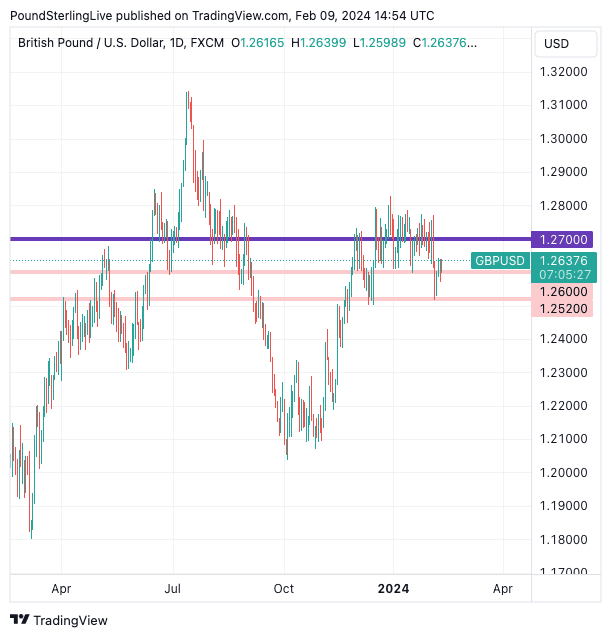

- GBP/USD well supported above 1.2520

- U.S. inflation data due on Tuesday

- UK inflation, wages, GDP and retail sales on tap

Image © Adobe Images

The Pound to Dollar exchange rate remains well supported and the coming week's heavy UK and U.S. economic calendars could offer the chance of a return to the 1.27 level.

The Dollar remains 2024's top-performing currency, but it has lost some impetus of late and has failed to exact any significant damage against Pound Sterling, despite the stellar U.S. economic data prints.

The Pound has withstood the USD's onslaught better than its G10 peers, which speaks of a resilience that is unlikely to fade anytime soon, particularly if this week's data confirms the UK economy picked up steam at the start of the year.

Above: GBP/USD remains well supported. The 1.27 pivot line looks an attractive target in the coming days. Track GBP and USD with your own custom rate alerts. Set Up Here

Data surprises from the U.S. have been resolutely strong over recent weeks, and we will need to see this pattern repeated in the coming days to keep the positive USD momentum going.

We question whether we have reached 'peak surprise' on the U.S. economy and the Dollar; i.e. expectations are already so elevated that the biggest currency reaction will be to any disappointments from data undershoots. It might just be the case that we need increasingly eye-popping releases to keep the USD impetus going.

This is why Tuesday's U.S. CPI inflation release will be so important: if we get a consensus-busting report, then we will look for further upside that pushes the Pound to Dollar exchange rate back down to the medium-term support at 1.2500/20 (tested last week).

This support looks firm, and we imagine U.S. inflation must beat the expected 0.2% month-on-month figure that the markets expect by some margin. (Expectations for year-on-year = 3.0%).

Should the U.S. inflation numbers undershoot expectations, we would look for a solid rebound in Pound-Dollar back towards the 1.27 level that has acted as a magnet to the pair for most of 2024.

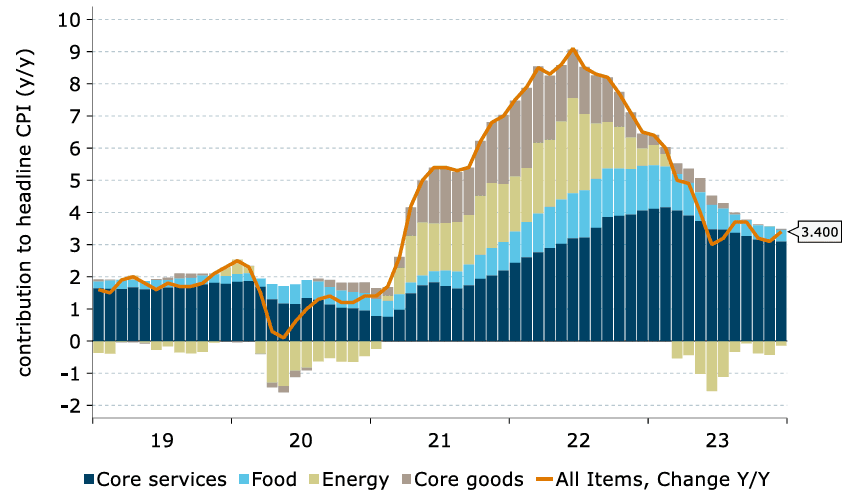

Above: Contributions to U.S. CPI inflation, image courtesy of ANZ.

