The combined years of experience in central banking of the members of the US Federal Reserve tends to have an impact on the trajectory of the Dollar, according to a study from Danske Bank.

The level of experience at the Federal Open Markets Committee appears to matter to the Dollar - surprising as this may seem.

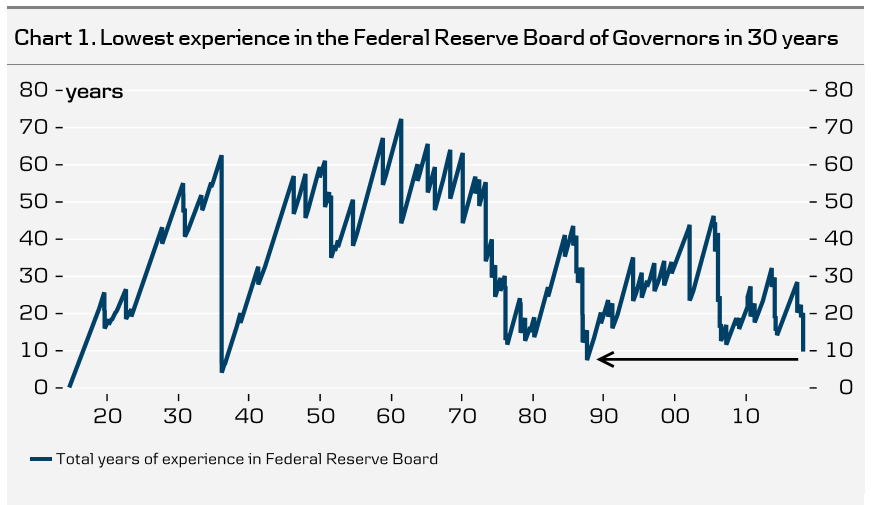

With the FOMC in transition, the new team appears to be one of the least experienced since the 1970's, and parallels between experience and Dollar performance might exist we are told by Danske Bank.

The new Chairman of the Federal Reserve, Jerome Powell, is not actually a banker but a lawyer by practice. Although he moved into banking during his career, his background is in law, and at the Federal Reserve, he was in charge of banking regulation before he was promoted to the job of Chair by President Trump.

He's not the only one on the Fed's board of governors who, according to Danske Bank, 'lacks experience, the other two current board members, Lael Brainard and Randal Quarles are also relatively inexperienced - at least when it comes to years spent in central banking anyway.

Quarles was only elected to the Fed in 2017 and Brainard in 2014.

Nevertheless, both have strong academic backgrounds, experience in finance and considerable terms of service working as 'mandarins' in the US Treasury.

Brainard has only been at the Fed for about five years, and altogether the members of the Fed's Board of Governors only have a combined experience-age of 10 years, which is the lowest since the Bretton Woods agreement in 1973.

To put it into perspective, the previous deputy chair of the Fed Stanley Fischer had, "30 years of experience from top posts in the World Bank, International Monetary Fund and Bank of Israel, before joining Federal Reserve," says Danske Senior Analyst Jens Nærvig Pedersen, and Janet Yellen joined the central bank in 1994.

The reason why all this should matter to FX markets is that the level of experience at the Fed appears to matter to the Dollar - surprising as this may seem.

Or so says research from Danske Bank anyway.

"We find evidence of a ‘Fed experience premium’ on USD over the period since 1973," says Danske's Pedersen, adding:

"For financial markets, the question is what a less experienced Federal Reserve will mean for the USD? To answer that question we have looked at the impact on the dollar index (DXY) from the level of experience in the Board of Governors in the post-Bretton Woods era (i.e. in the period since 1973). We find a significant positive effect on monthly data after taking into account the impact of monetary policy," he adds.

