Image © Adobe Images

- EUR is still a 'sell on rallies' currency for now says Credit Suisse.

- Strength would undermine already-insufficient inflation expectations.

- Any rise by EUR would invite a bearish policy response from the ECB.

The Euro continued to languish close to the bottom the G10 league table for 2019 on Friday and could remain there for a while to come if the latest guidance from Credit Suisse is anything to go by, because the bank has told its institutional clients they should keep selling the single currency on rallies.

Europe's unified unit has endured multiple twists and turns in its fortune over recent quarters, with the latest coming after the European Central Bank's (ECB) June assessment of the Eurozone economic outlook was perceived as much less downbeat than what the market had expected.

Financial markets had been betting the ECB would cut its interest rate before long but guidance issued by the bank's chief Mario Draghi suggested only that policymakers are now likely to wait a bit longer before raising borrowing costs for companies and consumers.

As a result the Euro bounced last Thursday and remained on its front foot against rivals well into the current week and it wasn't until Wednesday that the market's appetite for the single currency actually began to wane.

Shahab Jalinoos, global head of currency strategy at Credit Suisse, wrote in a note to the bank's clients this week explaining why such reaction should not have surprised anybody. He also outlined the bank's case for why any further gains are likely to be short-lived.

"The past week has seen both an ECB meeting that was widely interpreted as less dovish than markets had initially anticipated (with ECB chief Draghi emphasising a total lack of deflation concerns), and a softer-than-expected US May payrolls report. With the market convinced that the broader positioning is short EURUSD, it is not surprising that the pair is up," Jalinoos writes.

Changes in rates are only normally made in response to movements in inflation, which is sensitive to economic growth, but impact currencies because of the influence they have on capital flows and their allure for short-term speculators.

Capital flows tend to move in the direction of the most advantageous or improving returns, with a threat of lower rates normally seeing investors driven out of and deterred away from a currency. Rising rates have the opposite effect.

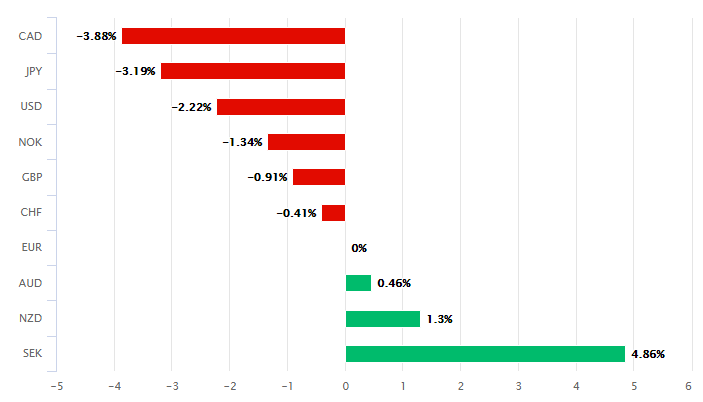

Above: Euro performance Vs G10 rivals in 2019. Source: Pound Sterling Live.

The ECB's perceived optimism came against a backdrop of an increasingly bearish market view on the outlook for the U.S. Dollar, and helped breathe new life into the single currency, which had ceded ground to the greenback ever since late January.

However, that rebound was called into question Wednesday and Friday by U.S. inflation and retail sales figures that might've prompted second thoughts in the market about now-consensus idea that the Federal Reserve (Fed) will slash its interest rate multiple times before the year is out.

"We note that, at time of writing, the gains are still less than 1%, and 3m EURUSD implied volatility is once again declining from historically low levels. This is especially interesting," Jalinoos writes, before giving three reasons that could explain the seemingly lacklustre move in the Euro.

Even before this week's pushback from the Dollar, the rally in the Euro-to-Dollar rate had seemed a lacklustre one when compared with the move seen in June 2017 when the bank surprised markets by suggesting it could soon end the quantitative easing programme that'd kept bond yields, which are most responsive to interest rates, so low.

