- CHF among top performing major currencies this quarter

- Signs of SNB opposition could frustrate CHF's path ahead

- Supportive development for USD/CHF, GBP/CHF, EUR/CHF

Image © Adobe Images

The Swiss Franc has been an outperformer major currencies in recent months but after drawing the scrutiny of the Swiss National Bank just days ahead of this week’s meeting, it may now face a more arduous path ahead that would be supportive of USD/CHF.

Switzerland’s Franc advanced further against most counterparts early this week and ahead of Thursday’s SNB policy decision in a continued demonstration of the “very strong” credentials cited by the Bank in September for market interventions, that appear to have been revived last week.

Monday’s sight deposit data was widely interpreted as suggesting up to CHF2.4BN of foreign exchange intervention in the week to December 10, although the policy-important EUR/CHF rate still declined slightly for the period and remained close to its recent multi-year lows on Tuesday following a more than 4% decline this quarter.

“This was the biggest weekly change since the middle of May, and coincides with EUR-CHF attempting to break below 1.04 for the first time since 2015 and the aftermath of the EUR-CHF currency peg removal,” says Dominic Bunning, head of European FX research at HSBC.

“The speed of the move has probably been more concerning than the specific level for the SNB,” Bunning also said, writing in a Tuesday briefing.

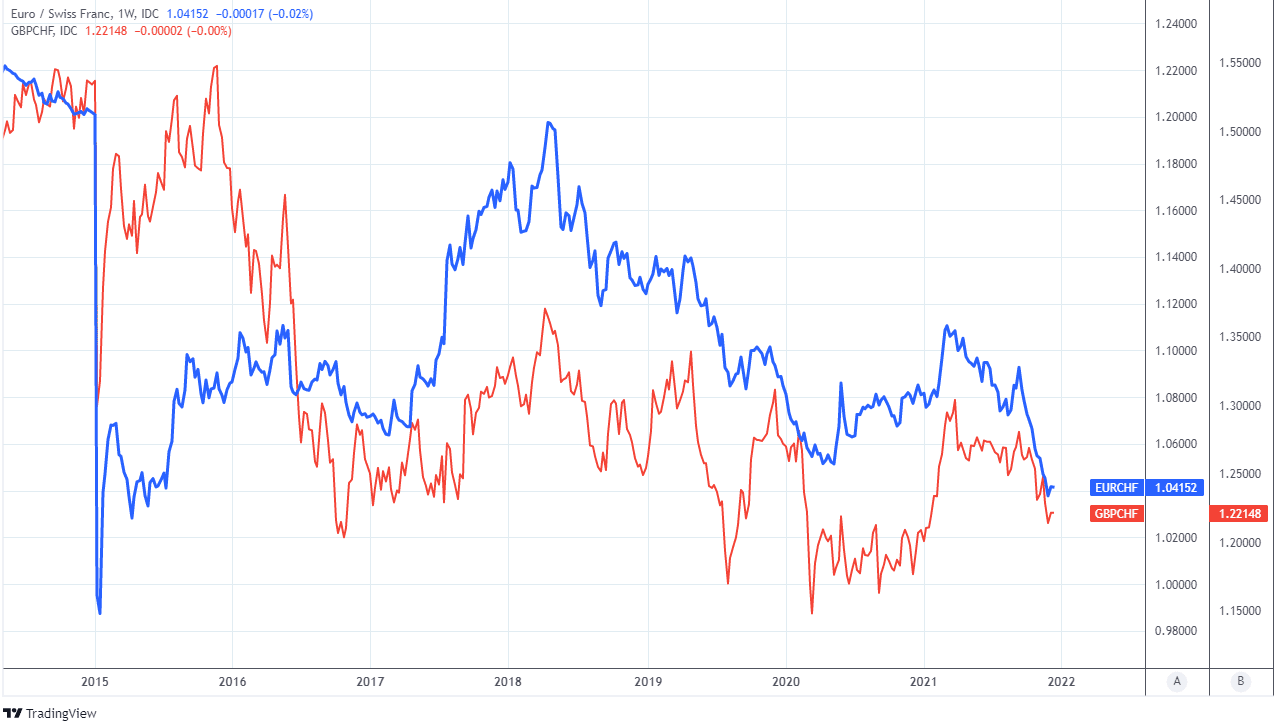

Above: EUR/CHF shown at weekly intervals alongside GBP/CHF.

- Reference rates at publication:

GBP/CHF: 1.2188 - High street bank rates (indicative): 1.1760-1.1850

- Payment specialist rates (indicative: 1.2078-1.2127

- Find out more about specialist rates, here

- Set up an exchange rate alert, here

- Book your ideal rate, here

The SNB had previously appeared to eschew intervention earlier in the final quarter even after the EUR/CHF pair slipped beneath its 2020 crisis low around 1.05, a level that drew large intervention from the SNB last year, in the middle of this November.

