© Robert Cicchetti, Adobe Stock

- USD has topped out, will soon decline says Morgan Stanley.

- U.S. growth to slow as stimulus fades and conditions tighten.

- Rest of world to motor on as Chinese markets, outlook stabilises.

The Dollar is close to topping out and will not reach meaningful new highs, according to analysts at Morgan Stanley, who are telling the bank's clients to begin selling the U.S. currency.

The Dollar is set to resume its 2017 decline early in the New Year, the bank says, as support provided to the economy by President Donald Trump's tax cuts begins to ebb away and growth starts to slow.

This will see the tables turn on the Dollar because the currency tends to do well only when the U.S. is growing at a faster pace than the global economy, or on occasions when the overall global economic outlook turns sour.

During the good times, when all of the world's economies are motoring along at a healthy pace with no signs of any icebergs on the horizon, investors tend to ditch the safe-haven Dollar and go off in pursuit of higher returns elsewhere.

That relationship explains how and why the Dollar converted what was a -4% 2018 loss at the end of the first-quarter, into a near-5% gain during the seven months or so until the beginning of November.

Above: U.S. Dollar index shown at daily intervals.

"Instead of strong inward foreign direct investment or other long-term flows, we see evidence that flows to the US have been into money market funds and are carry trade motivated. We expect these carry trade flows to reverse and flow out of the US as US growth slows," says Hans Redeker, head of currency strategy at Morgan Stanley, in a recent note to clients.

U.S. economic growth picked up to its fastest pace for four years during the second quarter, aided by fiscal support from Washington that almost halved the corporate tax rate and handed an estimated $1,200 in annual earnings back to the average household.

This, combined with rising oil prices, supported an increase in inflation and a perkier outlook for consumer prices pressures over coming years. That gave the Federal Reserve (Fed) the only excuse it needed to press on with its multi-year efforts to "normalise" its monetary policy by lifting interest rates toward more historically normal levels.

Meanwhile, growth in the Eurozone fell from a quarterly pace of 0.7% at the end of 2017, to just 0.4% during the first three months of 2018. The quarterly pace of GDP growth subsequently declined to 0.2% by the end of the third-quarter.

And during that time President Trump's reviled but long-mooted confrontation with China over its "unfair" trade policies has stoked fears for the Chinese and global economies, casting a shadow over the outlook for both.

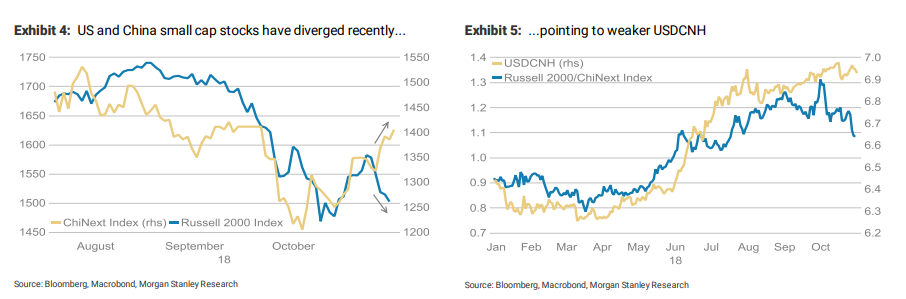

"Small cap companies provide the backbone for both economies and it seems that optimism concerning the performance of US economy has decreased over recent weeks while China’s market now expresses a higher degree confidence, rallying 18% from its October lows," says Redeker.

Above: Performance of U.S.-Chinese stocks and currencies. Source: Morgan Stanley.

After spending the summer months crushed beneath the weight of fears over what President Trump's tariffs might do to the economy, Chinese stock, bond and currency markets rebounded during late October and early November.

Mounting hopes that the so-called trade war between the world's two largest economies will soon be de-escalated were behind the change in fortunes.

Presidents of both countries are set to discuss bilateral trade at the G20 summit scheduled for the end of November. This has led some analysts to suggest a detente could now be in the pipeline, which would be positive for the global outlook.

Meanwhile, over the same period, U.S. stock markets have begun to falter and so too has the bond market. This has been particularly apparent in the small-cap universe.

Small U.S. companies, some of which are highly indebted, have seen yields on their bonds rising faster than those of U.S. Treasuries.

This is lifting funding costs and tightening "financial conditions" for those operating inside the engine room of the U.S. economy and will have an adverse impact on the growth outlook if it goes on for much longer.

"The message seems clear: the narrative is no longer about US-RoW growth de-synchronization, but rather about an improving Chinese outlook, which in turn raises doubts about USDCNH breakinghigher. A USD long positioned market will increasingly find less support," warns Redeker.

The U.S. Dollar index was quoted -0.10% lower at 96.34 Monday but has risen 4.39% for this year. The Pound-to-Dollar rate was -0.01% lower at 1.2827 and has fallen -4.9% in 2018. The Euro-to-Dollar rate was 0.18% higher at 1.1427 but has declined -4.7% since January.

Advertisement

Bank-beating exchange rates. Get up to 5% more foreign exchange by using a specialist provider to get closer to the real market rate and avoid the gaping spreads charged by your bank when providing currency. Learn more here