- EUR/CHF nears 1.06 as EUR/USD approaches 1.15

- Could hold 1.05 as trend begins to turn, UBS says

- After ECB warns balance of inflation risk is shifting

- GBP/CHF & USD/CHF bid by BofA Global Research

Image © Adobe Images

The all-important EUR/CHF exchange rate could steady above 1.05 in the months ahead, according to UBS Global Wealth Management.

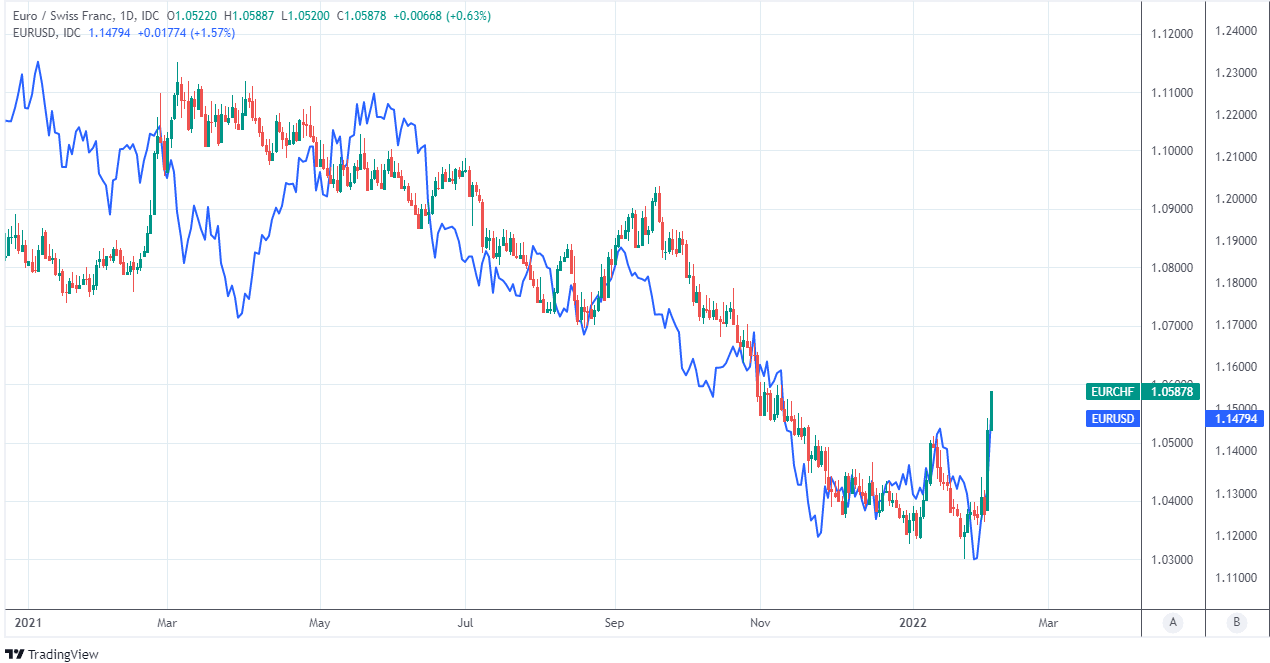

Europe’s single currency rallied back toward the 1.15 handle and its highest level since November last year on Friday, lifting the EUR/CHF exchange rate back toward 1.06 in the process as markets contemplated a possible end to the era of negative interest rates at the European Central Bank (ECB).

This was after President Christine Lagarde said on Thursday that uncertainty about the ECB’s inflation outlook has increased and that risks are tilted to the upside along the immediate path ahead, leading some economists to revise forecasts in favour of an interest rate rise as soon as late in 2022.

“The ECB council signalled concern about inflation in its press conference on 3 February. Rate hikes this year cannot be excluded anymore,” says Thomas Flury, head of FX strategies at UBS Global Wealth Management.

“EURCHF is likely to stabilize above 1.05 as soon as markets return to a risk-on mode and start to expect an unwinding of ECB stimulus,” Flury and colleague Gaétan Peroux said in a note to clients on Friday.

Above: Euro-Swiss Franc exchange rate shown alongside EUR/USD.

While it’s still early days and much about the Eurozone economic outlook could yet change in the interim, the mere prospect of an increase in the ECB’s negative 0.5% deposit rate has evidently prompted many in the market to walk away from earlier bearish bets against the Euro-Dollar exchange rate.

That has in turn eased the downward pressure on EUR/CHF, which has often been a source of consternation for the Swiss National Bank (SNB), and led strategists in the chief investment office of UBS Global Wealth Management to become more confident in their forecasts for EUR/CHF this year.

“The kettle of hawks continues to grow with the BoE and ECB joining the Fed in starting to head towards the exit of their extraordinarily easy monetary policy settings,” says Valentin Marinov, head of FX strategy at Credit Agricole CIB.

