Image © Nazli Sart, Adobe Stock

- GBP/USD could be starting a new downtrend

- Bearish sign if the pair breaks below 1.2949

- Brexit news to dominate Sterling and 'Thanksgiving effect' the Dollar

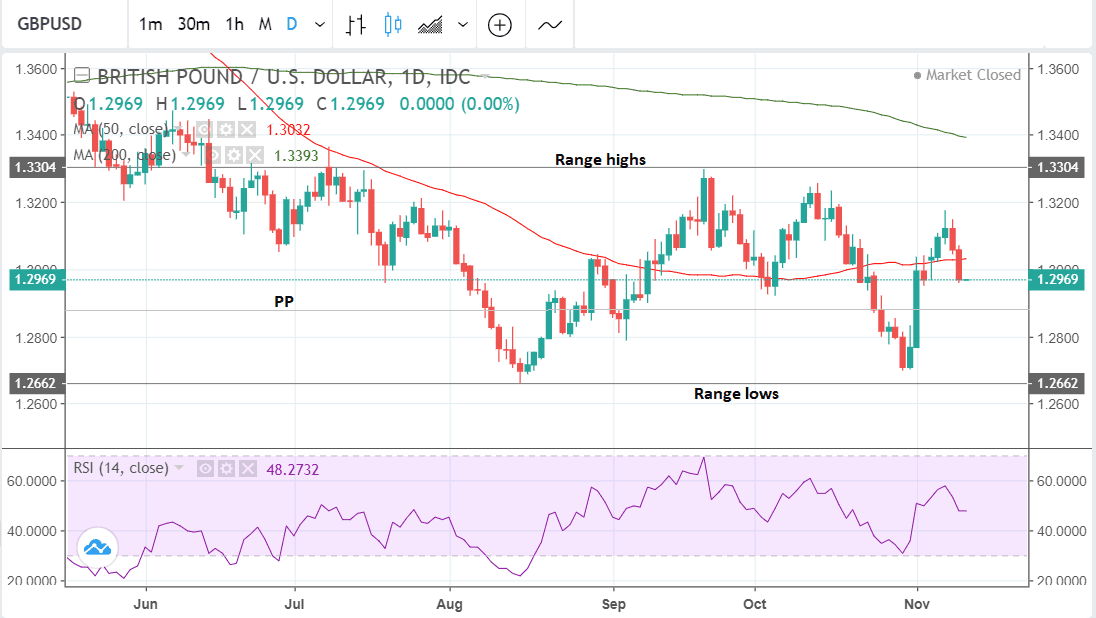

The GBP/USD exchange rate closed out last week at 1.2970, a fall of almost a half a percent from the week before.

The pair is now trading slap-bang in the middle of its short-term range between 1.2660 and 1.3300.

From a technical perspective, there is evidence the recent uptrend enjoyed by the exchange rate may have rotated lower after pulling back down below the 50-day moving average (MA) on a closing basis, which is in itself a bearish sign.

The news out over the weekend that the government's latest attempt at securing a withdrawal deal has been rejected by the E.U. adds a fundamental argument to the view a new short-term downtrend might be commencing.