That took many in the market by surprise at the time but now the bank has effectively signaled its concern it could have implications that frustrate, if not largely prevent further falls in USD/CHF over the coming weeks in the absence of a Euro-Dollar recovery.

This is in part because declines in USD/CHF would reflect strength in the Swiss Franc that then exacerbates the downward pressure on EUR/CHF from falls in the Euro, which creates a dynamic where betting on declines in USD/CHF becomes the same as betting on an increase in EUR/USD.

The SNB announces its final quarter policy decision on Thursday and the market will be looking to its language about the Swiss Franc, although there will also be new economic forecasts and a likely confirmation that there’s still no prospect of a change in the -0.75% cash rate any time soon.

“Any shift towards even firmer language about the franc would bring greater intervention to the forefront of market thinking and could help to curb or even reverse some of the CHF’s gains over the last few quarters,” HSBC’s Bunning says.

Should USD/CHF find itself better supported over the coming weeks, or perhaps even rising, it would have the effect of slowing, halting or potentially even reversing the decline in GBP/CHF over the same period.

Thursday’s policy announcement comes on the eve of a decision from Switzerland’s federal government about whether to adopt a system of so-called vaccine passports or to return the economy to a state of all out ‘lockdown.’

“Simply put, the starting point for the Swiss National Bank's (SNB’s) final decision of the year should be an acknowledgement that downside risks have materialized to the Swiss economy on multiple fronts since the September decision,” says Geoffrey Yu, an FX and macro strategist at BNY Mellon.

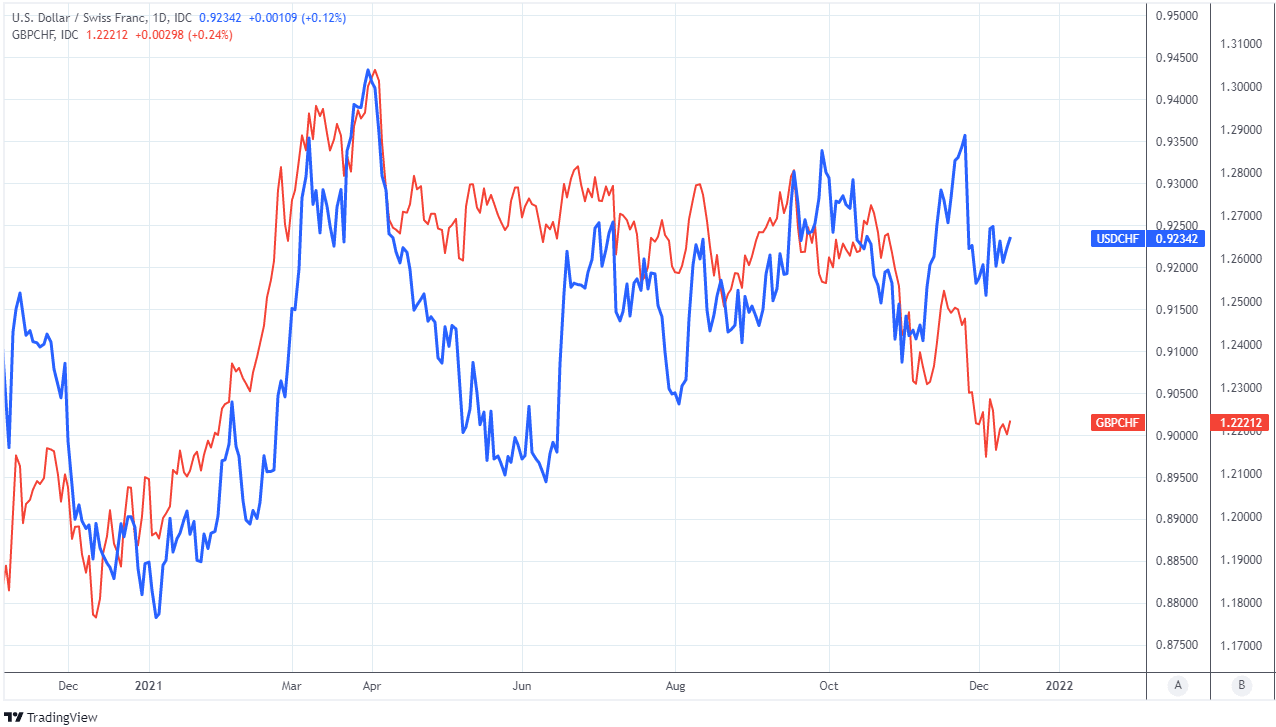

Above: USD/CHF shown at daily intervals alongside GBP/CHF.