“The JPY will continue to underperform most of the rest of the G10, and the equally dovish SNB will see the CHF pace the JPY at the back of the G10 currency pack. Whether or not this environment will continue will depend heavily on risk sentiment,” Marinov and colleagues said on Friday.

{wbamp-hide start} {wbamp-hide end}{wbamp-show start}{wbamp-show end}

The tentative shift in the ECB’s assessment of the balance of risks around inflation followed Eurostat data showing Eurozone inflation edging higher from 5% to 5.1% in January when many professional forecasters had anticipated that it would decline to 4.4%.

The ECB itself had envisaged that Eurozone inflation would to around the turn of the year and so far the indications are that it could remain elevated for longer, potentially necessitating a change in the bank’s monetary policies further down the line.

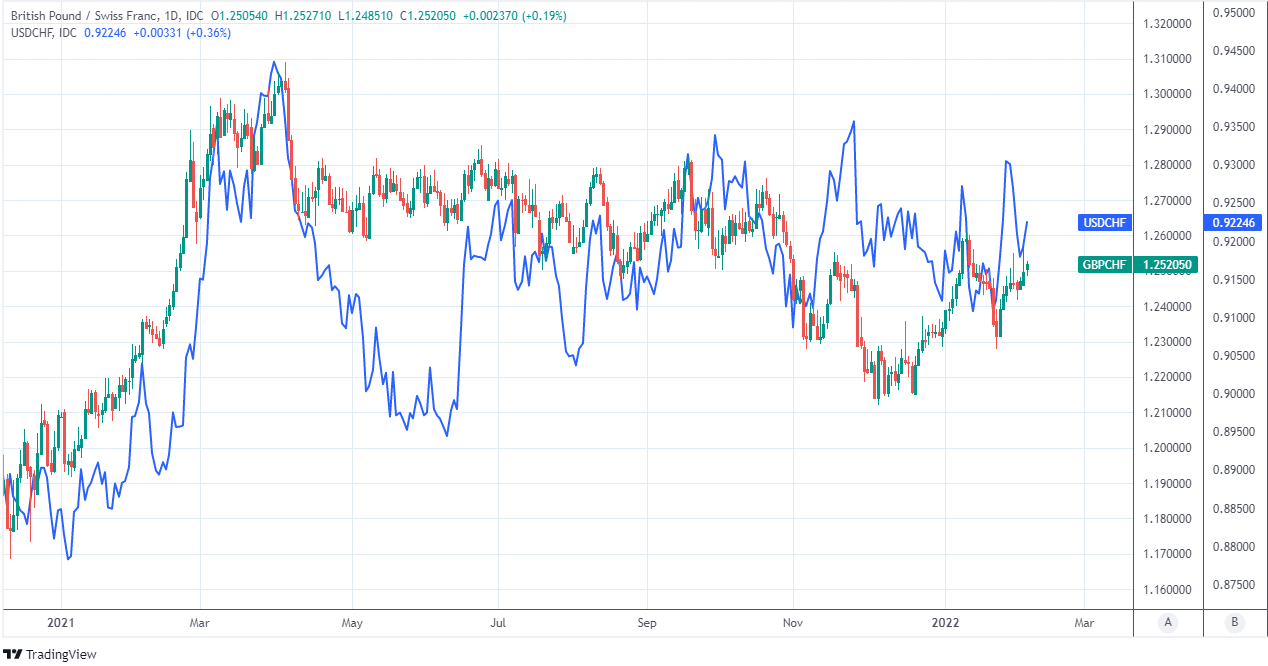

“Our only bullish USD signal is long USDCHF (+1) and it is a modest one at that,” says Ben Randol, a strategist at BofA Global Research.

“By magnitude, our strongest signals on the crosses are long GBPCHF (+6) and long CADCHF (+5). These are pro-risk, pro-carry and pro-commodity FX exposures,” Randol and colleagues wrote in a Friday research briefing.

Above: GBP/CHF shown at daily intervals alongside USD/CHF.

While the European Central Bank inflation stance is shifting and with it, the Euro-Dollar and EUR/CHF rates, there has been little sign of a change in policy on the horizon at the Swiss National Bank (SNB) thus far.

“The stronger CHF has shielded Switzerland from the high inflation rates in other G10 countries. Still the SNB remains active in the currency market to prevent too much CHF strengthening,” says UBS’ Flury and Peroux.

Like in other jurisdictions including the Eurozone, Switzerland’s inflation rates have been submerged far below the levels desired by the SNB for many years but unlike in the Eurozone, there’s reasons for why the outlook and balance of risks could be set to remain on the downside for Swiss inflation.

Not least of all among these is the strength seen in Swiss Franc exchange rates including during the last year, which has continued to weigh on Switzerland’s inflation rate and could potentially ensure the SNB continues with its negative interest rate policy throughout the coming year.

That’s one significant reason why exchange rates like USD/CHF and GBP/CHF could remain pointed higher during the months ahead.