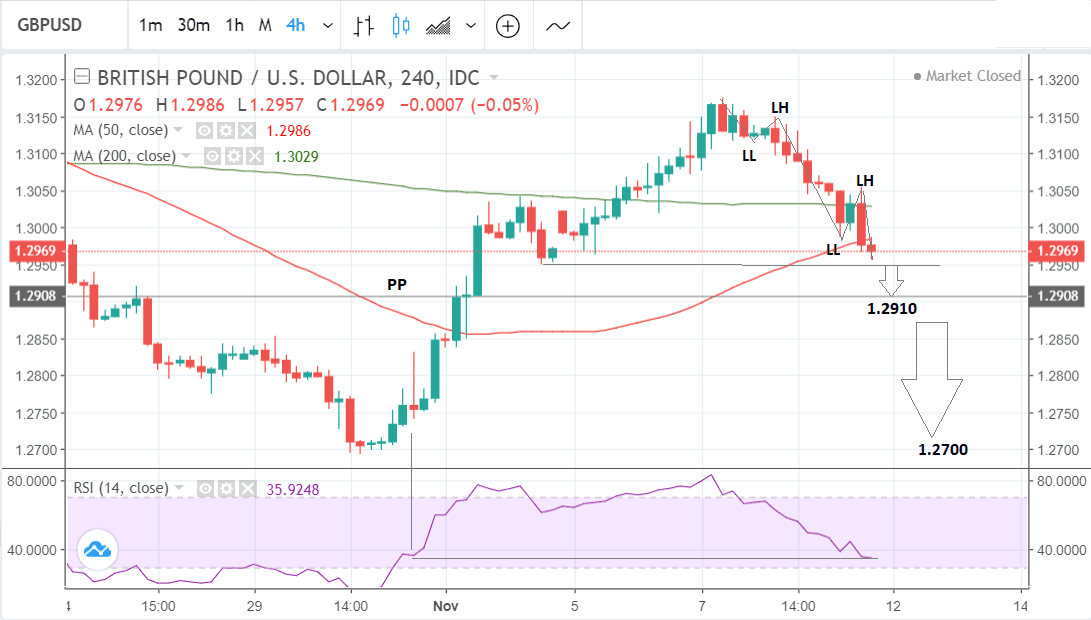

There are signs the pair may have changed trend on the four-hour chart after forming a new down sequence of two lower highs and lower lows - this is often taken by technical analysts as one of the first signs a new downtrend may be forming.

A break below the 1.2949 November 2 low, the last lower high before the November 7 peak, would also add confirmation of a short-term downtrend, with a probable initial target at the 1.2910 lows, where the monthly pivot is situated and should provide a floor for the exchange rate.

A break below that, signalled by a move below 1.2885 would bring the 1.2700 lows into focus as the next downside target.

The extremely low RSI reading suggests strong bearish momentum and further enhances the bearish outlook. RSI is at 35.9, the same level it was at in late October when the exchange rate was only at 1.2750, and this means the pair is more likely to fall purely from the perspective of momentum.

Advertisement

Bank-beating GBP/USD exchange rates: Get up to 5% more foreign exchange by using a specialist provider to get closer to the real market rate and avoid the gaping spreads charged by your bank when providing currency. Learn more here

The Dollar: What to Watch this Week

The most important event in the week ahead for the Dollar is probably actually the US national holiday, Thanksgiving day.

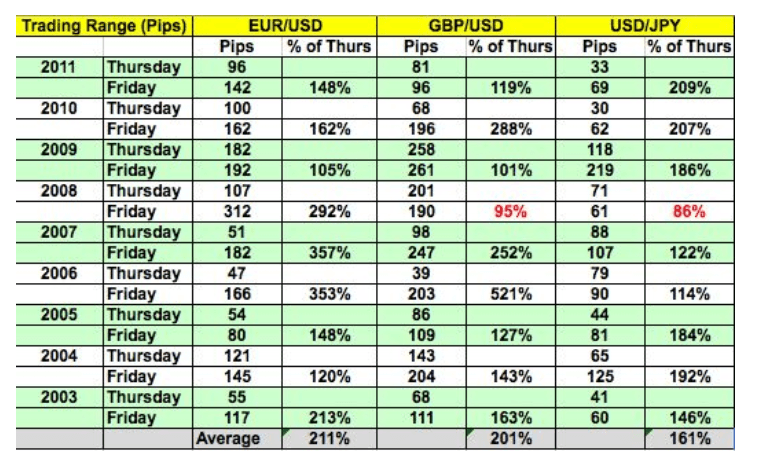

There is a 'Thanksgiving Day effect' in FX markets in which US Dollar pairs tend to narrow their range on Thanksgiving day and then breakout on the Friday after.

The effect is put down to a lack of liquidity due to US traders taking the day off.

The 'Thanksgiving effect' was discovered by Kathy Lien, the managing director of BK Asset Management. The chart below shows how ranges contract in key dollar pairs on Thanksgiving Day and then expand on the Friday after.

Another major release for the U.S. Dollar is CPI data which is forecast to increase by 0.3% on a month-on-month (mom) basis in October from 0.2% in September, when it is released on Wednesday at 13.30 GMT. A beat of expectations could well fuel the ongoing rally in the Dollar.

PPI inflation numbers out on Friday came in well ahead of expectation, suggesting that price pressures in the economy are building.

Core CPI is probably more indicative of domestic price pressures, more relevant to monetary policy and therefore more impactful on the Dollar - it is expected to rise by 0.2% on a monthly basis and keep its year-on-year growth at 2.2%. If so the Dollar will probably remain well-supported as this suggested the Fed continuing with the current policy trajectory.

Analysts at Wells Fargo see a probable 'tariff effect' pushing up prices and lending a positive bias to October's CPI data.

"Looking ahead, we expect price pressures to steadily build, as more businesses feel pressure from tariffs. Tariff effects may be drawn out, since businesses may have some ability to absorb increased costs, but with capacity tight, they may find it easier to pass on higher input costs to consumers. We expect the CPI to climb to 0.3% in October," say Wells Fargo in a foreign exchange briefing to clients.