“The focus for markets, as EUR/CHF slides gradually towards parity at the current rate, is whether intervention can be stepped up or whether additional measures can be introduced,” Yu wrote in a Tuesday morning briefing.

With some Eurozone economies already mired in varying degrees of renewed closure even before the SNB’s meeting, both domestic and international coronavirus developments have undermined the bank’s key September assumption that “rigorous containment measures will no longer be necessary.”

This could flatten what had been an upbeat tone at the SNB in September and likely necessitates what would be a second set of downgrades to economic growth forecasts this Thursday, all of which creates risk of further FX market interventions by the SNB for the coming weeks.

“As the dollar has managed to hold in a tighter range over the past quarter, the bulk of upward pressure on franc valuations will come from the euro,” says BNY Mellon’s Yu.

“The question is whether to wait until a new European Central Bank (ECB) strategy comes through after the Pandemic Emergency Purchase Programme (PEPP) is complete, or for the SNB to act on its own accord. Based on past form, the SNB will likely prefer the first option,” Yu also said.

The reason for the SNB’s intervention is that further strength in Swiss exchange rates, if not countered, would reduce future inflation rates that have already remained close to zero for years and were also still expected by SNB to remain that way even when the economic outlook was much brighter.

September’s SNB forecasts had inflation peaking around 0.7% in 2022 before ebbing to 0.6% in 2023 and while these forecasts could rise in December’s update, such increases are unlikely to match the scale of those seen or expected in the Eurozone, U.S. and elsewhere.

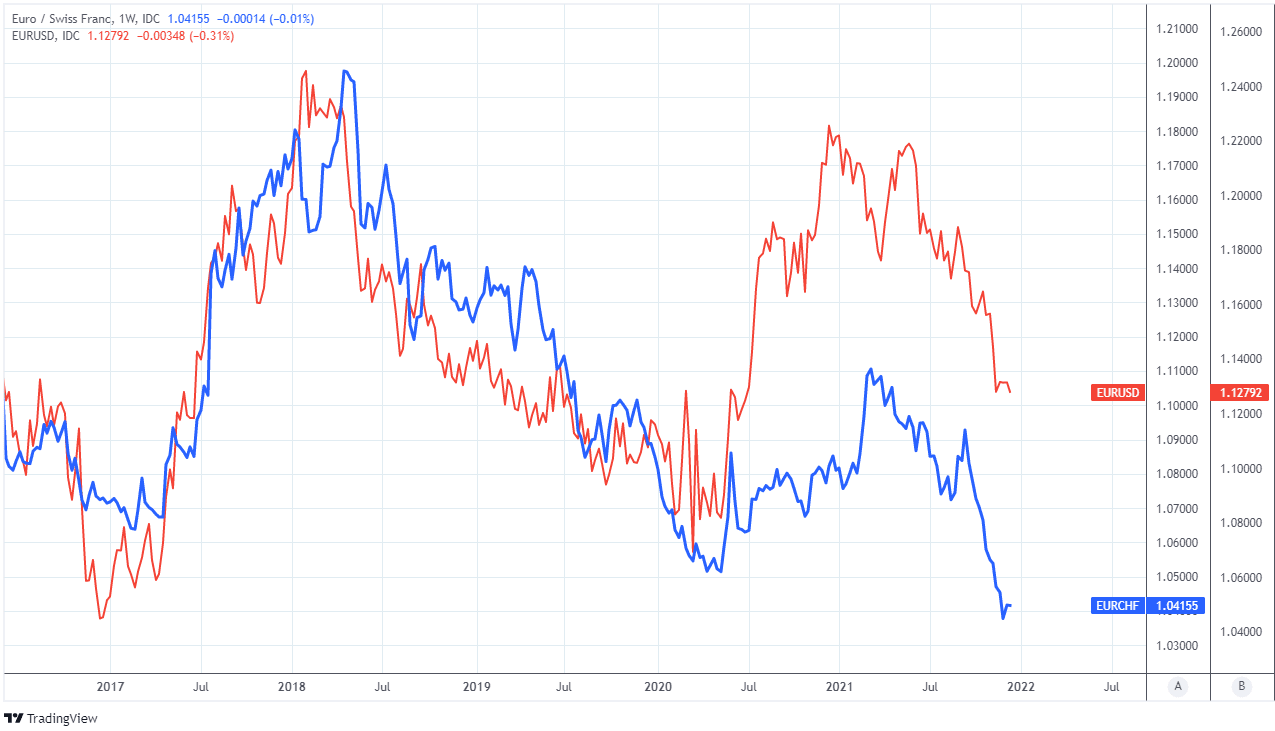

Above: EUR/CHF shown at weekly intervals alongside EUR/USD.