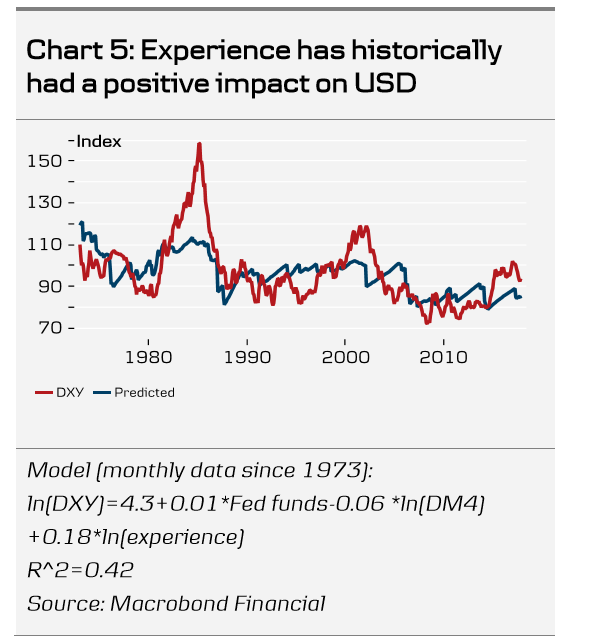

Below is a chart which illustrates the correlation between Experience and the Dollar Index:

Quite astonishingly, Pedersen finds a compelling correlation between the two sets of data, suggesting that the more experienced the Fed, the stronger the Dollar.

"A 1% gain in years of experience in the Board of Governors had led to about a 0.2% higher DXY," he concludes.

Why Experience Matters

Of course whilst it is one thing to say there is a correlation - or coincidence - between experience and the stronger Dollar it is quite another thing to say greater experience causes a stronger Dollar or less experience a weaker Dollar.

Yet Pedersen argues experience could be crucial in making certain key decisions which the chairman is faced with at the moment.

The first is about setting a suitable level for an inflation target, and the second the pace and volume of reductions in the Fed's balance sheet.

These challenges are highly technical and "in this respect, experience matters" says Pedersen.

"As an example, former chairman Ben Bernanke with his long resume on research and practice in monetary policy, was instrumental in pushing through the current inflation-targeting set-up," says the Danske analyst.

Mutiny on the FOMC!

Apart from experience, Danske cites another factor to do with Fed 'personnel' issues which could impact on monetary policy.

This issue relates to the number of people there are on the Fed Board of Governors.

The Board of Governors is made up of permanent staff on the FOMC and normally numbers 7 - the Chair, the two Vice-Chairs (one of Supervision) and the four Governors, however, currently there are only three members - Powell, Quarles, and Brainard, as the other empty posts have yet to be filled.

Why this should be an issue for monetary policy, is because of the composition and voting patterns of the Federal Open Market Committee (FOMC) which meets more or less monthly and decides on where to set the level of interest rates.

The voting core members of the FOMC are actually made up of the Board of Governors and the second set of officials called the President of the Fed Regions, who are Fed Presidents for selected regions in the US, and rotate to vote on policy amongst themselves on a year-by-year basis.

The Fed President voting group has five members and the Board usually seven, but right now only three.

The reason it could impact on the trajectory of policy is that the Board tends to vote as a collective whilst the Presidents show a strong tendency to dissent.

When there are seven Board members this is not a problem as the board still wins, but now there are just three, it could mean the Chairman and his executive team might get beaten.

"The balance of power within the Federal Open Market Committee (FOMC) shifts towards the Regional Federal Reserve presidents (which have been dissenting, while governors have worked by consensus) which have a total of five votes in the FOMC – a full Board of Governors would have seven votes," says Pedersen.

Another issue for the Board is that there will be more work to go around the three who are left as there are seven committees to chair and only three people to do it when previously each member would be a chair.

Finally, the Sunshine Act, which prevents members of the Fed from discussing policy in private could make things even more difficult for Powell as he won't be able to build a consensus behind the scenes.

"This is unlikely to be a lasting issue for the board, since some or all of the vacant seats likely will be filled during 2018, perhaps by striking a deal with the Democrats in order to smooth the approval process (the Senate Banking Panel Chair likes to work by consensus). However, the problem about lack of experience remains," concludes Pedersen.

Forecast

Based on their thesis that length of experience is a determining factor in the strength of the Dollar, Danske has come up with a forecast for EUR/USD, which is for it to rise to a new upside target of 1.25.

"We continue to stress that a 2018 rebound towards 1.25 is on the cards for EUR/USD and crucially stress that upside risks dominate the medium-term outlook with levels around 1.30 justified by valuation," says the Danske analyst.

Part of the basis for the forecast is the expectation that the European Central Bank (ECB) will continue 'normalizing' policy, which means winding down their money printing (Euro-positive) and possibly even raising interest rates eventually (also Euro- positive).