- Markets:

- 1 GBP = 1.1565 EUR. Day's best = 1.1559, low = 1.1537

- 1 EUR = 0.8652 GBP. Day's best = 0.8667, low = 0.8639

Pound Sterling is seen trading steady against its major competitors but downside pressures continue to linger for the currency.

Domestic news remains thin with an update to UK GDP data from the ONS proving unremarkable from a currency perspective but nevertheless confirming the UK economy remains exposed to a slowdown.

This is a negative for the currency on a longer-term basis but in the near-term the Pound to Euro exchange rate is being driven by the Euro.

Those with an interest in this market should therefore be watching at Euro-orientated events in the near-term we believe.

European stock markets continue to provide the main source of demand for Euros as global investors flock to a region that is in the midst of a sustained cyclical recovery.

The desire for exposure to Europe by investors is one reason why the Euro is the best-performing currency of the month and of 2017.

“Demand for Euros remains strong and steady,” says Samarjit Shankar, Managing Director, Head of iFlow and Quant Strategies at Bank of New York Mellon. Shankar has been watching the movement of funds into Europe for some time now and finds no surprises in the currency’s recent outperformance.

The Pound to Euro exchange rate is seen trading at 1.1583 at the time of writing having been under sustained pressure against the Euro for a week now.

The pair was seen as high as 1.1927 earlier in the month.

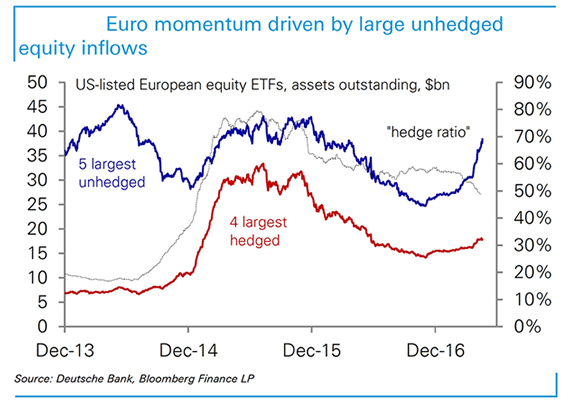

“The Euro's momentum remains strong thanks to large unhedged equity inflows,” says Robin Winkler, Strategist with Deutsche Bank in London.

That investors are not hedging exposure would suggest they expect the Eurozone economy and the Euro itself to maintain strength for a good portion of time.

“A potential reallocation of foreign investors into European equities, as euro area politics look less threatening, likely will offer support to the EUR," says Hamish Pepper, an analyst with Barclays Bank in London.

Can the Move in Favour of the Euro Continue?

There are however concerns that the rally might be at risk of overheating and that a dose of profit-taking amongst investors might spark a period of Euro weakness.

The EUR/USD rate is looking increasingly overbought and should it reverse direction then we could well see the EUR/GBP catch a break.

The timing and scope of the retracement is however the hard bit to call.

We expect and dips in the Euro’s strength to prove short-lived as the fundamental drivers behind the Euro remain in place and it will take some more time before the market seriously questions them.

“It is interesting to note that the size of the ECB’s balance sheet now exceeds that of the Federal Reserve’s, driven by the ECB’s ongoing asset purchases and the Euro’s strength of late,” says Shankar. “Expectations of ECB-Fed policy divergence may continue to buoy European asset market inflows which, if sustained, should underpin the Euro.”

Deutsche Bank’s Winkler also sees the prospect of the Euro strengthening further from here.

“While our equity strategists caution that valuations are getting to be stretched, we expect foreign investors to continue to re-allocate into Eurozone stocks in the near-term at any rate,” says Winkler in a note to clients dated May 22.

The pro-Euro story will also be tested by the European Central Bank (ECB) who will deliver their latest policy verdict on June 8.

Markets are front-running a decision by the ECB to withdraw its quantitative easing programme and start raising interest rates.

The risk then is that the ECB doesn’t play ball with the markets and indicate such moves.

But, strategist Yianos Kontopoulos at UBS remains optimistic:

“We have been EUR/$ bulls since late November 2016. We continue to prefer Europe as the location to take cyclical risk. And heading into the June ECB meeting the market may continue to trade the European outperformance theme across stocks, bonds and FX.”

So the rally could well last until June based on the above.

There are some doubters.

“Clients have built considerable EUR-longs in anticipation of portfolio inflows into Eurozone stock markets and unwinding of EUR-funded carry trades as the ECB moves ever closer to the QE taper. We doubt that these inflows can boost EUR, however, so long as they are hedged,” says Valentin Marinov at Crédit Agricole Securities in New York.

Recall that to date, most of the inflows have been unhedged as investors feel confident enough in the future direction of Eurozone economic growth and ECB policy to not buy protection.

But Marinov says the hedging behaviour of the investors and, ultimately, the timing and the aggressiveness of the ECB taper will depend on the Eurozone inflation outlook.

“We expect the relative fundamental outlook for EUR/USD to deteriorate from here. Starting with EUR, we expect Eurozone inflation to slow down sharply in May,” says Marinov.

The release is due on 31 May.

Inflation is going higher but there are concerns that core inflation is not going higher - this is inflation that cuts out the more volatile elements of the inflation picture - for instance fuel rises.

Core inflation therefore gives a better picture of underlying wage growth and the strength of the economy.

The ECB has long used core inflation data as a benchmark for their decision-making arguing that until core inflation heads towards 2% in a sustainable manner there is little reason to raise interest rates.

If there is no sign of a strong pickup in core inflation market expectations concerning the ECB event in June might be seriously questioned and so too will the Euro’s rally.