- Pound to Euro exchange rate (19-7-17): 1 GBP = 1.1303 EUR

- Euro to Pound Sterling exchange rate: 1 EUR = 0.8849 GBP

Pound Sterling is expected to suffer a sizeable adjustment lower against both the Dollar and Euro, and not even an interest rate rise at the Bank of England will help the currency.

In fact, such a move could actually be one of the drivers of the move lower argue strategists at HSBC Bank plc.

There is a clear divide within the policy-setting team at the Bank of England with regards to whether or not they should raise interest rates.

Concerns over rising inflation have seen more members of the Bank’s Monetary Policy Committee signal that an interest rate rise might be needed to quash rising inflation.

Bank of England Governor Mark Carney’s hawkish comments made towards the end of June added an extra notch to the debate. By explicitly stating that “some removal of monetary stimulus is likely to become necessary”, this indicates a rate hike is not just possible, but might even be probable.

Recall as a rule of thumb, rising interest rates are a positive for a currency as higher rates attract greater inflows of foreign investor capital as global investors seek greater returns in assets like government bonds.

This dynamic might explain why Sterling continues a steady rise against the Dollar and won’t fall further against a bullish Euro.

But, this dynamic is ultimately not going to last we are told.

“We believe it would be a mistake to hike rates in the UK at this juncture and do not believe a rate hike would cause a sustained rally in Sterling,” say HSBC FX Strategists David Bloom and Dominic Bunning in a recently co-authored research note.

Get up to 5% more foreign exchange by using a specialist provider. Get closer to the real market rate and avoid the gaping spreads charged by your bank for international payments. Learn more here.

Why Now is Not the Time to Raise Rates

Let’s say Brexit never happened and the UK was the best-performing major economy in 2017m as it was in 2016, a scenario would likely result in whcih the labour market nears full employment.

Wage pressures naturally build as employers have to pay more for labour.

“This causes a rise in nominal wage growth which prompts stronger consumer spending and demand-driven inflation. Such higher inflation would be more permanent in nature – a condition that warrants a series of rate rises,” note Bloom and Bunning.

By raising rates, inflation is therefore tempered. “If this is a cyclical upswing in growth and inflation, then a rate hike would be appropriate and GBP would justifiably rally,” say Bloom and Bunning.

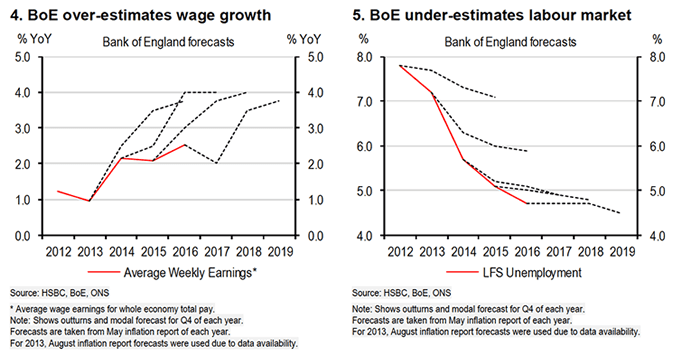

However, this is all good in theory - even though UK unemployment has fallen at a sharper rate than the BoE expected, significant wage growth has not materialised.

“That the BoE has simultaneously over-estimated wage growth whilst under-estimating the drop in unemployment should not be ignored,” say Bloom and Running.

HSBC believe hiking rates in this environment might risk exacerbating consumer retrenchment at a time of heightened political uncertainty.

“This could induce a more vicious downturn and might cause GBP to fall even further,” warn the two analysts.

The last thing the UK needs in HSBC’s view is an unnecessary rate rise being added to the already difficult economic and political outlook.

Because the rise in inflation is structural - i.e driven by the one-off event in Sterling’s depreciation as opposed to a cyclical upswing in economic momentum - “then a rate hike now could exacerbate the slowdown in consumption and the mechanism could assume a new and unwarranted brutality”.

Monetary tightening could prompt GBP weakness, not strength. We have seen this before in other economies.

