© RCP, Adobe Stock

- Sluggish global growth to support the U.S. Dollar.

- High hedging costs keep short-sellers at bay.

- Poor long-term fundamentals are a spoiler.

A global economic slowdown and the exorbitantly high cost of hedging against falls in the Dollar are likely to help keep the U.S. currency supported at relatively high levels over the coming months, ING Group says.

Notwithstanding America’s stellar Q1 growth stats, sluggish activity and softer monetary policy prospects in the rest of the world (RoW) are as responsible for the recent rebound in the U.S. Dollar as domestic factors, and the trend will probably continue.

High short-term U.S. interest rates have driven up the cost of hedging investments in the U.S., especially for core investors from Europe and Japan. The result has been more support for the U.S. Dollar as those investors who buy U.S. assets are no longer selling the Dollar at the same time as they invest.

Hedging investments into the U.S. involves selling the Dollar so that if it weakens over the life of the investment then the investor recoups from the hedge what was lost from the value of the U.S. asset they bought.

Yet, it is now just not worth buying a Dollar currency hedge on a U.S. investment since it can cost as much as 3.1%, which is more than the Federal Reserve interest rate today, says Chris Turner, global head of strategy at ING.

Turner says this high hedging cost could really help suport the Dollar if the trend of global economic stagnation continues and inflation in economies outside the U.S. falls then demand for U.S bonds (and the Dollar) could increase.

“If increasing fears of secular stagnation are realised, we would expect to see the investment community (eg, those running balanced funds which invest in both equities and bonds) rotate away from equities and into the bond market," Turner says. "US fixed income would receive sizable inflows as a result of its large weight in global bond benchmarks. Currently, the US has the largest weight (around 30%) in the Bloomberg Barclays Global Sovereign Index.”

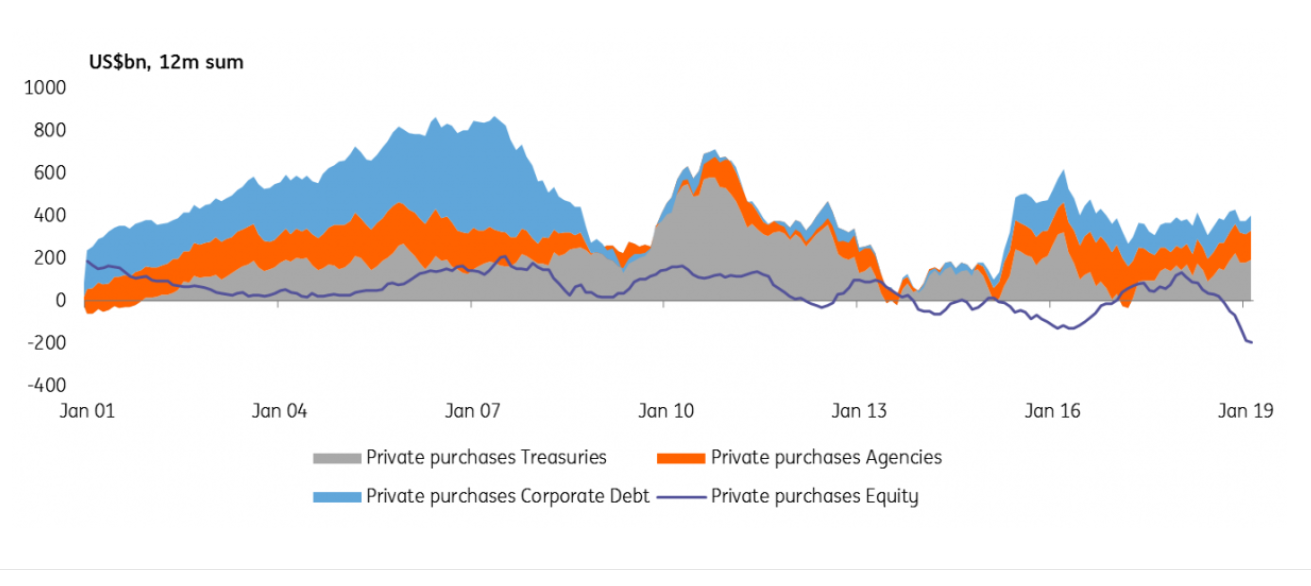

Above: Investment flows into the U.S. Source: ING Group.

Higher unhedged inflows into the U.S. bond market will see demand for the U.S. Dollar surge, increasing its value, because investors must buy the Dollar before they buy the bonds.

“The data (as of February 2019) shows consistent foreign private sector purchases of US bonds (Treasuries, Agencies and Corporates). In contrast, foreigners have sold US equities for the last ten months,” says Turner.

The main risks to ING’s are of a sharp, positive re-assessment of growth overseas, or much weaker US growth which prompts a re-assessment of Fed policy by the market that ultimately leads to expectations of an imminent easing. But this scenario is seen as unlikely, which means the Dollar will probably be staying stronger for longer.

Turner says the pro-Dollar outlook suggested by his analysis will result in an eventual revision of ING’s year-end 2019 EUR/USD and USD/JPY forecasts of 1.18 and 108. But other analysts see the Dollar’s rally as limited by economic fundamentals.

"Our medium-term contention remains that the USD has peaked and should begin a secular downtrend. However, robust US data, continued underwhelming data in Europe, and positive risk sentiment may keep USD modestly supported in the near-term. The increase in corporate issuance in low-yielding currencies, converted back into higheryielding currencies like USD, may continue to provide support to the USD. DXY broke the previous cycle high of 97.70," says Gek Teng Khoo, a strategist at Morgan Stanley.

Time to move your money? Get 3-5% more currency than your bank would offer by using the services of foreign exchange specialists at RationalFX. A specialist broker can deliver you an exchange rate closer to the real market rate, thereby saving you substantial quantities of currency. Find out more here.

* Advertisement