Pound Sterling Supported, GDP Data Beats Expectations at Start of Eventful Week

- Written by: Gary Howes

Image © Adobe Stock

UK economic growth data came in stronger than analysts were expecting when released on Monday, offering the Pound some sideline support at the start of what promises to be a pivotal week.

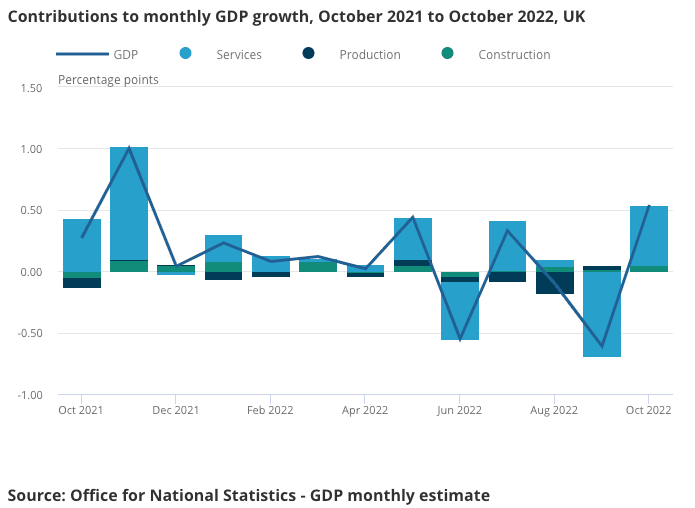

This week's UK data docket started with the release of GDP data that confirmed the economy grew 0.5% in October, ahead of expectations for a 0.4% increase and making for a strong recovery from September's -0.6%.

Monthly GDP is now estimated to be 0.4% above its pre-coronavirus levels of February 2020.

September's 0.6% decline was largely the result of the extra bank holiday for the State Funeral of Queen Elizabeth II, where some businesses may have closed or operated differently on this day, said the ONS.

The services sector grew by 0.6% in October 2022 and was the main driver of the growth in GDP.

Output in consumer-facing services grew by 1.2% in October 2022, after falling 1.7% in September 2022 and 1.6% in August 2022.

Pound Sterling was steady in the wake of the numbers with the Pound to Euro exchange rate quoted at 1.1628 and the Pound to Dollar exchange rate at 1.2270, which brings it closer to the multi-week highs at 1.2345.

Compare Currency Exchange Rates

Find out how much you could save on your international transfer

Estimated saving compared to high street banks:

£2,500.00

Free • No obligation • Takes 2 minutes

But the UK economy risks registering a recession as GDP fell by 0.3% in the three months to October 2022 compared with the three months to July 2022. However, this was better than the -0.4% figure the market was anticipating.

It would require a strong November and December to ensure the economy avoids contraction in the final quarter of 2022, as a technical recession requires two consecutive quarterly declines.

The manufacturing sector was another bright spot as output increased 0.7% in the month to October, up from 0% in September and better than the 0.1% expected.

Elsewhere, the repair of motor vehicles and motorcycles was a particularly strong contributor said the ONS as it grew by 1.9% in the month following a fall of 2.0% in September 2022.

This as demand for new cars remains subdued; the Society of Motor Manufacturers and Traders reported new registrations for September 2022 were only 4.6% above September 2021, which was the weakest September since 1998.

Another area of strength was provided by health activities and a rise in cCovid testing and vaccinations for the second consecutive month because of the autumn booster campaign.

"Despite this positive outlook from the monthly growth figure, there are still strong downside risks to GDP in the fourth quarter of this year due to high inflation and interest rates – which continue to suppress demand – and supply chain disruptions, as well as work backlogs due to industrial action and a tight labour market – which continue to weigh on business growth. We still expect GDP to remain flat in the fourth quarter of this year," says Paula Bejarano Carbo, NIESR Associate Economist.

Ellie Henderson, an economist at Investec, says the economy should avoid slipping into a technical recession.

She says the economy will struggle in December, especially considering the output that will be foregone due to industrial action across the month; estimates suggest one million working days will be lost to strikes in December.

"Despite this, we forecast that the economy will be able to eke out growth in Q4 and avoid a technical recession this year," she adds.

The GDP data is relatively dated and foreign exchange markets will likely prove more responsive to Tuesday's wage and employment figures and Wednesday's all-important inflation data.

These cover the November period and come as the Bank of England starts to debate raising interest rates ahead of their decision which is due Thursday.

But it is data and events in the U.S. that will likely determine how the Pound flares this week.

All-important U.S. CPI inflation figures are due on Tuesday, followed by the Federal Reserve's interest rate decision midweek.

The outcome could determine whether the Dollar's recent pullback extends or whether it snaps back in recovery.

These events will influence global market sentiment and, as we have noted on numerous occasions, this is a critical ingredient in Sterling's performance and will likely determine where it ends the year.

(If you are looking to protect or boost your international payment budget you could consider securing today's rate for use in the future, or set an order for your ideal rate when it is achieved, more information can be found here.)