SNB Tipped to Drop its Defence of the Swiss Franc

Although the Swiss National Bank (SNB) famously gave up defending its EUR/CHF floor at 1.20 last January, it was not long before it began to regularly intervene in foreign exchange markets again to weaken its own currency in order to support Swiss exports.

The need to keep the currency competitive is compelling as Swiss exports continue to suffer.

In February 2017 the official Swiss watchmaker's federation reported that exports of Swiss watches was down a further 10% on a year ago. In fact 2016 was the worst year for the industry since 2008 when the financial crisis took place with many blaming the persistently expensive Franc as a contributing factor.

But defending the export base of Switzerland comes at a cost for the SNB and is hardly sustainable over the long-term and has lead to some analysts warning an end to intervention is on the horizon.

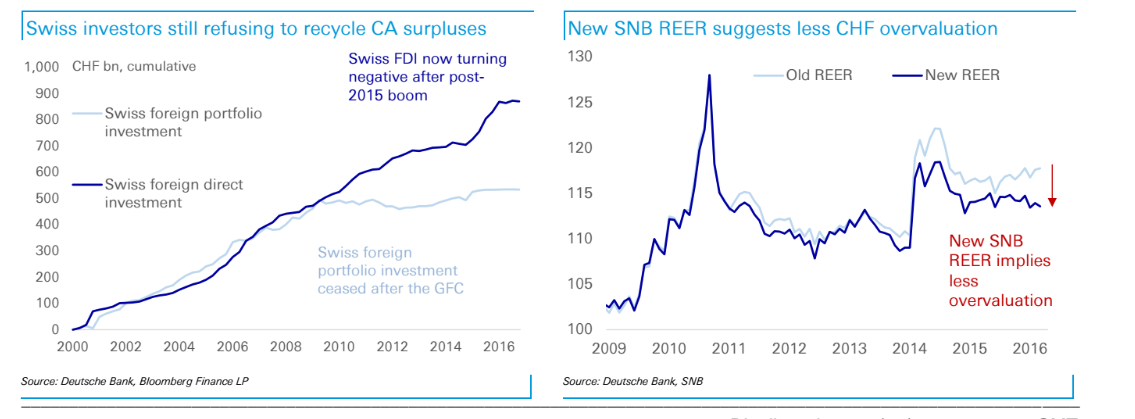

Besides the cost element of the market operations there is also an argument against agressive intervention to be made on the changing nature of Swiss trade and a recent re-assessment of the currency as less overvalued than previously thought.

Research by SNB staffers suggest the currency is not as overvalued as previously thought, and this analysis may prompt a revaluation and provide support to insiders who wish to put a stop to the SNB manipulating its currency lower.

An increasing shift in trade to stronger Asian currencies appears to have changed the inputs into models which had previously concluded CHF is overvalued, and lessened the overvaluation.

“The SNB may not resist indefinitely. Last week, a SNB research paper tacitly revised the assessment of franc overvaluation. The staffers re-weighted the broad exchange rate index to reflect the recent shift in Swiss trade from low-inflation Europe to high-inflation Asia. This means that Switzerland has deflated more against her trading partners than the old indices suggested. As a result, the real broad exchange rate has depreciated significantly more since 2011 than the SNB would have assumed previously,” says Deutsche Bank’s Robin Winkler.

EUR/CHF to Descend

Despite the new analysis, a removal of supportive intervention in the EUR/CHF, will still likely cause significant weakness in the exchange rate.

The main driver behind CHF strength is Swiss investor aversion to investing in foreign financial markets, preferring their own domestic markets instead, and this tends to inhibit outflows, prevent the ‘re-cycling of surpluses’ and therefore demand for other currencies, leading to more net Franc appreciation.

Part of the problem is that many Swiss investors see too high a currency risk from non-Franc investments, given the Franc’s propensity to rise.

“Their home bias is unlikely to recede as long as the perceived FX risk in investing abroad remains negatively skewed. And to the extent that fears of another floor break prevent current account recycling, they risk becoming self-fulfilling,” says the Deutsche analyst.

Wilkins does not agree with those who are optimistic pressure on EUR/CHF will subside if Le Pen loses the French elections, as he sees the lack of demand from Swiss investors for foreign securities as the main driver.

“Many investors see safe-haven inflows as the main pressure and thus expect it to subside if Le Pen loses the French presidential election. We disagree,” said the analyst.

Nevertheless, many in the market expect a significant rebound in EUR/CHF if Le Pen loses due to the combination of the fall in safe-haven flows and the appreciation of the Euro ‘on its own’ due to the less risky political outlook.

Several analysts have pointed out how the Euro is undervalued due to the exaggerated discounting of political risk, and if Le Pen were to lose it would substantially remove that weight.

Meanwhile, traders may wish to keep their eye on the EUR/CHF for signs of the SNB withdrawing their support, which would make the pair susceptible to swift declines to below parity.

Also expecting strength in the Franc are analysts at DNB Markets.

Analysts from the Norwegian investment bank have this week written to clients warning of increasing risk of SNB adjusting policy, either by interest rate cut, exemption threshold or scaling back on interventions

"Pressure on the CHF remains, despite negative rates and interventions. We expect to see SNB scaling back intervention as balance sheet risks rise, and let the CHF strengthen somewhat more," say DNB.