverse on March 26 when EU leaders rejected the idea of corona bonds.

Some observers noted at the time how the Brexit referendum left Sterling trading like an emerging market currency but in April 2020 the Euro was the only emerging market currency in the Pound-to-Euro rate, which now moves in the opposite direction to the ZAR/USD rate. For the time being at least, the Euro now rises and falls with the Rand as it did in the debt crisis and as Sterling did after the Brexit referendum as well as in the dark days of the 2008 crisis.

Above: Pound-to-Euro rate shown at daily intervals alongside ZAR/USD (orange line).