Analysts at Barclays have updated clients with their latest forecasts for the Australian Dollar.

For those hoping for a stronger Australian Dollar, the news is not constructive and it would appear that the recent strong run could be about to fade and reverse.

The British-based bank has warned clients that the trajectory for the currency is likely lower.

“We see the AUD falling gradually against the USD in 2017,” says Marvin Barth, a foreign exchange analyst with Barclays in London. “Although improving domestic fundamentals and a less dovish RBA should provide support for the AUD, external factors are likely less favourable.”

Barth cites China’s plans to curb property speculation and informal sector credit growth as two indications that the Chinese pedestal that has for so long supported the Aussie is being shaved.

Furthermore, China aims to run a ‘less easy’ monetary policy which also suggests the support for commodities could wane.

Australia's two biggest exports are iron ore and coal, both of which are largely destined for the Chinese market.

The commodities research team at Barclays believe that the price rally in iron ore is not sustainable and forecast prices to fall to the mid-$50s/t in H2 17.

This week we also reported that analysts at Macquarie bank warned that the outlook for iron ore was softening based on their surveys of the commodity trading community.

However, Macquarie’s view on the outlook facing the iron ore sector remains rather upbeat and makes for an interesting contrast to the view forwarded by Barclays.

“Iron ore restocking appears to be easing, as steel mills look well covered for their forthcoming ramp-up in steel output. Steel mills are not yet planning to cut iron ore purchases, however, and iron ore prices should continue to be supported while steel prices remain elevated,” say Macquarie.

Australia’s Superior Interest Rate is Being Challenged

The final reason to expect a softer Aussie Dollar profile lies with the Australia-US yield differential, which should continue to narrow in 2017, thus reducing support for the Australian currency.

Australia’s interest rate profile has for many years now been superior to that of the US, UK, Eurozone and Japan - nations which have all slashed interest rates to record-lows over recent years.

While the Reserve Bank of Australia has also embarked on a programme of cutting rates in response to soft inflation over recent years the cuts have been nowhere near as sever as elsewhere in the developed world.

This creates a scenario whereby it is cheap to borrow in currencies such as the Dollar, Euro, Pound and Yen and invest in Australian-based assets that offer higher returns. This in turn drives demand for the Australian Dollar.

But with the US Federal Reserve starting to raise interest rates again, the gap is being closed and the support for the Aussie Dollar from this sector is likely to slide.

“Taking into consideration our forecast of two more Fed rate hikes this year while the RBA remains on hold – historically, AUDUSD has more often than not moved in the direction of yield differentials,” says Barth.

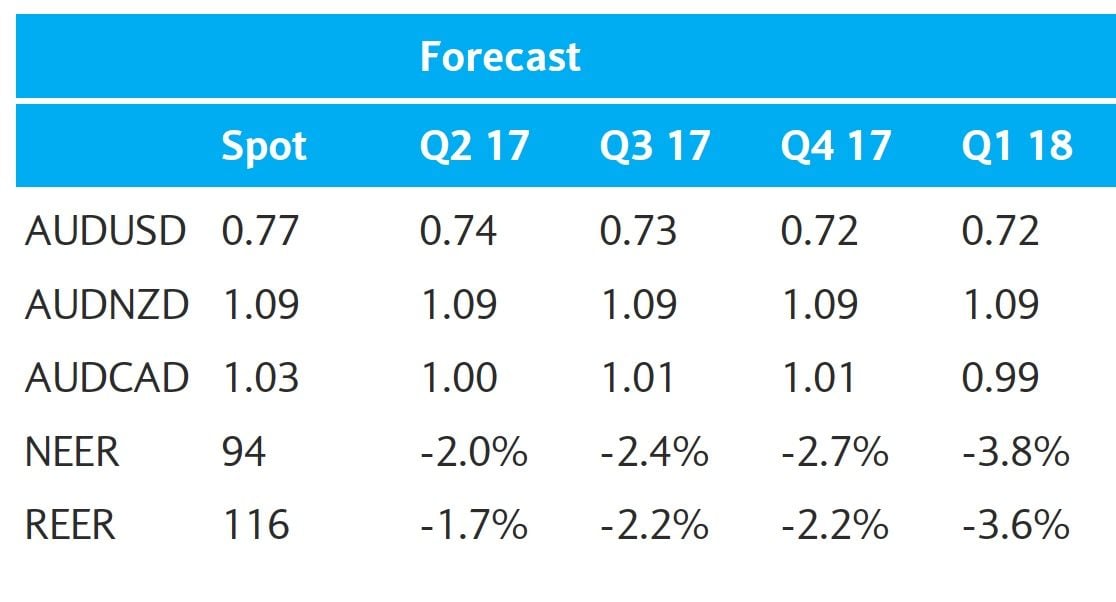

Below are the latest Australian Dollar forecasts offered by Barclays for 2017 through to early 2018.