- JP Morgan warn there will be limits to the Canadian Dollar's performance

- Technical studies however suggest further CAD strength is likely

- "Odds are stacked heavily towards additional GBP losses in the weeks ahead" - TD Securities on Pound v Canadian Dollar.

The past month has seen a dramatic change in policy by the Bank of Canada which as in turn prompted a sharp rally in the Canadian Dollar.

From a previously dovish stance, in which the Bank favoured keeping interest rates low, the Bank has suddenly turned around and raised interest rates from 0.50% to 0.75% at this week’s policy meeting.

This has led to a rise in the Canadian Dollar against all major counterparts as higher interest rates tend to attract greater inflows of capital from foreign investors seeking a higher return from their money.

Just over month ago, the dominant policy framework at the BoC was one of lingering cautiousness given the labour market was still showing signs of underemployment, exports were underperforming and the economy was showing a lack of wage growth and inflation.

The about-turn was signalled in comments from BoC deputy governor, Carolyn A Hughes, who said that the time for continuing ultra-low interest rates was coming to an end.

After this week’s rate rise, markets have grown confident more hikes are in the pipeline.

“Rates markets went from pricing in one hike before end-2018 a month ago, to pricing in three. This re-pricing drove a 45bp narrowing of US-CA 2y yield spreads, and a concomitant 5.7% decline in USD/CAD,” says Daniel P Hui at JP Morgan.

Low wage growth, inflation and underemployment remain obstacles to further interest rate hikes, but their influence is expected to be shortlived.

“Conviction that recent disinflation was to a large extent transitory on technical factors; (b) strong confidence in output gap closure estimates; and (c) conviction that projected output gap closure would nudge inflation back to target,” supported the outlook for monetary policy and the currency.

Hui points out that BoC is a rare example of a central bank basing its policy expectations on an ‘old normal’ model which contrasts with ‘new normal’ which expects lower rates for longer.

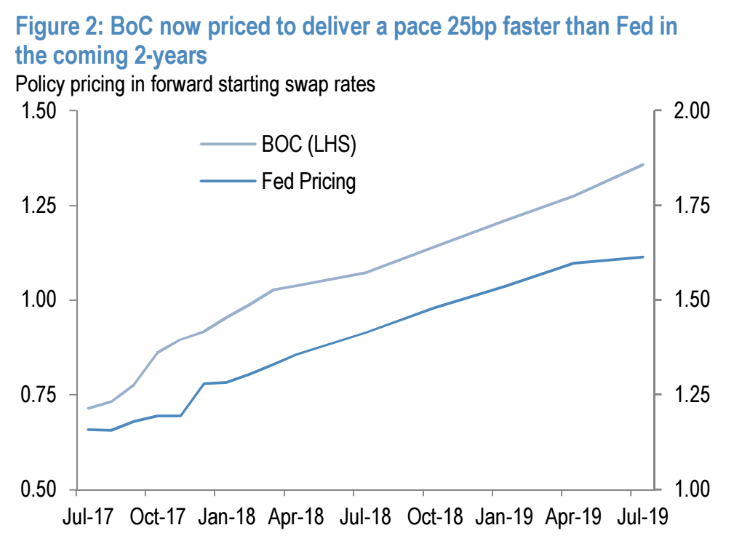

Expectations are more hawkish at BoC compared to the Fed despite US data outperforming CAD data.

“The priced policy approaches here look particularly polarised and stretched versus the US: the priced Fed curve is extremely flat in-part because of concerns that recent US disinflation might derail the Fed from delivering its three-yearly hikes signaled in the dots,” said Hui.

In short, markets are pricing in more rate hikes in Canada than in the US.

“In Canada, despite inflation running even lower than target (1.3 vs 1.4 US core PCE) and a positive, rather than negative output gap, markets are now pricing in one more BoC hike than Fed hikes in the coming two years,” says Hui.

Eventually, however, “policy framework re-convergence” should trim CAD outperformance.