Also watch U.S. retail sales on Thursday, where a beat on the expected 0.1% m/m growth can signal the U.S. consumer remains unfazed by the Fed's interest rate rises, which can signal upside risks to inflation.

The UK calendar is busy with inflation, wages, GDP, and retail sales being dumped on investors, which have already reduced expectations for the number of interest rate cuts to come from the Bank of England's Monetary Policy Committee (MPC) in 2024.

"GBP has clawed back into a perceived 1.26-1.30 range but remains vulnerable to the market's interpretation of next week’s data and the shifting bias of comments from MPC members," says Tim Riddell, a strategist at Westpac Bank.

Should data beat expectations, expect rate cut bets to reduce further, leading to Pound-Dollar upside.

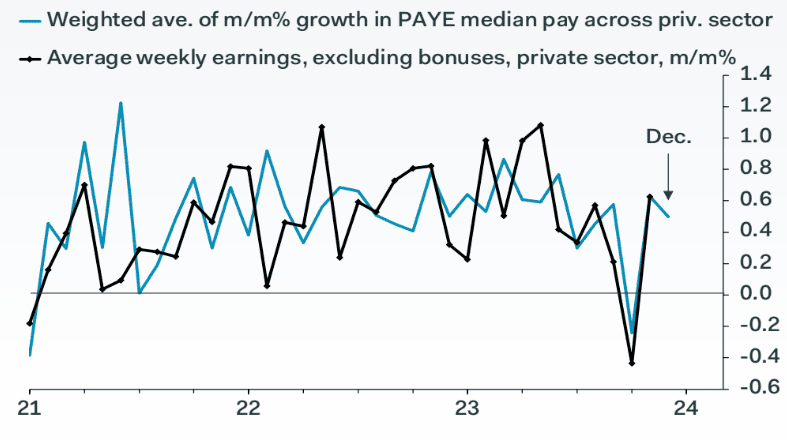

Monthly wage data will be released on Tuesday, where a 5.7% 3M/yr reading is expected for December. Inflation is due Tuesday, and markets expect headline CPI inflation to read at -0.3% m/m and 4.1% y/y in January, with the important core CPI rate at 5.2% y/y.

Above: "PAYE data point to another hefty rise in wages" - Pantheon Macroeconomics.

UK GDP data for December 2023, Q4 and full-year 2023 are due on 15 February at 07:00 GMT; the market looks for -0.1% m/m, -0.1 q/q and 0.2% y/y for the respective releases.

"The UK economy remains on the very cusp of a recession, with our forecast of a 0.2% fall in December GDP enough to deal the final blow and deliver a mild 0.1% contraction in output in the final three months of the year," says Gabriella Willis, UK economist at Santander CIB. "After the fall in GDP already logged in the three months to September, this would be enough to give the UK the unwelcome 'badge' of recession."

