Image © Adobe Images

- Pair bounced off key 1.1300 yearly lows

- More upside expected on balance in week ahead

- The main release for the Euro is retail sales

- Dollar eyes mid-term elections, FOMC

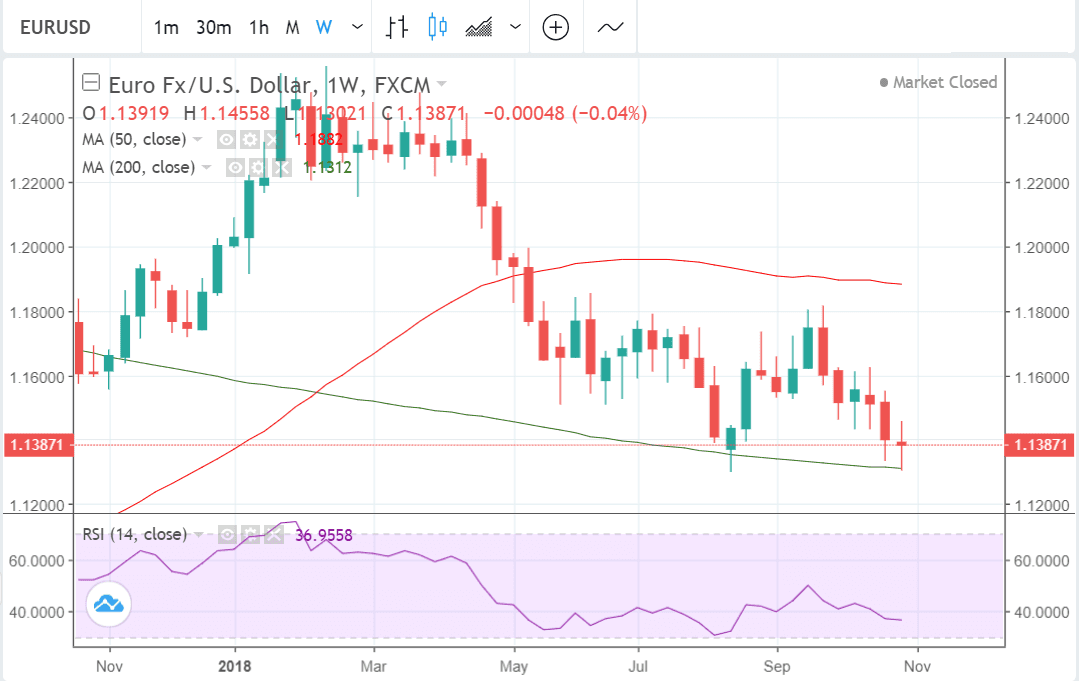

Last week the EUR/USD pair touched the yearly low at 1.1300 before staging something of a recovery. One interpretation of the late-week recovery is that it ensures the exchange rate closed above key lows which can be interpreted as somethign of a bullish signal for the pair.

Coinciding with the 2018 lows was the 200-week MA which enhanced support at the level and probably contributed to the defense and subsequent bounce.

The pair rose up strongly on Thursday and Friday morning but then lost ground in the afternoon after the release of Non-Farm Payrolls (NFP) boosted the Dollar, due to a better-than-expected rise in vacancies filled in October.

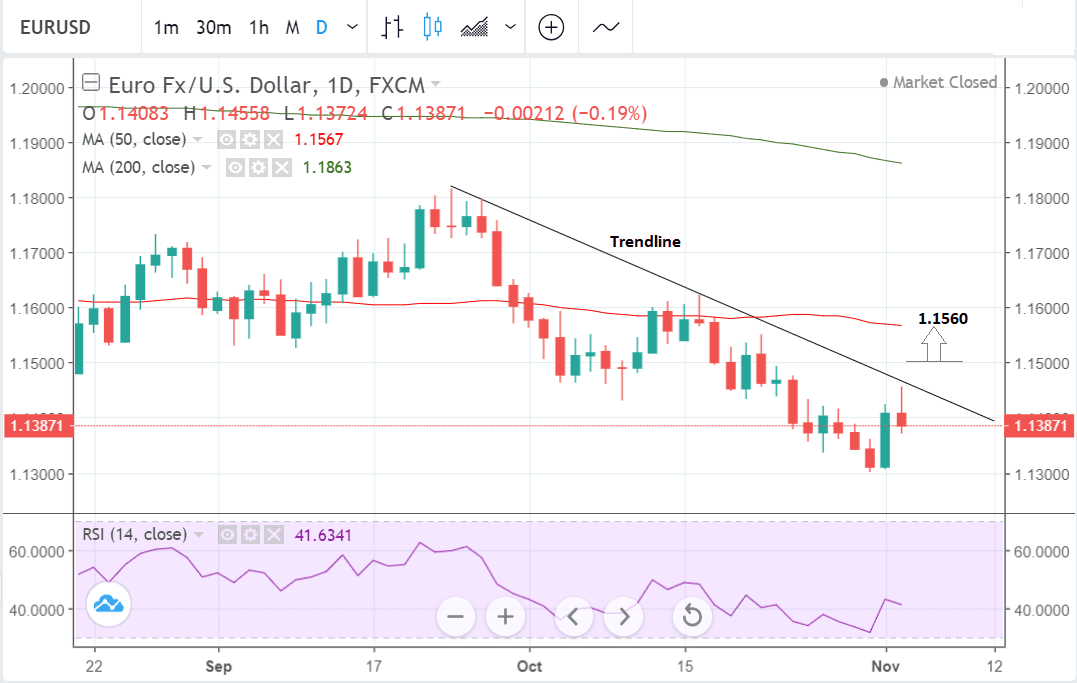

The pair remains stuck below the trendline for the move down from September, however, a clear break above 1.1500 or above the trendline on a closing basis, would probably provide confirmation of an upside break, which would be expected to rise up to an initial target at 1.1560, just below the level of the 50-day MA at 1.1567.

