- USD spikes on Israel attacks, boosting USD

- GBPUSD short-term outlook remains positive

- But strength to be limited given broader USD dynamics

- UK GDP data due Thursday

- Watch Bank of England's Pill on Thursday

- And Governor Bailey on Friday

Image © Adobe Images

Surging oil prices at the start of the new week put the U.S. Dollar back on the offensive, but a correction higher in the Pound to Dollar exchange rate can extend over the coming five days

Global markets were in the red at the start of the new week owing to rising geopolitical concerns centred on the Middle East following the weekend terrorist attacks by Hamas on the state of Israel. The arch of concern loops back to Iran - a longtime sponsor of Hamas - which remains a major supplier of oil to global markets.

"The shocking attacks in Israel have sent the price of oil soaring, as investors assess the potential for the conflict to disrupt supply in the Middle East, if other countries are drawn in. With the Israeli government warning of a long and difficult war, there are concerns that deep and incessant retaliative strikes on Gaza could potentially bring Iran into the conflict and have an impact on the flow of energy in the region," says Susannah Streeter, head of money and markets at Hargreaves Lansdown.

Rising crude is inflationary and can weigh on the global growth outlook, boosting the Dollar, considered a safe haven currency.

Making predictions based on geopolitics is notoriously difficult, but if Iran is able to maintain a low profile over the coming days, the Monday spike in the Dollar and oil could prove shortlived. At the time of this article's update, the USD has indeed given back much of its strength, allowing Sterling to extend its recovery.

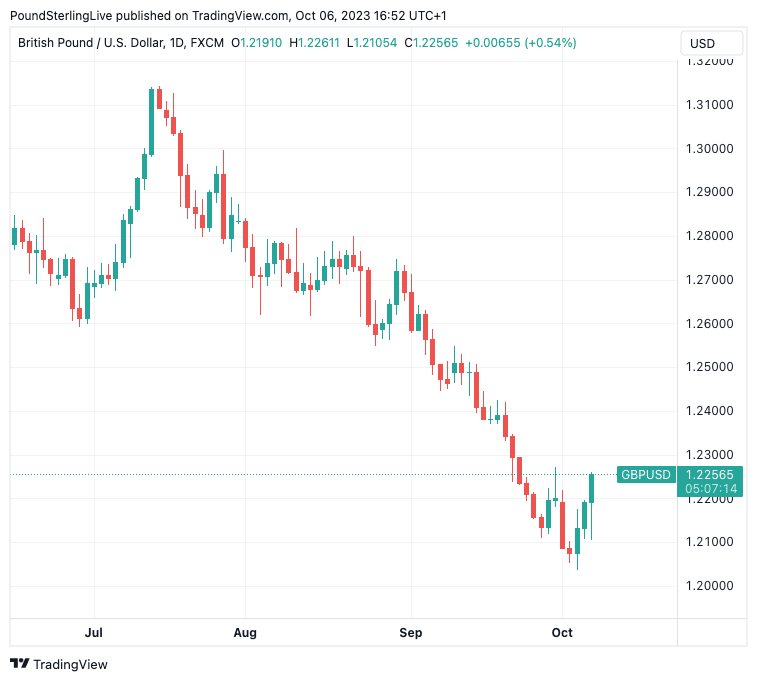

The Pound to Dollar exchange rate's technical picture had improved owing to last week's razor-thin gain that effectively halted an impressive run of losses as predicted by last Monday's edition of Pound Sterling Live's week ahead forecast.

Analysts we follow look for this technical improvement to extend over the coming days and a UK GDP release on Thursday and inflation figures from the U.S. could further boost Pound Sterling's prospects.

Shaun Osborne, Chief FX Strategist at Scotiabank, says short-term readings are bullish for Pound-Dollar as per a solid rebound from a mid-week low "via a big, bullish key reversal/outside range signal".

The exchange rate printed a low of 1.2037 midweek before rallying for three days in succession to hit a high of 1.2219, a move made all the more impressive by the recovery from Friday's knee-jerk selloff that followed an impressive job report out of the U.S.

Above: GBPUSD at daily intervals showing last week's advances. Exchange rate alerts. Set up a daily rate alert email to track your exchange rate OR set an alert for when your ideal exchange rate is triggered ➡ find out more.

The gains through the 1.2175/80 area "add to the GBP’s bullish credentials on the short-term charts and support the case for some additional progress in the near-term towards 1.23," says Osborne.

Short-term support in the event of a downturn in fortunes would be found at 1.2185/95.

It must be stressed that the bullish setup here is strictly short-term in nature and covers a timeframe of hours to a few days. The overall picture remains one of weakness owing to the strength of the U.S. Dollar advance.

The Dollar has rallied amidst a surge in long-dated U.S. yields and weak market sentiment all linked to a view the Federal Reserve will be required to keep interest rates at elevated levels for an extended period.

This trade can switch back on anytime and any bullish case for GBPUSD must be viewed as being a counter-trend profit-taking event that is required to rebalance the market from previously overextended positions.

"While we believe that the bulk of the upward adjustment for US yields and the USD has already taken pace now, it is not clear that a peak is yet in place," says Derek Halpenny, Head of Research for Global Markets at MUFG.