Get up to 5% more foreign exchange by using a specialist provider. Get closer to the real market rate and avoid the gaping spreads charged by your bank for international payments. Learn more here.

“Revised forecasts anticipate mean-reversion higher from these depressed levels in the coming quarters,” says Hui.

JP Morgan argue downside is limited for USD/CAD, which translates as upside being limited for CAD.

CAD is now too overstretched to make more gains, especially versus the Dollar, and if anything USD is more likely to catch up or CAD to fall when USD’s stronger fundamentals eventually shine through.

“Assuming the underlying cyclical mechanics of inflation between the US and Canada are not that different, there will need to be some convergence between what is priced for BoC and the Fed: Either BoC pricing shows less confidence due to ongoing undershooting of inflation and/or growth sensitivity to higher CAD rates; or, US inflation bounces reaffirming a Phillips curve relationship and allowing the re-pricing of some of the Fed dots. This limits further downside in USD/CAD and biases some mean reversion higher,” says JP Morgan’s Hui.

Based on their expectations that the two monetary policy frameworks will “converge” JP Morgan forecast a retracement in USD/CAD back to 1.30 by year-end.

This would be followed by further retracement, “to 1.34 by mid-year (2018) on expected weakness in crude prices, and some skepticism about how far and quickly BOC normalization can proceed.”

The Charts Tell Another Story

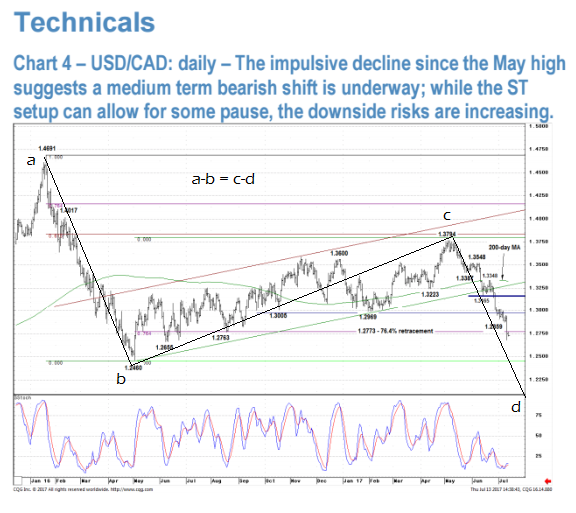

Unfortunately for Hui’s elegant analysis, the chart’s tell a different story, suggesting more CAD strength, at least in the short-medium term.

For USD/CAD, the recent breakdown below the important 1.30/1.2970 support zone was a very bearish sign.

“Moreover, the follow-through weakness below the next zone of key support levels in the 1.2775/1.2760 zone, which includes the 76.4% retracement from the May 2016 low affirms the downside bias,” adds Hui.

Nevertheless, one positive for US Dollar Bulls is that the recent bout of weakness has left short-term conditions oversold, increasing the risk of a consolidation phase.

“However, corrective retracements are viewed as selling opportunities.”

And, “Near-term retracements should find resistance at the 1.2800/10, before the 1.2860/90 zone.”

Our own view is that the pair is forming a large abcd pattern with an incomplete c-d wave down, which will probably still fall further and target in order to fulfil wave equality with wave a-b.

The Pound Should Also Continue to Lose Ground

The GBP/CAD is also locked in a technical downtrend.

"Sterling retains a heavy undertone. Intraday charts show price gaining modestly from just under the 1.64 area currently, near last week’s low, but this only follows a significant drop in the market earlier in the session from a little above 1.66 which puts a broadly negative spin on short-term price action," says Shaun Osborne at TD Securities.

TD Securities note the GBP is struggling to regain 1.6550 consistently (formerly retracement support), the daily bear channel remains intact and that trend oscillators remain bearishly aligned on the short, medium, long and ultra-long term studies.

"This will allow for very limited counter trend corrections and suggests to us that odds are stacked heavily towards additional GBP losses in the weeks ahead. We think a full retracement of the H1 2017 rally toward 1.60 remains likely. Fade minor GBP gains," says the analyst.