The 50-day is likely to provide tough resistance to further gains and the exchange rate is at risk of rotating after touching the MA and moving lower.

Although the pair has avoided a sell-off below the 2018 lows the risk remains they will capitulate and eventually successfully break below them. Such a move would open the way down to more bearish loses, with the next target probably at 1.1203 where the S1 monthly pivot is situated, and likely to provide a safety net of sorts.

Overall we are marginally biased to expecting further upside, however, as the Euro is very undervalued and the US Dollar quite overvalued, compared to fair value estimates based on economic fundamentals.

This suggests the pair is more likely to drift higher and going any lower will exacerbate the already stretched valuations as they are, as such we see a marginal bias to further gains in the week ahead.

Advertisement

Bank-beating EUR-USD exchange rates: Get up to 5% more foreign exchange by using a specialist provider to get closer to the real market rate and avoid the gaping spreads charged by your bank when providing currency. Learn more here

The U.S. Dollar: What to Watch this Week

The mid-term elections will take place this week, with the outcome widely tipped to result in a stalemate in Congress with Republicans maintaining control of the Senate and Democrats retaking control of House of Representatives.

The outcome, "is unlikely to drive a market reaction," says Daniel Been, Head of FX Research at ANZ Bank. "In the medium term, we don’t see this as a positive outcome. It would halt policy progress and very likely push the President to focus on what he can control without support from the houses – notably, trade policy."

"We expect 1.13 to hold, unless the Republicans pull-off a majority in both chambers in the mid-terms on Tuesday," says Andreas Steno Larsen, Global FX Strategist with Nordea Markets. Larsen does however warn against considering a hung-congress a done deal.

Larsen cautions that Trump is certainly not as unpopular as many traders might think when once mainstream press coverage is taken into account. Using regression modelling based on previous mid-term elections Nordea Markets believe there is a chance the Republicans hold onto both houses by a notch.

The main economic calendar event for the U.S. Dollar in the week ahead is likely to be the meeting of the US Federal Reserve (Fed), on Thursday at 19.00 GMT.

The Fed sets interest rates, which have a profound impact on the Dollar. When interest rates rise, so does the greenback.

Currently, analysts do not think the Fed will change interest rates at their meeting on Thursday. The market, will, however, nevertheless, be watching for any changes in wording in the accompanying statement from the Fed, and J Powell's press conference, about their expectations for future policy.

Analysts at Westpac think it is unlikely, the Fed will alter their stance given strong recent economic data which has, if anything, reinforced, their hawkish outlook for about an average of three 0.25% interest rate hikes in 2019.

"Come the November meeting, there is no reason to expect a material change in view, though rates will not be raised. Employment growth has remained strong, so too GDP," says a currency strategy note from Westpac Bank. "The nascent evidence of interest rate sensitive sectors coming under pressure is unlikely to concern the Committee at this stage with policy still seen as accommodative. This is also true of recent market declines as equities remain at elevated levels."

The other main release in the coming week is non-manufacturing ISM which is forecast to slow to 59.3 from 61.6 previously when it is released on Monday at 15.00.

JOLTS Job openings are also out at 15.00 on Tuesday.

Euro: What to Watch

While there is no major data release out of the Eurozone scheduled for the coming week, what data there is will be scrutinised more than usual owing to worrying signs of slowdown in the Eurozone economy.

We have seen data disappoint over recent weeks and markets have been wondering whether or not it is prudent for the European Central Bank (ECB) to reduced it stimulatory support to the economy.

Expectations for the ending of the support tend to prompt a stronger Euro, but expectations for any delay in the ECB's withdrawal of stimulus tend to weigh on the currency.

"While the ECB is set to end QE this year, persistent soft inflation undermines its (and investors’) confidence in the scope for eventual rate rises. Further, while activity data continues to deteriorate we see scope for more sustained weakness in the EUR over the medium term," says ANZ Head of FX Research Daniel Been.

The main release for the Eurozone is probably retail sales in September, out at 10.00 GMT on Wednesday, which is forecast to show a 0.1% rise on a monthly basis.

The ECB's latest economic assessment is out on 09.00 G.M.T on Thursday, and may well be closely scrutinised by traders looking for hints about whether the central bank is having doubts about removing stimulus in 2019, due to slower growth.

If the ECB is having doubts the Euro could see a quite rapid sell-off.

The October PMI data out on Monday are revisions so unless they differ markedly from the first estimates are unlikely to change the currency.

Advertisement

Bank-beating EUR-USD exchange rates: Get up to 5% more foreign exchange by using a specialist provider to get closer to the real market rate and avoid the gaping spreads charged by your bank when providing currency. Learn more here