Image © Adobe Images

- GBP/USD reference rates at publication:

- Spot: 1.3877

- Bank transfers (indicative guide): 1.3491-1.3588

- Money transfer specialist rates (indicative): 1.3750-1.3808

- More information on securing specialist rates, here

- Set up an exchange rate alert, here

The Dollar's two primary drivers into year-end will remain 1) expectations for policy normalisation at the Federal Reserve, and 2) risk sentiment on global markets.

The latter driver could however throw up some unexpected surprises for unwary investors warns a prominent foreign exchange analyst we follow.

Stephen Gallo, European Head of Foreign Exchange Strategy at BMO Capital Markets finds the U.S. Dollar might be losing its responsiveness to fluctuations in risk-on/risk-off sentiment in global markets.

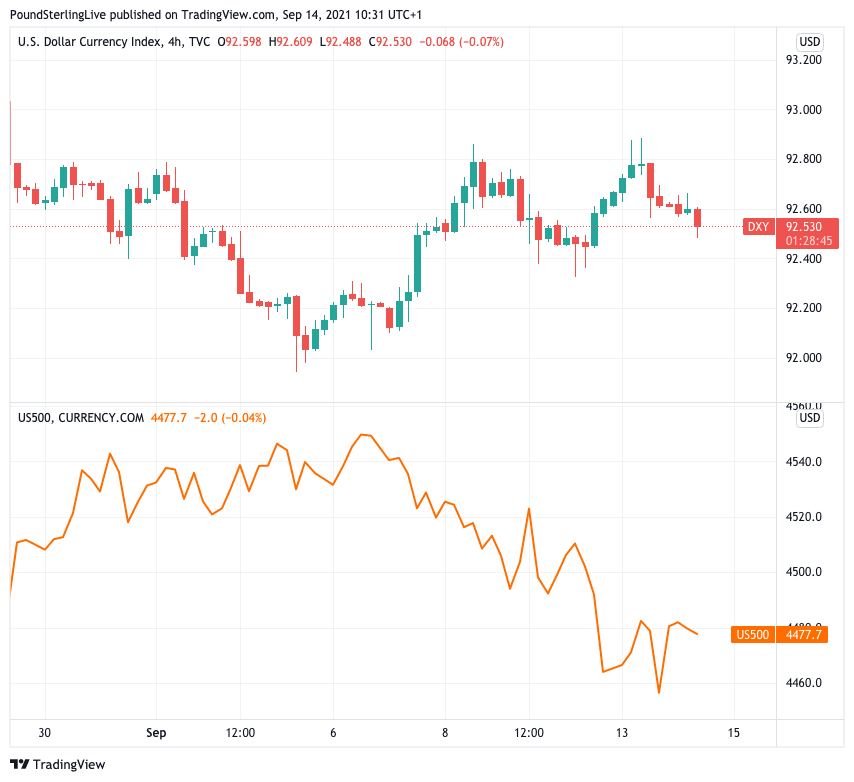

"The S&P 500 fell by 1.6% last week, with the bulk of the damage coming on Thursday and Friday. Given the typical rhythm of RORO (risk-on/risk-off) price action that we have seen for most of the past 15 months, one might have expected a substantial USD rally over that period," says Gallo in a regular daily research briefing.

He finds that Bloomberg's USD index - a broad measure of Dollar performance - did rally by 0.5% last week, but when the equity decline was the most intense on Thursday and Friday, BBDXY fell by 0.1%.

"That price movement doesn't seem to square with RORO at all!" says Gallo.

Above: The USD index (top) and the S&P 500 (below) which is seen as a proxy for global investor sentiment.

The 'Ro-Ro' trade means the Dollar, considered a safe-haven asset, tends to benefit when stock markets are selling off.

Another spin on this dynamic is that when investors liquidate holdings of stocks or commodities the Dollar naturally benefits as the asset is converted to cash.

The Dollar's vast liquidity makes it the default beneficiary when markets are falling, therefore any further market jitters related to the Delta variant could mean that, all else being equal, the Dollar would benefit.

With the U.S. and Asian regions seeing rising Covid cases (China looks particularly prone to stop-start restrictions as Delta flares up) the prospect of Dollar gains driven by souring market sentiment therefore remains a prospect for global FX going forward, unless of course the link is broken.

Gallo finds that one explanation for the Dollar's refusal to rally when markets slipped recently lies with the investment community's existing investment in the currency.

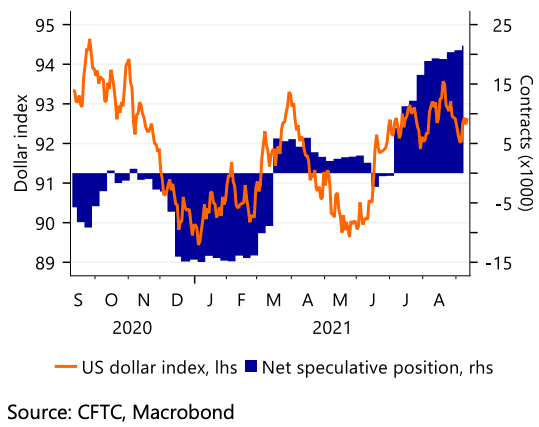

Image courtesy of Rabobank.

The most recent report on how investors are positioned from the CFTC "gives a hint as to why the USD didn't rally as equities cratered," says Gallo.

The CFTC data shows that IMM leveraged funds were holding their largest net long-Dollar position (against the basket of other primary currencies) since June 2020.

As of last Tuesday, leveraged funds' net long-USD position stood at $9.2BN, which Gallo says is only "moderate-sized" relative to Dollar longs seen in 2019 and the first quarter of 2020.

Why then would positioning be an impediment to the Dollar now as opposed to when positioning was significantly more crowded in the past?

"It is important to note that those USD longs were accompanied by much higher carry for being long-USD (in the case of 2019) or a much strong USD trend (in the case of Q1 2020)," says Gallo.

{wbamp-hide start} {wbamp-hide end}{wbamp-show start}{wbamp-show end}

"Over the past 6 months since early March of 2021, we have seen leveraged funds flip from a small-to-moderate net short-USD position to a moderate net long-USD position. In our experience, such a flipping of sides is normally comes hand-in-hand with a substantial spot move," he adds.

The recent positioning flip from 'short' to 'long' Dollar is observed to have occurred when the spot exchange rate was around similar levels as in March.

"Yes, the greenback made an attempt higher in August, but that attempt failed," says Gallo.

BMO's strategy team are not declaring this to be the end of the Dollar's rally, instead suggesting that a new normal might be emerging

"Risk-off conditions in other markets like equities may not lead to a USD rally because the liquidation trade in FX is now to sell out of substantial USD longs," says Gallo.