Euro Exchange Rate Complex Could Only Bottom in December

Following a torrid week for the Euro we ask whether there is much downside remaining for a currency that has over recent months shown it is immune to prolonged periods of weakness.

- Euro to Dollar exchange rate today (24-10-16, markets closed): 1.0875

- Euro to Pound exchange rate: 0.8901, Pound to Euro: 1.1224

- Euro to Swiss Franc exchange rate: 1.0814

- Euro to Australian Dollar exchange rate: 1.4263

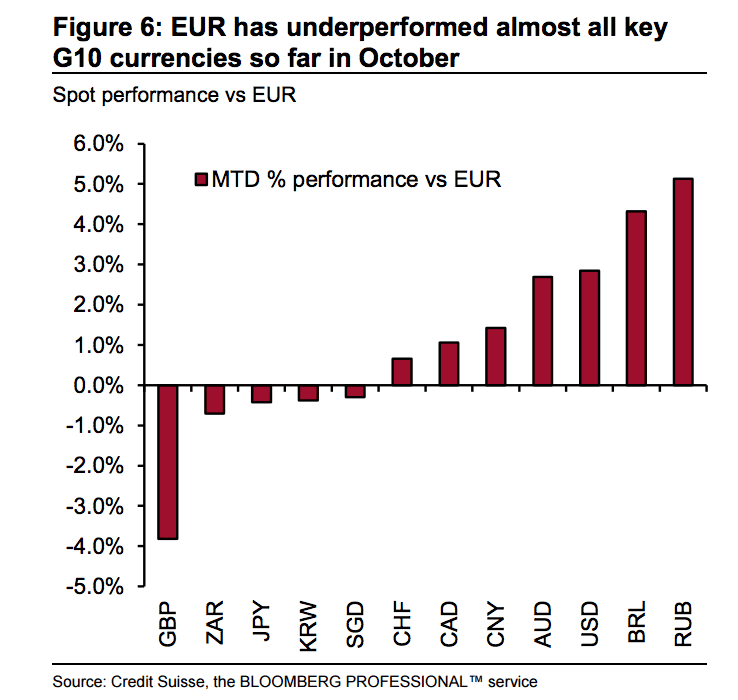

The Euro exchange rate complex underperformed notably during the week 17-21 October - only the Swedish Krona and Candian Dollar underperformed the Euro against the Dollar.

This is surprising for a currency that has throughout 2016 shown it is stubborn to prolonged bouts of weakness.

EUR/USD is trading at a seven-month low, below the 1.0915 low set around the Brexit decision in June, EUR/GBP is meanwhile trading at a two-week low at 0.8901.

However, the month of October sees the shared currency continue to outperfirm the Pound with the latter having more work to do if it is to better the Eurozone's shared currency this month:

Our latest forecast concering the GBP to EUR pair suggests that further advances by Sterling are in fact possible over coming days.

The declines in the shared currency accelerated on Thursday the 20th despite the ECB providing no clear indication that additional easing is certain in the future at their October policy meeting.

“Our view is that the market is not listening to the ECB,” says Peter Rosenstreich, head of market strategy at Swissquote Bank, “they hear the words but show no comprehension of their meaning”.

Rosenstreich describes the Euro’s reaction as being a ‘false negative’ who points out that over the past ten years, markets have become so conditioned to get currency debasing easing every time the inflation outlook deviates from the central bank’s target rate (in this case the ECB’s 2% target).

“Despite Draghi’s growing intellectual conflict, broader public disagreement on the effectiveness of the current monetary policy mix and the negative effect of distortion in financial markets, markets are still expected more easing,” says Rosenstreich.

The Swissquote analyst believes financial markets are simply projecting that the ECB must do something and that the action will be euro-negative, as the recent experience with the BoJ has shown currency traders.

2-year Eurozone-US spreads widened modestly after President Draghi poured cold water on the idea of that the ECB could reduce asset purchases.

Thomas Harr, Global Head of FICC Research at Danske Bank, observes positioning is not yet stretched short EUR/USD, which supports a greater role for relative rates.

“The political risks and relative monetary policy will weigh on EUR/USD where yesterday’s downside break of 1.0950 opens the door for further losses towards 1.0700-1.0850,” says Harr.

A decision on policy settings will be made in December and analysts agree that an extension of the programme beyond March of next year appears more likely than not, considering the ECB President noted that economic risks remain tilted to the downside while core inflation was showing no sign of a convincing recovery.

"Technically EURUSD’s breakdown below important support at 1.0952/13 – the 61.8% retracement of the December 2015/May 2016 rise and the June/July 2016 price lows – has reinforced an existing top and our bearish view. We look for further downside to 1.0826/22 next, then the January 2016 low at 1.0711," says a research note from Credit Suisse released following the ECB meeting.

Others are more bearish:

“We remain bearish on the outlook for the EUR. Fed-ECB policy divergence and weak seasonal trends for the EUR suggest 1.05 should be a fairly easy reach for the market into year end,” says Shaun Osborne at Scotiabank.

The Euro's Decline Won't Last, But Where is the Corner?

"There was nothing exceedingly dovish Draghi's comments and yet the lack of emphasis on the positive gave investors the green light to continue driving the currency lower. While we can't rule out a final flush to 1.08, we believe that EUR/USD is a near a bottom and expect it to find its way back to 1.10," says trader Kathy Lien at BK Asset Management who believes the Euro could enjoy a firm end to October.

Watch the PMI data due out Monday the 24th - this could be a trigger to a firmer currency.

However, others are looking for the turn around to only come towards year-end.

Longer-term, Swissquote's Rosenstreich believes the Euro will have to ultimately react to an impending realisation that central banks have reached their limit when it comes to boosting the economy.

“Negative rates were just a step too far for most people. It is only a matter of time before central banks accept the fact that they are not in total control, with Victorian-era precision, and realise that the cost of doing something does not outweigh the cost of doing nothing,” says Rosenstreich.

He argues that in 2017, financial markets will need to learn to live in a world were central banks no longer pretend to offer economic salvation.

“We see political risks in Europe as more EUR negative,” says Danske Bank’s Harr citing Spanish, German and French elections and of course Brexit negotiations dominating coming months.

But, Danske Bank say the EUR/USD will have bottomed in December and will head convincingly higher in 2017 on the large Eurozone-US current account differential and valuation.