The Russian Example

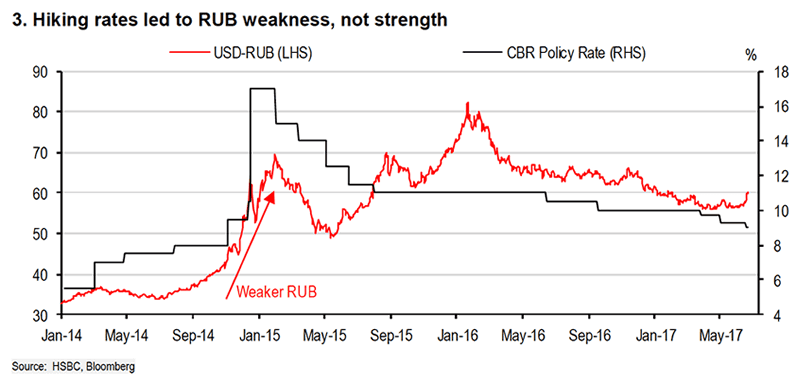

HSBC point to the recent experiences of Russia where unwarranted interest rate rises caused an unexpected decline in the value of the currency.

“The UK’s vote to leave the EU is an exogenous shock that prompted sharp GBP weakness. Some similarities can be drawn with the exogenous shock Russia experienced from a collapsing oil price in 2014,” explain Bloom and Bunning.

With Russia’s key export declining so rapidly in value, the Ruble came under severe pressure, depreciating by over 40% versus the USD in the second-half of 2014.

By the end of the year, inflation had jumped to double digits, and the Central Bank of Russia (CBR) faced a similar, albeit more extreme, predicament to that which the BoE confronts today.

This left the CBR with two options:

1. Hold policy steady and let the real income squeeze rebalance the economy

2. Raise rates in conjunction with the real income squeeze

“The CBR responded by raising rates. The CBR prioritised pulling inflation lower and stabilising the currency, and delivered an aggressive 650bp emergency hike on 15 December 2014,” note Bloom and Bunning.

Yet a sustainably stronger RUB did not emerge; the analysts note that instead the FX market realised the dire consequences that were to follow such aggressive monetary tightening and the RUB weakened even further in the early part of 2015.

Why did the move backfire on the CBR; why did the Ruble actually fall in response to aggressive interest rate rises?

“In the market’s eyes this interest rate reaction would lead to considerable pain for the Russian consumer. It was only as inflation subsided in 2016 and real rates moved back into positive territory that the RUB started to recover,” explain Bunning and Bloom.

They add, Russian consumers, who were already squeezed through falling real incomes, now faced much tighter monetary policy. Consumption fell off a cliff, prompting a recession.

“Although hiking rates in Russia did accelerate the rebalancing of the economy, the pain the consumer had to endure was acute,” say the co-authors.

HSBC do not believe the UK warrants such a drastic course of action and it is unlikely the BoE wants it either.

“But it underlines that when there is a structural break, and the currency is falling thereby squeezing real incomes, a tightening of monetary policy does not guarantee a stronger currency,” say Bunning and Bloom.

“We believe the UK is in the midst of a structural and political upheaval that warrants inaction from the BoE. If the BoE were to hike, we think it could actually lead to GBP weakness rather than strength,” say the analysts.

The view is not unique to HSBC, with analyst Kathrin Goretzki of Italian lender Unicredit S.p.A. breifing clients that a premature interest rate rise would represent something of a policy mistake by the Bank.

UniCredit maintain a view that the BoE will stay on hold during the time of Brexit negotiations and while, "UK sentiment is showing signs of deterioration, real incomes are being squeezed and inflation has risen while wage growth remains stagnant".

So Where is the British Pound Going?

So, would it be wise to go against the flow if Sterling rallies on further signs that an interest rate rise at the Bank of England is becoming more likely?

If HSBC are correct, this could well be the case.

HSBC forecast the Pound to Euro exchange rate to fall to 1.00 by the end of 2017, where it is predicted to languish until mid-2018.

The Pound to Dollar exchange rate is forecast to trade down to 1.22 by the end of 2017 ahead of a further decline down to 1.20 in early 2018; a level it should stay at over subsequent months.

{kind=link}