In an interview with the Wall Street Journal US President Trump said that the Dollar is “getting too strong” and that he prefers a “low interest rate policy”.

It appears Trump’s reference to lower interest rates has really caught attention with most analysts reading this to signify intent to appoint to the Federal Reserve board members who would share his view that low interest rates - and by proxy a lower Dollar - are appropriate.

The Trump administration set to appoint two new Fed Governors this year – and potentially a new Chair and Vice-Chair next year.

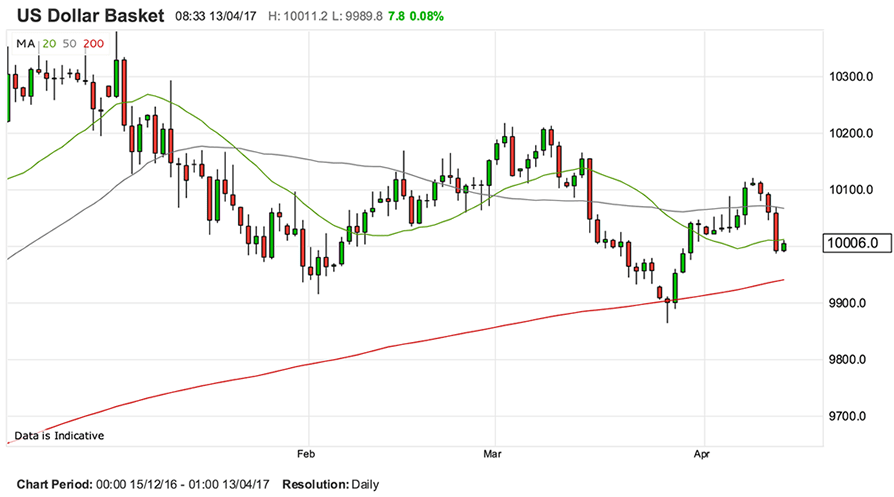

The US Dollar index - which is a measure of broader Dollar performance against a basket of currencies - endured its largest daily drop since mid-March on the comments.

To us it appears that further Dollar weakness is now likely and we would imagine that the Dollar index is intent on falling back towards the 200 day moving average which is denoted by the red line in the graph above.

We saw the index bounce back from this level back in March and would suggest this could be repeated.

However, losses towards the mid-99’s must be endured first.

Reactions

Kit Juckes at Societe Generale says further Dollar strength should be muted from here:

“President Trump doesn't like a strong Dollar, does like low interest rates, may yet offer Janet Yellen a second term, recognises that China isn't a currency manipulator, and is struggling to enact policies that will boost US growth.

“Looked at in that light, perhaps it's only to be expected that the Dollar is drifting lower. The medium-term case for the euro to usurp it as strongest of the major currencies grows steadily even if European political uncertainty holds it back in the short term.

“Looking ahead, it's tempting but probably unwise to write off the Dollar's prospects completely. The Fed isn't done tightening yet, the economy isn't done growing and we don't think we've seen the highs for yields yet.

“At this point, market expectations of a third Fed hike this year has faded significantly, and by too much. For all that though, further Dollar strength is going to be muted because by and large, economic prospects elsewhere are improving too.”

Viraj Patel at ING Bank N.V says some losses in USD should be recovered:

“While we've seen attempts from the President to talk down the Dollar before, the reference to interest rates makes this jawboning with a hypothetically credible action point.

“All assumptions around the interaction between Trump’s pro-growth fiscal plans and the Fed’s reaction function have so far been hinged on inflation being anchored around the 2% target; the baseline view is that the Fed might be forced to tighten quicker if any fiscal stimulus was delivered.

“But it’s clear that this chain of logic is becoming distorted and with the Trump administration set to appoint 2 new Fed Governors this year – and potentially a new Chair and Vice-Chair next year – the standard assumptions cannot be taken for granted.

“A shift in the inflation target remains a tail risk for now (given the negatives here), but it’s not inconceivable to see the Fed allowing for a sustained period of above-target inflation, while hiking rates very gradually. While this points to downward pressure at the front-end of the US rate curve, the reality is that US growth and inflation will remain relatively robust.

“For now, the Dollar’s woes remain compounded by rising geopolitical tensions (North Korea) – although in the absence of any escalation, we would expect the $ to pare some of its post-Trump loses (DXY above 100).”

Bipan Rai at CIBC Capital Markets says the implications for the USD “are huge”:

“For two decades, the US has pursued a ‘Strong Dollar’ economic policy which states that a strong USD is in the interests of the US and the rest of the world.

“Markets have been confused about the current administration’s US Dollar policy for some time now. Today’s comments confirm what we already suspected - that Trump is taking aim at trade deficits.

“A strong USD is incongruent with that goal which means that markets can no longer rely on this administration’s support of the ‘Strong Dollar’ policy.

“Additionally, Trump’s prior statement that health care reform should come before tax reform is important. The implicit takeaway here is that tax reform will be delayed further beyond August and towards the end of the year (if that) – a serious blow to USD bulls in the near-term.”

Marko Valli at UniCredit Bank:

“The policy of a “strong Dollar” and the plan to “bring back US manufacturing jobs” were not really a consistent mix. A stream of remarks these past few months seems to confirm that the US administration is erring towards a softer currency stance to support industry jobs and reduce the current account deficit.

“All this chimes with our fundamental view of Dollar weakness.”

Valentin Marinov at Credit Agricole:

“A weaker USD maybe a wish too far, however, for a President willing to introduce fiscal stimulus before long, which could help US growth and boost inflation. In addition, the Fed remains resolutely independent and will hike in response to improving economic conditions from here.

“Fiscal stimulus, independent Fed and weaker USD seem to constitute what we like to call President Trump's impossible trinity. The construct also makes us fairly constructive on USD for the time being as we expect improving US fundamentals and Fed tightening to boost the demand for the currency once more before long.”

Diane Schumaker-Krieg at Wells Fargo Securities Economics Group says the Dollar should retain a positive tone going forward:

“We have seen that the Trump administration’s position regarding trade seems to have changed or morphed into a more benign view about the changes needed for trade to benefit the U.S. economy.

“We expect the trade-weighted Dollar will continue to appreciate in 2017 as U.S. short-term rates rise. This represents a continued challenge to any attempts to reduce the U.S. trade balance.”