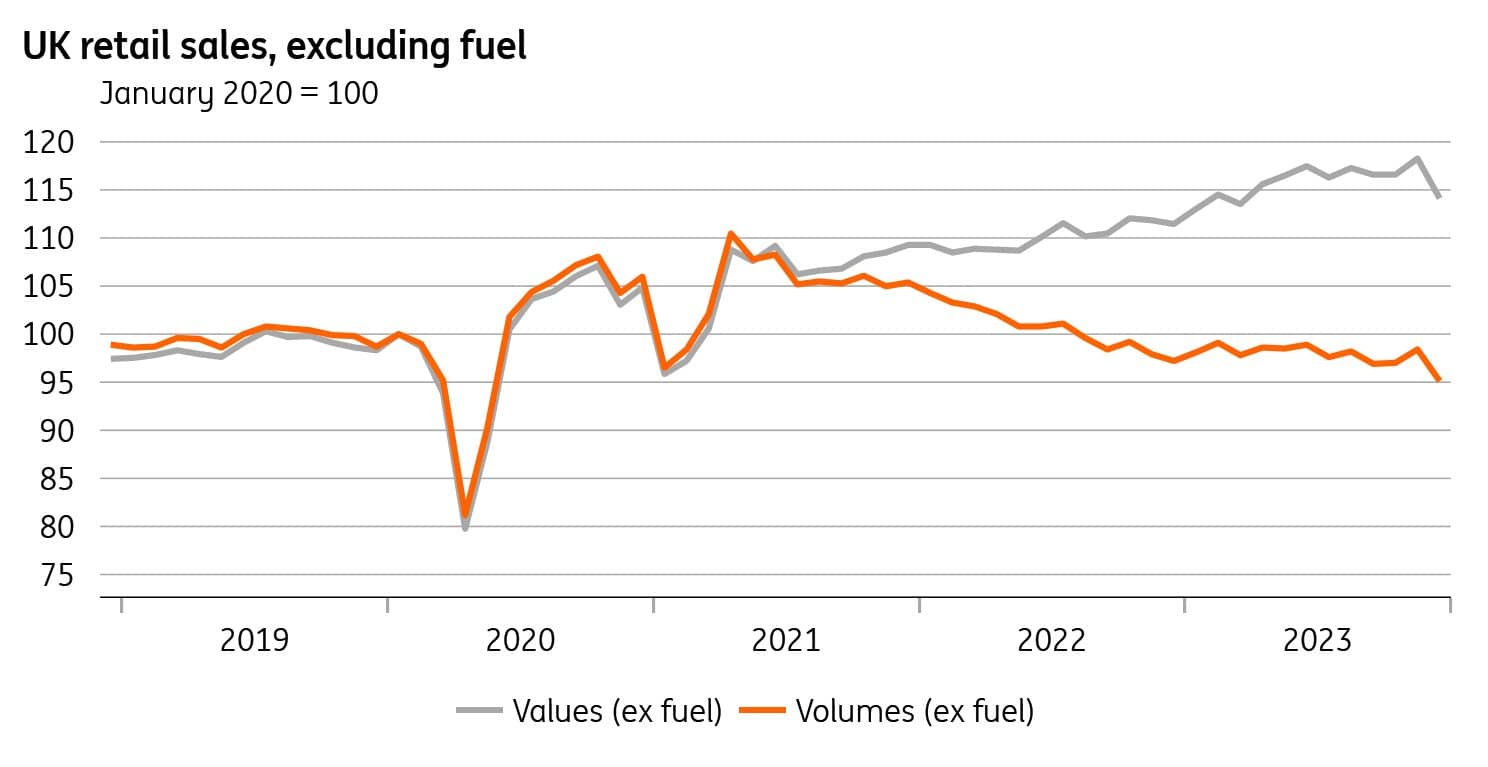

Above: A lot of bad news is already priced into the UK retail sector heading into Friday's release. Image: ING Bank.

Friday brings retail sales data; one only needs to recall that January's release of December retail numbers provided the biggest surprise for the month, sending the Pound lower.

Another weak outturn could result in a dour end to the walk, although we note that survey data has suggested the economy picked up steam January, which suggests the figures could land on the positive side.

With wage growth continuing to outstrip inflation, the outlook for UK consumers has improved markedly, and this will offer pretty conditions for retailers in the months ahead.

Simon French, Chief Economist and Head of Research at Panmure Gordon, says despite the soft retail data, "the UK’s economic outlook has improved markedly over the last twelve months. Benchmarking its economic momentum against other major European economies, the UK has moved up from 8th of 9 last January, to 3rd of 9 currently."