Image © Adobe Images

The Swedish Krona has fallen to within striking distance of its coronavirus crisis lows so far in the year and could be at risk of further losses in the week ahead unless the Riksbank is able to convince a hawkish market of its plan for containing rising rates of inflation in Sweden’s economy.

Sweden’s Krona fell more than 10% against a stronger Dollar and by almost four percent against a depreciated Euro in the first half of the year and its losses very likely reflect more than just the evaporation of investor risk appetite that has crushed many stock markets during the second quarter.

Recent trends in other currencies including the disparity between performances of the Japanese Yen and Swiss Franc, which are both typically viewed by traders as ‘safe-havens,’ suggests that inflation and central bank policy have been significant drivers of the market and declines in Swedish Krona.

“Inflation readings continue to exceed the central bank’s forecasts. The rise in underlying inflation is broad and significant. We believe that the Riksbank will therefore find it necessary to front-load its rate hikes to mitigate the risk of secondary effects,” says Pernilla Johansson, an economist at Swedbank.

All of this puts the Riksbank in the hot seat ahead next Thursday’s policy decision for which market-based measures of investor expectations are suggesting that a 0.50% increase is all but certain to take the policy interest rate up to 0.75% while also implying some probability of a larger move than that.

Above: GBP/SEK shown at monthly intervals and alongside USD/SEK.

Above: GBP/SEK shown at monthly intervals and alongside USD/SEK.

“The rate path will probably be adjusted upward to just over 2% by 2025 and about 1.35% at the end of the year. Asset purchases will be further reduced in the fourth quarter,” Johansson wrote in a Thursday research briefing.

Market expectations are a potential pitfall for the Krona as they mean the Riksbank may now have to go further than it might want to in order to convince of its plan to contain inflation following this year’s significant increases.

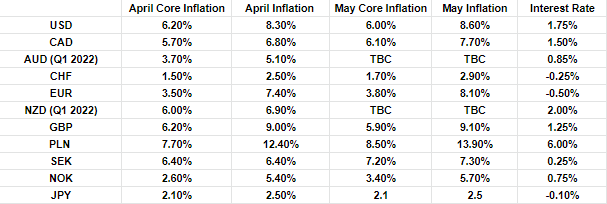

With energy and food excluded from the goods basket under the microscope, Sweden’s underlying inflation rate was among the highest of the G10 currency economies in April and May, while the Riksbank’s 0.25% interest rate was among the lowest and near the most negative in ‘real terms.’

Above: Inflation rates featured according to descending order of 2022 currency performance relative to the U.S. Dollar.

Above: Inflation rates featured according to descending order of 2022 currency performance relative to the U.S. Dollar.

“Almost 80% of the fixed income market's investors expect a 50bps policy rate hike in June and nearly 60% expect another 50bps hike in September,” says Lara Mohtadi, an analyst at SEB, in reference to results of an SEB survey.

“As for the krona, just under half of those surveyed believe that further weakness will not affect monetary policy, the others see 11.00 in EUR / SEK as a "limit" which, if passed, will mean that the Riksbank needs to act in a more hawkish direction to limit the effects of rising imported inflation,” she added.

The Riksbank already surprised economists by lifting its interest rate to 0.25% back in April and announcing that it would rise further to 1.75% by 2025 but since then Swedish inflation figures have trumped all expectations and prompted markets to anticipate a series of sizable rate steps up ahead.

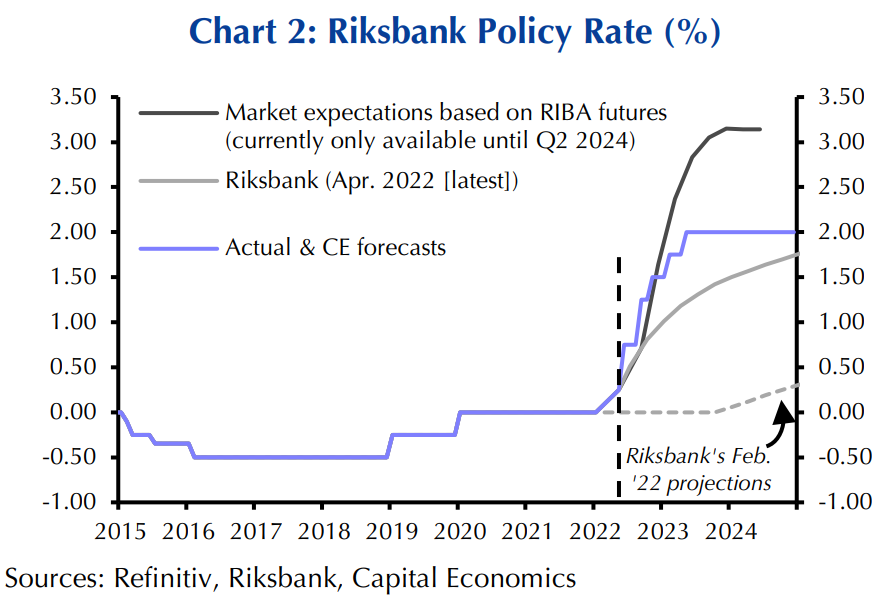

Source: Capital Economics.

Source: Capital Economics.

Expectations implied by overnight index swaps - a form of derivative that can be used for hedging against, or speculating upon changes in interest rates - suggest that investors and traders see Sweden’s interest rate as likely to rise more than tenfold in the months ahead to leave it at 2.37% by year-end.

This sets a very high bar for the Riksbank to surprise in a way that would be favourable for the Krona next week, although not an insurmountable one.

“W expect policymakers to revise them up further next week, notably in the near-term profile. We forecast another 50bp hike on 20th September, and it would not be a huge surprise if the Bank made an unscheduled increase before then,” says David Oxley, a senior Europe economist at Capital Economics.

“That said, with households in Sweden more sensitive to rate hikes than in many countries, and rate hikes likely to be working in tandem with “QT”, the ‘terminal’ rate in Sweden is likely to be below that in most advanced economies. So while the risks to our forecast of the policy rate peaking at 2% next year are on the upside, we suspect that investors have got ahead of themselves,” Oxley adds.