Image © Adobe Images

- AUD slips as markets turn defensive and construction data hurts.

- Ailing construction sector sees markets eye capex and GDP figures

- Downside capex surprise to hurt GDP, upside surprise may lift AUD.

- Figures matter for RBA policy, come as charts point to clouded outlook.

The Australian Dollar was on the defensive Wednesday after official data revealed a larger-than-expected fall in construction sector output for the second quarter, which has put forecasts for economic growth at risk of downgrades.

Australia's Dollar was weaker in tandem with other exchange rates and financial markets in general Wednesday but the bulk of losses came shortly after 0.2:30, when the construction data was released, and it's the economic figures that have caught the eye of analysts.

Output from the construction sector fell by 3.8% on a seasonally-adjusted and annualised basis in the second quarter, deepening a revised 2.2% slump from the prior period and marking a fourth consecutive quarter of contraction. Economists and markets had looked for only a 1% decline.

"The data suggests that there will be a sizeable fall in dwelling construction in Australia’s Q2 real GDP. Our early estimate of Australian Q2 real GDP of 0.6%/qtr risks being revised lower. The construction work done data, combined with tomorrow’s Q2 capex data will give a good reading on how Australian business investment has tracked in Q2," says Kim Mundy, a strategist at Commonwealth Bank of Australia (CBA).

Above: AUD/USD rate at 4-hour intervals, and Pound-to-Australian-Dollar rate (orange line, left axis).

The fall in output resulted from declines in both residential and non-residential building, Australian Bureau of Statistics data shows, which is coming at the tailend of an 18-month long decline for house prices in Australia's main cities.

Fears among policymakers always were that lower house prices would lead to less construction activity, higher unemployment and threats to growth. They've also feared that lower prices will hurt household confidence and depress consumer spending, which has been weak at the retail level for a while.

All of those fears have crystalised into reality to at least some degree in recent months although some say Aussie construction output should stabilise soon and the full extent of the economy's plight is not yet known. The data due out over the coming week will help to remedy that.

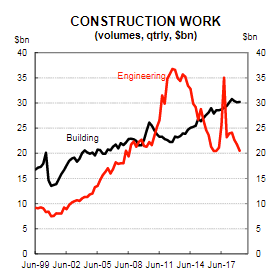

"The good news is that building approvals appear to be plateauing out. With the housing market starting to strengthen again we could see approvals begin to lift again later this year," says Kristina Clifton, an economist at CBA. "The wind down in the construction phase of major LNG projects has weighed on private engineering work done for many years. We are just about at the end of that process now, with engineering work looking to be plateauing."

Above: CBA graph showing Australian building work done Vs engineering work.

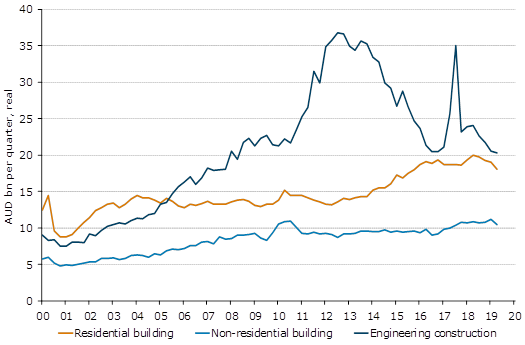

"The contraction in residential activity accelerated, non-residential building activity dropped across both private and public sectors, and the weakness in engineering construction persisted, with only a small uptick in public sector work done. Consequently, construction activity will detract even more from GDP growth in Q2," warns Catherine Birch, an economist at ANZ.

The data matters to markets because it has implications for GDP growth and inflation in the second quarter. Both of those are important for the Reserve Bank of Australia (RBA) interest rate outlook, which is typically the most significant driver of Australian exchange rates. However, the figures in question cover the three months to the end of June only and therefore, relate to a period that was mostly before the RBA began cutting its interest rate.

The RBA cut the cash rate by 25 basis in both June and July, leaving it at 1%, in an effort to lift inflation by stimulating the economy with lower borrowing costs. Changes in rates are normally only made in response to movements in inflation, which is sensitive to GDP growth, but impact currencies because capital flows tend to seek out the most advantageous or improving returns.

Above: ANZ Research graph detailing output from various sub-sectors of construction industry.

Wednesday's data comes just hours ahead of the capital expenditure figures for the second quarter and a week out from the all-important GDP growth number for the same period, both of which will cast a light over just how much the economy was struggling before the RBA came to the rescue.

"The upswing in private business investment has waned in the last few quarters driven by some moderation in plant & equipment spending. Continued tepid capital imports suggest a continuation of this trend in Q2," says Elsa Lignos, head of FX strategy at RBC Capital Markets. "We look for a 0.8% rise in total capex in Q2 and will be watching closely the 3rd estimate of capex plans for 2019-20. Early estimates have been disappointing."

Consensus is looking for a 0.4% increase in private capital expenditures during the recent quarter, which means the Aussie could benefit if Lignos is right in tipping a 0.8% increase. That data is out at 02:30 on Thursday morning and the GDP GDP figure are due in the early hours of Wednesday, 04 September but analysts will remain tight-lipped on their expectations for the latter until this week's figures are published, because those will impact the business investment component of GDP.

Above: AUD/USD rate at daily intervals, and Pound-to-Australian-Dollar rate (orange line, left axis).

Financial markets have long anticipated another Aussie slowdown this year because the global economy has been hurt this year. And the current global economic cycle was already considered mature and vulnerable even before global growth became threatened by the U.S.-China trade war, which has now got analysts, economists and financial markets fearing a recession in the U.S. as well as trouble elsewhere.

Australia's commodity-dependent and Asia-exposed economy could be disproportionately impacted by a global downturn that has the U.S. and China at the centre of it. This is part of the reason why the RBA has already cut the cash rate twice and is also why financial markets still expect it to cut again on a further two occasions.

That has weighed on the Australian Dollar, which has been tipped for more modest losses into the first quarter of next year as the RBA brings its cutting cycle to an end but the capex and GDP figures might help give the currency a lift if they paint the economy in a light that's not quite so dim as markets currently imagine. They will be released as the technical outlook for the Aussie on the charts is turning clouded.

"AUD/USD has recovered back into its range. Caution is warranted as we have 13 counts on both the daily and weekly charts and TD support at .6574/35. We have tightened the stops on our short positions. The intraday Elliott wave counts are negative for now. Rallies will need to regain the .6832 June low as an absolute minimum in order to alleviate immediate downside pressure," says Karen Jones, head of technical analysis at Commerzbank.

Time to move your money? Get 3-5% more currency than your bank would offer by using the services of foreign exchange specialists at RationalFX. A specialist broker can deliver you an exchange rate closer to the real market rate, thereby saving you substantial quantities of currency. Find out more here.

* Advertisement