Above: File image, Catherine Mann. Image: OECD.

The prospect of a 50 basis point hike at the Bank of England in May has been reignited by Catherine Mann, a member of the Bank's Monetary Policy Committee.

In a speech made on Thursday Mann said she saw evidence businesses and consumers' price expectations were pivoted towards stoking further inflation, to the extent longer-term inflation rates remain stubbornly above the Bank's 2.0% target.

Mann voted for a 50 basis point hike in February on the view that it was better to raise rates fast and early in order to minimise the overall amount of rate hikes required to get inflation under control.

"We can look at whether or not an additional 25 basis points or more might be necessary in order to keep inflation anchored," Mann said in response to questions after a speech on Thursday.

For Mann it remains the case that central bank interest rate hikes serve the important purpose of managing future inflation expectations at firms and households.

In her first speech as a member of the MPC back in January she said striking early and decisively was critical in containing inflation expectations; she followed that speech by voting for a 50 basis point hike on the occasion of the February meeting.

The Pound has found support over recent months on expectations for higher interest rates at the Bank of England in 2022 and 2023, as of the time of writing the market is pricing in 147 basis points of further rate hikes.

Mann's comments are therefore largely supportive of market pricing and Pound exchange rates.

She said the costs of a central bank overreacting to higher inflation are less than the costs of underreacting.

"The costs of making a mistake if the true inflation process is more persistent are larger than if the true inflation process is less persistent," said Mann.

This underpinned her decision to hike rates 50 basis points in February:

"Front loading the policy reaction did not necessarily imply a higher Bank Rate in the long-run – my focus was on the slope of the policy path. A bold tightening followed by a hold, or even a modest rate reversal appeared to me to be appropriate to address inflation expectations."

"A rate reversal at some future point would not necessarily be a mistake, nor a harbinger of recession, as it is sometimes viewed," she adds.

Mann says the March policy decision presented policy makers with a new set of issues: namely the surge in energy prices.

After all, this meeting followed Russia's invasion of Ukraine and the associated surge in gas and oil prices.

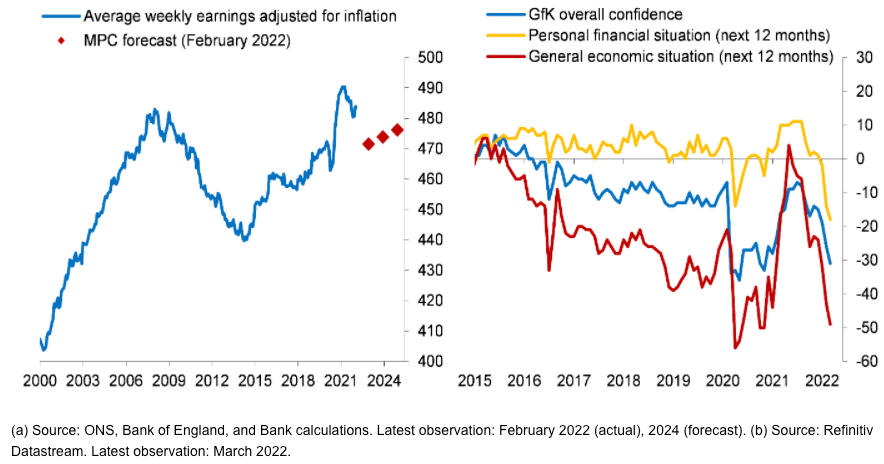

Above: "Real average weekly earnings (a) and GfK consumer sentiment indices (b) GBP at 2015 CPI (LHS) and diffusion index (RHS).

Mann calculates the impact of a doubling of consumer-facing energy prices – about what the October price cap might be relative to before-Covid – generated a reduction in real aggregate non-energy consumption of roughly 2%.

"This would come on top of any reduction in demand caused by the 2% drop in real post-tax labour income that was projected for 2022 as of the February forecast," said Mann.

Therefore a sizeable reduction in demand was considered by policy makers at the time the March MPC meeting came about.

This will inevitably impact the thinking of the Bank of England going forward and could prompt some members of the MPC to display caution in raising rates further.

This would lower expectations for the number of future rate hikes at the Bank, potentially weighing on the Pound.

But Mann remains relatively 'hawkish' in her belief that raising rates earlier is less costly than being put on the back foot and raising rates further and for longer in the event inflation becomes embedded.

She says UK businesses look intent on hike prices in the future, which should drive inflationary pressures.

She cites the monthly Decision Maker Panel (DMP) survey of Chief Financial Officers from small, medium and large UK businesses in signalling heightened pricing intentions.

Mann fears if firms embed current overall inflation into their own-pricing it may point to a situation in 2023 where pricing remains robust even as demand remains weak.

Mann maintains her view that it is better to raise rates early than be left behind by events: "monetary policy needs to keep inflation expectations anchored; by doing so now, less tightening will be required later, when demand may still be weak."