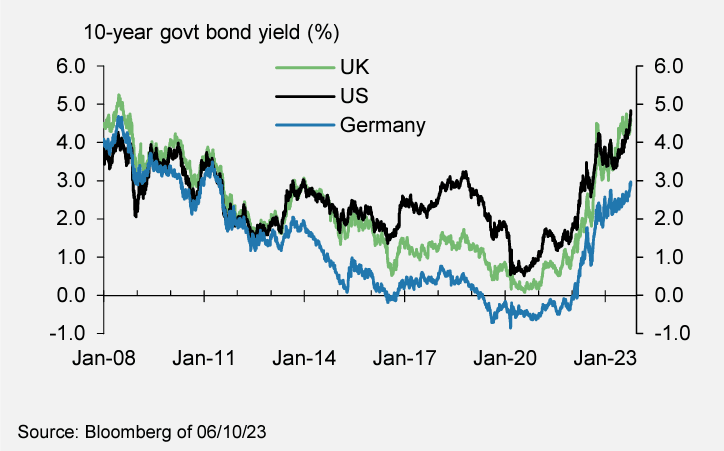

Above: "Government bond yields at multi-year highs" - Lloyds Bank.

The UK economic calendar comes back to life this week with Thursday's monthly GDP release and a number of other economic data prints.

The headline figure to watch is August's monthly GDP where a 0.2% expansion is expected in what amounts to a sharp recovery from July's weather-impacted -0.5% reading.

Should the number beat expectations it would amount to another positive surprise that could boost the Pound. Recall, it is data that is in the driving seat on global currency markets at present and last week we saw Sterling put in some decent gains following the upgrade to September's PMI readings.

There is interest elsewhere at 7AM on Thursday when manufacturing production and industrial production numbers are also released.

However, these tend to be overshadowed by the GDP figure, as does the monthly trade balance release.

Watch out for Bank of England Chief Economist Huw Pill, who is due to speak at 10AM on the same day. Pill's last speech made in Cape Town proved to be of relevance in it set out the Bank's desire to see UK interest rates stay elevated for an extended period.

More of the same could underpin the Pound's prospects against currencies where interest rate cuts are expected to commence earlier in 2024.

Governor Bailey speaks at 9:00 on Friday and could be expected to repeat the line that he expects inflation to fall notably over coming weeks, although the battle has not been won.

Above: File image of BoE Governor Andrew Bailey. Still courtesy of Bloomberg.

Therefore, he will likely parrot the Bank's official stance that it remains ready to hike interest rates again. On balance, this should support market expectations for a potential rate hike before the year is done, which would support Sterling.

Turning to the U.S., Wednesday sees the release of Producer Price Index (PPI) inflation figures that should give a view of how price pressures at the country's factories are evolving. This is an important figure as price changes here tend to lead to developments in the more important Consumer Price Index (CPI) measure of inflation.

The market will want to see a below-consensus figure to confirm U.S. price pressures continue to ease, despite the robust economy.

The market currently expects a reading of 0.4% month-on-month for September, which is down from August's 0.7%.

A beat of expectations would bolster the 'higher for longer' expectation for U.S. interest rate settings, which is ultimately a key source of support for the Dollar at the present time.

Wednesday also sees the release of the minutes to the Fed's September policy meeting, which could further shape expectations around the prospect of a November interest rate hike, although we would be surprised if they had a notable impact on the market.

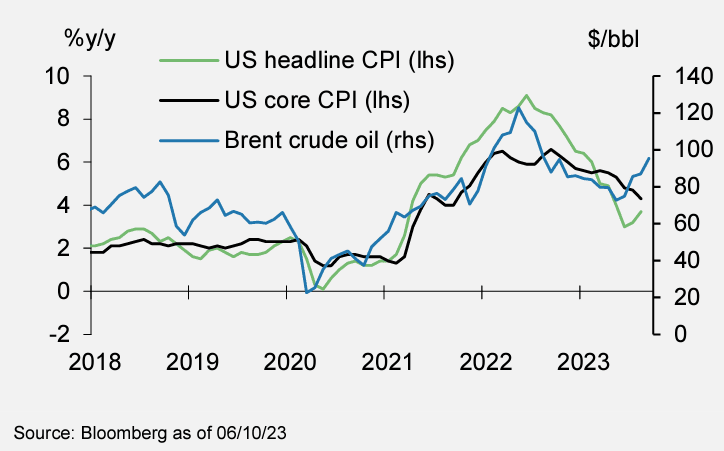

Above: "U.S. headline CPI dragged in both directions" - Lloyds Bank.

Thursday contains the week's highlight in the form of the CPI inflation release for September. The exact same themes relevant to Wednesday's PPI release apply here, except the market impact should be a number of degrees larger.

Headline CPI inflation is expected to have fallen from 0.6% month-on-month in August to 0.3% in September.

Such a development is consistent with the downtrend in U.S. inflation which will mean the Fed is close to ending its rate hiking cycle, give or take an additional 25bp hike in November.

As always, the market-moving impact would come from a surprise to the upside (+USD) or downside (-USD).