Above: Euro-to-Dollar rate shown at daily intervals, alongside the Dollar Index (orange line, left axis).

Jalinoos says this could be explained by market concerns over a series of domestic risks lurking on the horizon for the Euro, which are not least of all the odds of Italy clashing with the European Commission over its budget again and potentially introducing a parallel currency to sit alongside the Euro in the domestic market.

Other factors that might explain the bloodless move in the exchange rate include the wide difference between interest rates on either side of the Atlantic, which makes backing the Euro against the Dollar an expensive affair for traders, and perennially weak inflation pressures.

"It is hard to have confidence in a sustained EUR rally. Indeed Draghi himself pointed out in his press conference that EUR strength is a form of monetary tightening, which is notable given that the currency in trade-weighted terms is less than 2% up from its 2019 lows seen in April. This suggests that the higher EUR goes, the further inflation expectations will fall, consistently undermining the case for a still-higher EUR in the process," Jalinoos says.

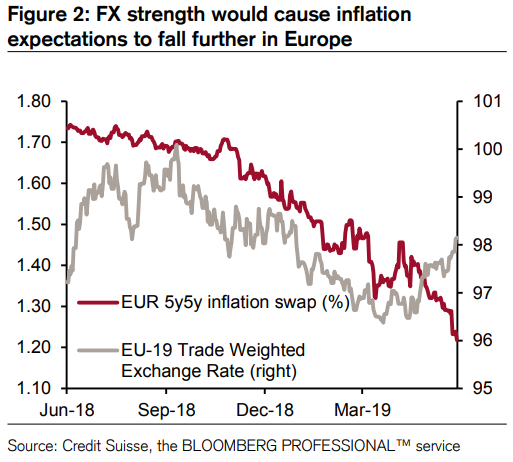

Jalinoos and the Credit Suisse team have flagged that market expectations for Eurozone inflation in five years time suggest strongly that investors see the consumer price index still remaining a long way below the ECB's target of "close to but below 2%" at that time horizon.

Above: Credit Suisse graph showing trade-weighted Euro and 5-year market expectations of inflation.

This is a problem for the European Central Bank and Euro because it's the low levels of inflation on the continent that have necessitated record low interest rates and all manners of 'unconventional' monetary policy in order to try to get inflation higher.

"Of course there are other factors to consider too, for example a sharp rise in European equity markets would offset some of this tightening impact on monetary conditions and allow more room for EUR gains. But the broad principle holds that EUR strength will likely be unwelcome for the ECB and hasten any intention to come through with new forms of monetary easing,"

It's the ECB's record low interest rates that have weighed so heavily on the Euro-to-Dollar rate in recent years. The Euro traded consistently above 1.20 against the Dollar before January 2015 when interest rates were cut to their current record lows and the quantitative easing programme that ended in December 2018 was first wheeled out.

However, the Euro has spent substantially all of the four and a half years since January 2015 trading significantly below the 1.20 level and was quoted at little more than 1.12 Friday. U.S. interest rates have risen from 0.25% to 2.5% during that time, which has also impacted the Euro-to-Dollar rate.

Jalinoos' says any gains by the Euro from here will simply store up even more trouble for the single currency and European Central Bank (ECB) further down the line, so they'll be self-defeating to at least some extent. This is a big part of why Credit Suisse is still advocating selling the single currency on rallies.

"We prefer to stay in sell rallies mode for EURUSD for now, until either European inflation expectations at least find a base or the pair posts a weekly close above March highs around 1.1450," Jalinoos concludes.

Above: Euro-to-Dollar rate shown at weekly intervals, alongside the Dollar Index (orange line, left axis).

Time to move your money? Get 3-5% more currency than your bank would offer by using the services of foreign exchange specialists at RationalFX. A specialist broker can deliver you an exchange rate closer to the real market rate, thereby saving you substantial quantities of currency. Find out more here.

* Advertisement