Image © Desiree Caplas, Adobe Stock

- AUD advances after GDP growth meets expectations for second-quarter.

- But economy only saved from contraction by Gov spending and exports.

- Consumer spending weak amid serious trade war threat to AU exports.

- More RBA interest rate cuts and weak AUD key to economic outlook.

- AUD tipped to lose steam on rising threat to domestic and global growth.

The Australian Dollar was riding high against most of its G10 counterparts during the morning session Wednesday after official data appeared to show the economy recovering its poise in the second quarter, although some analysts say there is trouble ahead and that nascent gains won't last long for the Aussie.

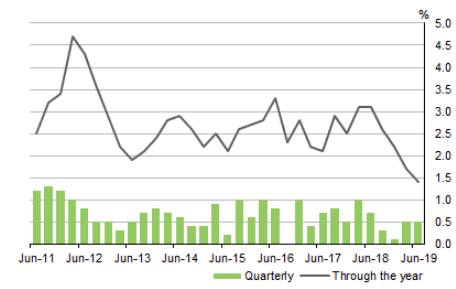

GDP growth was 0.5% for the second quarter, the Australian Bureau of Statistics (ABS) says, which was unchanged from the upwardly-revised pace seen in the prior period but in line with the consensus. However, this left the expansion running at an annualised 1.4% for the quarter, the slowest pace of growth since the financial crisis.

Furthermore, Wednesday's number was lower than the Reserve Bank of Australia (RBA) suggested just a month ago that it would be. The RBA had said that growth would be "firmer" in the recent quarter than it was previously while its official forecasts were looking for quarterly and annualised numbers of 0.75% and 1.7% respectively.

"Amid a modest rise in household consumption (0.4%) and a further fall in dwelling and business investment, domestic demand was saved only by the strength of public spending. Stripping out public demand shows another contraction in private final demand (-0.1% q/q) for the fourth consecutive quarter, taking y/y negative (-0.3%) for the first time since Q3 2009," says Elsa Lignos, head of FX strategy at RBC Capital Markets.

Above: Australian GDP growth rates. Source: Australian Bureau of Statistics.

Government spending, household consumption and exports all contributed positively to growth in the recent quarter while investment from both the public and private sectors detracted from the expansion, the ABS says. The rub for the economy going forward is that government spending can only provide so much support up ahead and there's a litany of risks that could easily see consumer spending and exports weaken from current levels.

"It seems unlikely that the labour market can remain quarantined from the weakness in the economy. The slowdown in GDP and domestic demand growth points to sharply slower employment growth. If this proves to be the case, the downside risks to the economy would increase," says Felicity Emmett, an economist at ANZ. "Ultimately, the Q2 GDP data confirm that the economy needs more stimulus to generate stronger growth, lower unemployment and inflation consistent with the RBA’s 2-3% target band."

Emmett says the second quarter likely marks a cycle low for Australian GDP but growth but that the economy will remain in a moribund condition for a while yet, which means a pick-up in the pace of expansion could be a long way off. She says a weak growth pulse will force the RBA to cut its interest rate for a third time before long.

The RBA cut the cash rate by 25 basis in both June and July, leaving it at 1%, in an effort to lift inflation by stimulating the economy with lower borrowing costs. It said last week it would like to see an “accumulation of additional evidence” that more stimulus is necessary before acting again and since then retail sales figures for July have surprised on the downside. So too have construction output numbers and markets are now coalescing around the idea of a third 2019 cut coming in October.

Above: AUD/USD shown at hourly intervals, alongside GBP/AUD (orange line, left axis).

"There are powerful structural headwinds from weak wages growth and productivity, constraining consumer spending. The global economy is slowing and downside risks have intensified as the global trade and technology war escalates," says Andrew Hanlan, an economist at Westpac. "Stimulus (tax cuts and interest rate cuts) will provide a boost to activity – but given the weak starting point and the powerful headwinds – the risk is that growth remains below trend over the remainder of 2019 and through 2020."

Governor Philip Lowe said Tuesday the board will monitor developments "including in the labour market" closely over the coming months and adjust its policy settings if necessary. The comments marked a departure from the RBA's earlier message that it would simply take its interest rate cues from the labour market, which has seen uemployment rise 30 basis points to 5.2% since May. The new guidance could mean the RBA also considers the rate of GDP growth as well as other factors.

Westpac forecasts the RBA will cut its cash rate again in October after it becomes apparent that even its latest downgraded growth forecasts are still too optimistic for the Aussie economy. The RBA's current projection for 2019 GDP growth is 2.5% but after two quarterly expansions of just 0.5% each, the economy has a long and uphill climb ahead of it if the forecasts are to be met.

Above: AUD/USD shown at daily intervals, alongside GBP/AUD (orange line, left axis).

"We anticipate the rally in AUD will run out of steam," says Kim Mundy, a strategist at Commonwealth Bank of Australia. "Without the recent lift in export volumes and a low AUD assisting net exports, if the government had cut back on consumption expenditure, the Australian economy would have contracted in Q2. AUD needs to remain heavy to assist net exports and absolute growth in Australia's economy."

Australia's economy is slowing following a bust in the housing market that's driven prices lower in all of its major cities in the last year. Although some parts of the market are now stabilising, the downturn has already mothballed many projects and some fear it could yet have more of an impact on the jobs market. Meanwhile, the U.S-China trade war has continued to escalate, further threatening Australia's China-facing and commodity-exposed economy.

President Donald Trump went ahead Sunday with a new 15% tariff on another $112 bn of goods imported from China each year, which takes the total value of Chinese exports now covered by punitive levies above $360 bn, although there's still a further $190 bn worth of tariffs scheduled to take effect on December 15. China has retaliated with a tariff of its own on around $75 bn of imports from the U.S., although its capacity to respond is constrained by the fact it has a significant trade surplus with the U.S.

The U.S. and China have been warring with tariffs and other policy tools over the latter's "unfair" trading practices since the first quarter of 2018 and with the White House facing an election year in 2020, it's under pressure to secure a victory and cannot afford to lose face in the conflict. Global trade, not to mention economic growth, has already fallen as a result of the uncertainty thrown up by the conflict but many now anticipate further weakness ahead.

Time to move your money? Get 3-5% more currency than your bank would offer by using the services of foreign exchange specialists at RationalFX. A specialist broker can deliver you an exchange rate closer to the real market rate, thereby saving you substantial quantities of currency. Find out more here.

* Advertisement