© Open Water, Adobe Stock

- EUR underperforms after German industrial production contracts again.

- Industrial sector and German economy may now be in recession.

- "There's more to this than just cars," says ING Group economist.

The Euro underperformed rivals Tuesday after official data revealed a second consecutive contraction in German industrial production took place in November, all but ruling out a rebound from weakness seen in the third-quarter and prompting one economist to warn of a "technical recession".

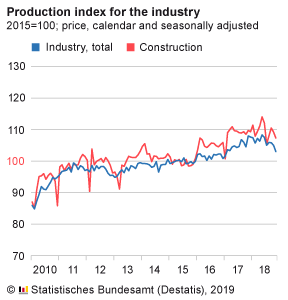

Industrial production fell -1.9% in November when markets had looked for it to grow by 0.3%. Moreover, October's -0.5% decline was revised higher to -0.8%, which leaves overall industrial production down some -4.7% for 2018.

This was driven by a -4.1% decline in consumer goods output as well as falls of -1.8% and -1% for capital and intermediate goods. The capital goods number is what captures changes in output from the car sector.

It was the industrial sector that contributed the lion's share of weakness seen in the third-quarter GDP report, which revealed Germany's first economic contraction since 2015, mainly due to disruption among car manufactureres following implmentation of new rules governing emissions testing.

Now at least one economist is warning the German economy could already be in a "technical recession", which is two consecutive quarters of contraction, although it will be the end of January before observers know for sure what happened to growth in the final quarter of 2018.

German GDP fell -0.2% in the third quarter. Another small negative outturn cannot be ruled out which would mean two consecutive quarters of contraction ensuring a recession by one popular definition.

"Today’s industrial production data has clearly increased the risk of a technical recession in Germany in the second half of 2018. Watch out for tomorrow’s trade data. Another disappointment, combined with the high inventory build-up in 2Q and 3Q, would clearly increase the likelihood of a technical recession," says Carsyen Brzeski, chief German economist at ING Group.

Brzeski says that a recession in Germany would likely be nothing more than a technical adjustment and that there are still plenty of reasons to think growth will return to more normal levels over coming months.

This is not only because industrial order books remain in rude health, but also because spending from consumers and the government could yet make up for any output lost as a result of a slowdown in manufacturing.

"This headline is much worse than we expected," says Claus Vistesen, chief Eurozone economist at Pantheon Macroeconomics. "The German manufacturing sector was in recession in the second half of 2018, reflecting in part the fact that the industry hit capacity constraints earlier in the year and rising global uncertainty amid the trade conflict between the U.S. and China."

Vistesen forecasts that industrial production fell during the fourth and final quarter of 2018, meaning it could now be essential for the consumer and government to pick up slack from the industrial sector if the economy is to have avoided a brief period of recession. Both German and Eurozone retail sales rose sharply in November.

Markets care about the industrial data because manufacturing is Germany's largest economic sector so production numbers here always have an impact on expectations for overall GDP growth.

GDP growth is important for currency markets because it reflects rising and falling demand in the economy, which has a direct bearing on the inflation and interest rate outlook.

"November’s decline in German industrial production adds to the evidence that the euro-zone’s largest economy grew at a meagre pace in Q4," says Jack Allen, a European economist at Capital Economics. "The big picture is that the German economy – and the euro-zone more generally – has clearly shifted down a gear."

In plain English, German economic data matters for the Euro because of what it could mean for the European Central Bank (ECB) interest rate outlook.

The single currency's appeal to investors is hinged on expectations the ECB will begin raising its interest rate in 2019. But in order for it to do this the inflation outlook must remain consistent with a gradual return of the consumer price index toward its target of "close to but below 2%".

A return of inflation toward its target will require the Eurozone economy to continue growing at an inflationary above-potential pace over the coming quarters, which is something that would be less likely to happen if the Euro bloc's largest member were either in or recovering from a recession during the early stages of 2019.

The Euro was quoted -0.27% lower at 1.1447 against the Dollar following the release Tuesday while the Euro-to-Pound rate was -0.10% lower at 0.8968.

Both exchange rates have fallen so far in 2019 and the Euro declined against all G10 currencies during the morning session Tuesday.

"That's put paid to the latest attempt at breaking out of the upside of the current EUR/USD 1.13-1.15 micro-range, and yet we're still around 1.1450 as I write," says Kit Juckes, chief FX strategist at Societe Generale, following Tuesday's data."The narrowing in the Treasury/Bund yield differential is doing stalwart work in defending the downside for EUR/USD now and my confidence we've seen the lows for this cycle is growing."

Juckes says a recent decline in U.S. government bond yields means the Euro-to-Dollar rate should be spared from any notable losses over coming weeks but that, without a concurrent pick-up in German government bond yields, the 1.13-to1.15 range that has gripped the currency pair for weeks now will hold for "some time".

Advertisement

Bank-beating exchange rates. Get up to 5% more foreign exchange by using a specialist provider to get closer to the real market rate and avoid the gaping spreads charged by your bank when providing currency. Learn more here