Image © Adobe Images

Pound Sterling traded higher against the U.S. Dollar following the release of data that showed U.S. inflationary pressures continued to ease in July, boosting market confidence that the Federal Reserve won't raise interest rates again in September.

U.S. inflation rose 3.2% in the year to August according to an official release, which was below the 3.3% expected by markets, albeit still higher than June's 3.0%. Month-on-month inflation was unchanged, and in line with expectations, at 0.2%.

The all-important core CPI reading stood at 4.7% y/y, less than the 4.8% the market was expecting and down on June's 4.8%. Month-on-month core inflation was also unchanged and met consensus expectations at 0.2%.

"Today's no-surprise U.S. CPI print provides more evidence that the disinflationary forces are firming and monetary policy tightening is working. Core inflation came in at 0.2% m/m for the second straight month, which in annualized terms is broadly consistent with the 2% target," says Ali Jaffery, an economist at CIBC Capital Markets.

The Pound to Dollar exchange rate extended a near-term recovery to go 0.75% up on the day to 1.2810, with the Euro-Dollar seen up by an equal amount at 1.1056.

This left the cross exchange rate that is Pound-Euro unchanged at 1.1587.

"The August number will be out before the Fed next meets in mid-September, but there is nothing in this release to suggest that they will do anything other than keep interest rates exactly where they are. It is increasingly looking like the Fed has done a good job, for now anyway. While we could see inflation track upwards again, markets will be giving them the thumbs up in the short term," says Neil Birrell, Chief Investment Officer at Premier Miton Investors.

The Dollar strengthened through the second part of July and into early August amidst rising U.S. bond yields that are in turn a reaction to a string of stronger-than-expected U.S. economic releases.

Markets have been betting the economy remains in robust shape and would be able to withstand further Fed rate hikes. However, rising yields and Fed hike expectations have weighed on equity markets of late, creating the kind of risk-off conditions that further fuelled a USD comeback.

But the softer inflation data reading suggests the Fed can afford to pause the hiking cycle, thereby boosting equity markets and reversing some of the Dollar's recent outperformance.

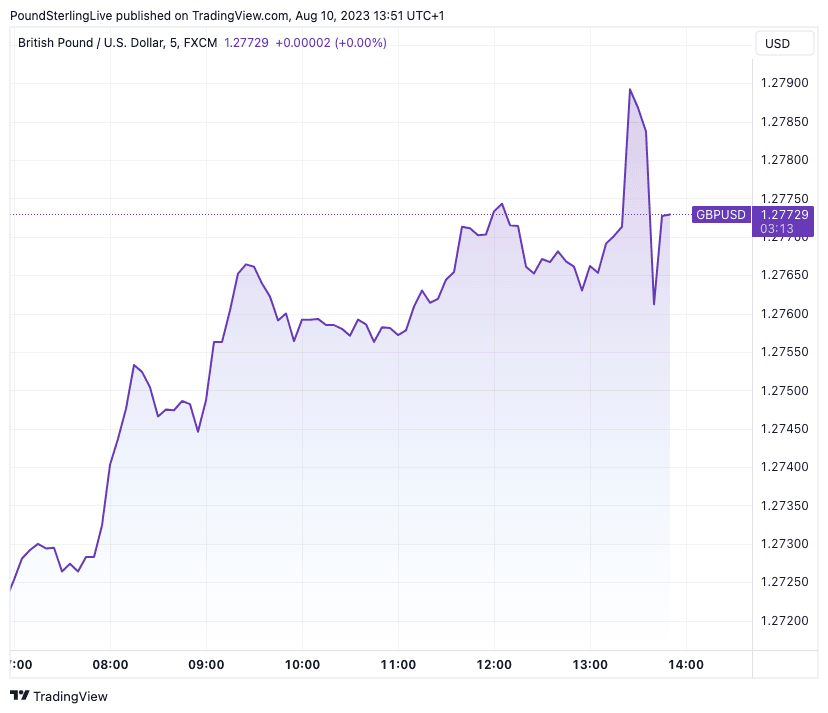

Above: GBPUSD at five-minute intervals.

As the initial knee-jerk reaction to the data release fades we see the Dollar retracing some of its initial losses, confirming that today's surprise was not large enough to fundamentally shift the market.

After all, there is still another inflation release to come ahead of September's FOMC.

"Inflation is grinding back towards target and the labour market is slowly cooling, but the FOMC will want to see yet more data before deciding in September if progress has been fast enough to warrant a pause, or if the balance of risks calls for another hike to ensure inflation targets are met. Market pricing currently favours a pause, but the market has underpriced the Fed’s actions before," says Ryan Brandham, Head of Global Capital Markets for North America at Validus Risk Management.

The low liquidity month of August is typically one that favours the Dollar and a number of analysts we follow suggest further near-term Dollar strength is possible.

"We’ve had the same view on the US dollar for a while now. To re-hash – we see near-term upside," says Bipan Rai, Head of FX Strategy at CIBC Capital Markets.

Expectations for near-term USD upside are based on markets underestimating the two-way risk for incoming U.S. data and how the Fed will react.

Treasury refunding and the amount of bill and coupon supply means that banking system reserves should fall more aggressively going forward as households and corporations absorb most of that supply.

Furthermore, there’s too much tightening priced in for other major central banks (including ECB, BoC) which must loosen.

However, the medium-term picture remains one of USD weakness says CIBC who see rallies in the currency as an opportunity to sell.