- GBP/EUR ascending in 1.15 to 1.18 range

- UK, European calendars quiet

- GBP/EUR eyes 1.20 for this summer

- EUR/USD recovery & CNH turn lower to aid GBP/EUR

Image © Adobe Images

- GBP/EUR market rate at publication: 1.1480

- Bank transfer rates (indicative): 1.1170-1.1260

- Specialist transfer rates (indicative): 1.1330-1.1400

- More about bank-beating exchange rates, here

- Set an exchange rate alert, here

The Pound-to-Euro exchange rate edged lower last week but could close the gap over the coming days with a swift reclamation of 1.15 leading to a choppy but ascending range throughout this quarter.

Pound Sterling was one of the big fallers when the Euro rallied late last week but with the UK economic picture too robust for it to be left behind by the single currency, a swift recovery of 1.15 is likely first on the agenda this week.

"Data-flow out of the UK was once again supportive for sterling, as strong retail sales, good PMIs, inflation rising (although slightly below expectations) and unemployment edging lower all endorsed the strong recovery narrative,” says Francesco Pesole, a strategist at ING.

"The data calendar next week is, instead, very quiet,” Pesole says.

This is a positive backdrop for Sterling and one which supports a renewed ascent within the recently earmarked range this week, which is also a period in which both UK and European economic calendars fall quiet.

The Pound-to-Euro exchange rate has traded as high as 1.18 in recent weeks and generally found good support around 1.15, which has led to a downward bias for EUR/GBP.

“In our view, EUR/GBP has plenty more room to drift lower. The starting point is EUR/GBP remains highly overvalued relative to the level implied by real interest rate differentials,” says Elias Haddad, a senior FX strategist at Commonwealth Bank of Australia.

Above: Pound-to-Euro exchange rate shown at daily intervals alongside EUR/GBP.

Haddad and the CBA team say “fair value” based on bilateral interest rate differentials is around 1.4280 for the Pound-to-Euro exchange rate but that it’s unlikely to trade as high as that any time soon because of the UK’s current account deficit.

CBA told clients last week that they should instead actively wager that Sterling rises to 1.25 over the coming months, while at the same time giving a strong indication that analysts at the bank do not expect Sterling to return to or below the 1.1357 level.

“Failure here will revert attention again to initial support at .8533 [GBP/EUR: 1.1719], the mid-March low and the March and May 2019 lows,” says Karen Jones, head of technical analysis for currencies, commodities and bonds at Commerzbank, referring to EUR/GBP.

There are lots of reasons for why bullish Sterling and Euro projections could appeal to readers, though yours truly likes them for reasons other than those advocated elsewhere and personally looks for GBP/EUR to ascend within a 1.15-to-1.18 range this quarter.

{wbamp-hide start} {wbamp-hide end}{wbamp-show start}{wbamp-show end}

That would be ahead of a subsequent rise to 1.20 and above this summer, and alongside a strong rally for EUR/USD as well as the central and eastern European currencies like the Polish Zloty and Romanian Liev.

Subject to conditions in the domestic economies concerned, those moves would be additional to gains in Asian, American and antipodean currencies like the Singapore Dollar, Korean Won, Australian Dollar, Canadian Dollar and Mexican Peso.

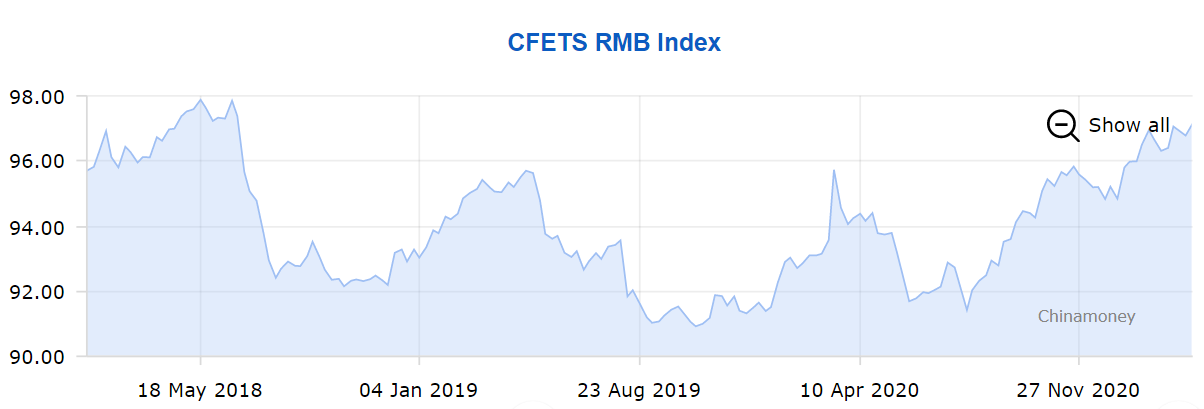

The reason is a seemingly overdue turn lower by the Renminbi against the China Foreign Exchange Trade System (CFETS) basket of currencies, which would appear misleading to some for its concurrence with a USD/CNH fall all the way to something like April 2018 lows of 6.33.

A USD/CNH fall to 6.33 would reflect a strengthening of the Yuan against the Dollar but, coming alongside a EUR/CNH rally near to 8.17, would actually be driving a trade-weighted Renminbi depreciation that was denied to it in January and the first quarter by Euro weakness.

Above: GBP/EUR at weekly intervals with Fibonacci retracements of referendum fall, major moving-averages.

“External factors for China’s currency, the yuan, to appreciate are weakening” according to a Reuters report covering remarks made by Xuan Changneng, deputy administrator of the State Administration of Foreign Exchange (SAFE) at the Boao Forum on Monday.

Relative to the CFETS basket the Renminbi has this year completed its longest unbroken stretch of appreciation for years, while managers of China’s foreign exchange reserves have given a pretty clear hint that some of this appreciation is likely to reverse in the months ahead.

This is where things get interesting because there are only two ways in which the Renminbi is able to depreciate meaningfully against the CFETS basket.

One of those is through a EUR/USD rally to around 1.29 over three-to-six months, which helps drive EUR/CNH near to 8.17 and comes alongside an incremental reshuffling of SAFE’s reserve basket by managers at the Peoples’ Bank of China (PBoC) so as to minimise adverse impacts on others’ trade-weighted currencies.

That’s where the envisaged GBP/EUR ascent to 1.20 comes in, as a large Sterling move is necessary in order to keep the trade-weighted Euro from going through the roof as it appreciates against the Dollar and Yuan.

Likewise with moves in the Zloty and other Central or Eastern European currencies as well as some of those from Asia and North America.

Above: Renminbi CFETS Index.

This is one of the two possible pathways for the trade-weighted Renminbi and the only pattern of price action that would be consistent with both the current reflation theme in financial markets, as well as the inflation-targeting objectives of central banks whose currencies are concerned.

"A central bank should always manage its reserves in such a way that it does not destabilise markets, take advantage of privileged information or hinder another central bank’s operations or objectives,” writes John Nugee, former chief reserve manager for the Bank of England.

The other and only alternative pathway for the Renminbi would, partly through correlation effects, involve such broad U.S. Dollar strength that it would be consistent with neither the global reflation theme nor the new average inflation targeting objective of the Federal Reserve.

Widespread Dollar strength would cheapen U.S. import costs, reduce inflation and undermine the Fed’s pursuit of its policy “objective” which, in the presence of alternative options, is not the done thing among the leading central banks in the world.

It’s also not the done thing at the PBoC if 2021’s order of gains and losses across the Chinese exchange rates included in the CFETs basket are anything to go by, with first-quarter Renminbi gains over the Euro and Japanese Yen evidencing this.