Another important event for the Dollar is a speech by Chairman of the Fed Jerome Powell on Wednesday at 23.00, and his speech on Thursday at 16.30. Powell will probably simply reiterated the relatively hawkish guidance provided at last week's FOMC given the short duration since the meeting, but if he changes stance or ups his rhetoric, it could impact on the Dollar.

The general consensus appears to be tilted towards expecting more hawkish commentary rather than dovish, which would strengthen the Dollar.

Retail Sales is expected to show a 0.6% rise in October compared to the previous month when it only rose by 0.1%. if this acceleration in buying materialises it may provide an updraught for the Dollar, although given the releases on Thanksgiving Day when USD pairs usually remain with tight ranges any reaction to data could be delayed until Friday when USD is prone to volatility. Since most economic growth in the US is driven by the consumer a rise in retail sales is usually a sign of strong growth and therefore supportive of the currency.

Other key data out on Thursday includes the NY Empire State as well as the Philadelphia Fed Manufacturing Indices in November. Both are expected to show marginal declines.

Industrial production is scheduled for release on Friday at 14.15 when it is expected to show a slightly slower 0.2% rise in October over the 0.3% increase noted in September.

The Pound: What to Watch

The main driver of the Pound in the week ahead is likely to be Brexit news and the British Pound could be in for a soft start to the new week thanks to headlines suggesting the E.U. are to reject proposals put forward by U.K. Prime Minister to break the deadlock in Brexit negotiations centred over the Irish backstop.

"Theresa May’s Brexit deal crashes as E.U. ‘turns off life support’" reports the Sunday Times; a headline that will surely see markets pare exposure to the U.K. currency in the near-term

"This weekend senior EU officials sent shockwaves through No 10 by rejecting May’s plan, sparking fears that negotiations have broken down days before “no-deal” preparations costing billions need to be implemented," says Caroline Wheeler, Deputy Political Editor at the Sunday Times.

The headlines from the Sunday Times are indeed worrying: if true then it might be the case that Theresa May will have to walk away from negotiations as she simply won't be able to muster parliamentary support for a wildly unpopular deal that risks the U.K. being subjugated to E.U. law indefinitely.

Yet, we always knew these negotiations would go down to the wire and with December being the final deadline we are not surprised by these negative headlines.

Markets could be accused of becoming far too optimistic on the state of Brexit negotiations of late. The E.U. always negotiates until the very end; and we are seeing just this.

That is also possible gains on any deal may be short-lived as even if the government announces a deal it will still have to get approval from Parliament, and this could be an arduous process, presenting a risk to Sterling.

The conservative government only has a small majority and is reliant on support from the DUP and every single one of it MPs, so there is a risk that if either the DUP or Brexit rebels vote against the deal Theresa May may find she does not have the majority to push it through, and this could weigh on the Pound.

On the hard data front, one of the most significant releases in the week ahead is likely to be inflation data for October, which, according to the market consensus, is forecast to show a 0.2% rise on a month-on-month (mom) basis and 2.5% rise on a year-on-year (yoy) basis (for headline inflation) when it is released on Wednesday at 9.30 GMT.

A result in line with expectations would probably be bullish for Sterling as higher inflation puts pressure on the central bank to raise interest rates which appreciates the currency.

This is because higher interest rates tend to attract more inflows of foreign capital drawn by the promise of higher returns.

There is a chance, however, that inflation will disappoint because of the waning influence of the cheap Pound which has appreciated on Brexit hopes. Headline CPI has already fallen from a peak of 3.0% in January due to the bounce in the Pound, so more losses are possible - although if comments from the Bank of England (BOE) are anything to go by unlikely.

"In its most recent meeting, the Bank of England (BoE) noted that it does not expect inflation to fall much further, with price growth instead holding fairly steady near the 2% target," say Wells Fargo in a note to clients.

Another major release for the Pound is labour market data out on Tuesday at 9.30. Probably of most significance to Sterling is the average earnings component because of its influence on inflation. The current expectation is for a rise of 3.0% in Earnings (including bonuses) and for a rise of 3.1% in earnings excluding bonuses. A result in line with expectations could be positive for the Pound as it will reflect an even stronger rise in real earnings since the fall in inflation from its January peak.

Other results of note within the labour report are unemployment, which is forecast to remain at 3.0% and employment change which is forecast to rise by 34k.

The final major release for the Pound is retail sales on Thursday, which is forecast to show a 0.2% rebound in October, from a rather weak -0.8% previously, and a 2.8% rise yoy from 3.0% previously, when it released at 9.30 GMT.

Advertisement

Bank-beating GBP/USD exchange rates: Get up to 5% more foreign exchange by using a specialist provider to get closer to the real market rate and avoid the gaping spreads charged by your bank when providing currency. Learn more here