Pound Sterling is likely to get stronger in 2018 say strategists at BMO Capital Markets as they update clients on their exchange rate viewpoints for coming months.

The British Pound is tipped to rise in 2018 for four reasons argues a new analysis from BMO Capital Markets - the global investment bank - citing easing Brexit concerns, undervaluation, a strong UK economy and increased chances of higher interest rates as being behind the view.

The call comes as Sterling edges lower against the Euro, Dollar and other major currencies at the start of February following January's strong performance. Indeed, the Pound was the best-performing major currency in January, a performance that lead a number of institutional analysts to raise forecasts.

The majority of analysts cite an easing of uncertainty pertaining to Brexit as being a key supporting factor to the currency's improved outlook, "a ‘soft Brexit’ looks more likely because of the constraints on UK PM May," says BMO Capital's head of European FX Strategy Stephen Gallo in a briefing to clients.

Given May's small majority and a significant remain fraternity within the party, it is believed May does not have the "political capital" do drive through a 'hard-Brexit', and such a deal would be incompatible with a solution for Ireland.

Her own hardline MPs will probably not undermine a softer Brexit because of the risk such a stance would topple the government, leading to a snap election which the party might lose.

Positive developments regarding Brexit will likely allow the Pound to rise from undervalued levels and drift back up to 'fair value' which can be found around levels seen before the referendum.

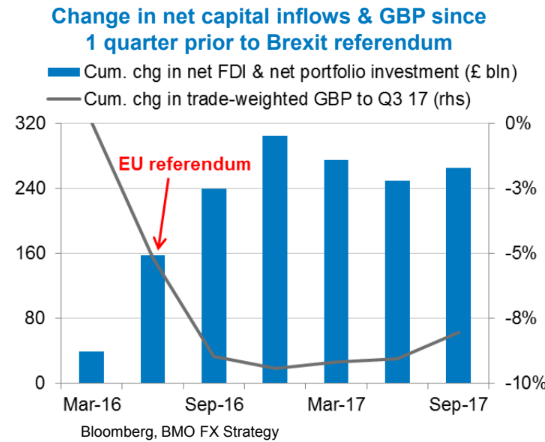

That the Pound is overvalued is suggested by the fact that demand for UK assets from foreign buyers rose significantly after the Pound devalued following the referendum, suggesting the currency was probably fairly valued beforehand suggests Gallo.

The increase in demand for UK assets as measured by FDI and Portfolio flows is shown in the chart below:

Further support for Sterling will be found from economic fundamentals with Gallo believing the UK economy is partaking in the global upswing as evidenced by rising rates of manufacturing.

Economic growth data released at the end of January confirms the UK economy grew 0.5% in the final quarter of 2017 - above consensus expectations. Survey data released at the start of the month confirms that while some of that momentum has been lost, the economy continues to grow at a steady pace which should further diminish unemployment and raise wages.

Expectations for higher wages are in turn fuelling expectations for robust inflation rates which are in turn fuelling expectations for higher interest rates at the Bank of England (BOE).

The higher interest rates will drive up Sterling as they attract higher capital inflows, drawn by the promise of higher returns, which are the modern driving forces of FX markets.

There is one further issue related to Sterling and that is the thorny problem of the current account (CA) deficit.

The CA deficit describes the shortfall in net outgoings and incomings for a country, and - like all shortfalls in income whether it be country, business or person- it must be financed either by borrowing more (from abroad) or by selling UK assets.

One of the key drivers of this imbalance is that the UK imports more than it exports, therefore to balance its books it needs additional inflows to keep the Pound propped up.

Problems financing the deficit can therefore be injurious to Sterling, yet Gallo's view is the deficit is not really a problem for the Pound because the UK is doing well at selling its assets as evidenced by the chart above showing rising demand for FDI and Portfolio flows - two metrics which measure UK asset sales.

BMO Capital forecast the Pound-to-Dollar exchange rate to rise to 1.45 in three months, 1.48 in six months, 1.51 in nine months and 1.53 in twelve months.

Based on BMO Capital's EUR/USD forecasts, we are able to work out the Pound-to-Euro exchange rate path as: 1/15 in three months, 1.1650 in six months, 1.18 in nine months and 1.1860 in twelve months.

Advertisement

Get up to 5% more foreign exchange by using a specialist provider to get closer to the real market rate and avoid the gaping spreads charged by your bank when providing currency. Learn more here.

British Holding of Overseas Assets Provides a Key Support for Sterling

BMO Capital's view on the current account deficit differs markedly from that of JP Morgan, who argue the UK will struggle to finance its current account deficit - although they too are bullish the Pound overall.

JP Morgan do not see the small increases in interest rates currently expected either by markets or themselves as attracting large enough inflows of foreign capital to cover the CA financing shortfall.

"We are not convinced that a modest increase in UK rates over and above what is now priced (we expect 50bp this year, the market prices 35bp) will be a game-changer for the ability of the UK to finance what remains by G10 standards an extremely weak external position," says JP Morgan strategist Paul Meggyessi.

Unfortunately higher interest rates are probably not a very useful tool when it comes to the CA deficit for although they encourage people to save rather than spend their money on foreign imports, they also drive up Sterling which tends to worsen the trade deficit as it makes UK exports less competitive and imports cheaper.

Interestingly, in relation to the UK current account deficit, one of the main reasons has widened so much is not that imports have increased faster than exports but that the amount of income the UK gets from assets owned overseas has fallen dramatically since the financial crisis.

This used to be an important balancing factor in the UK current account sums as it brought a net surplus to the Uk because the UK is such a massive owner of assets abroad.

The situation may change, however, as global growth picks up, the assets the UK holds abroad may increase in value and could start to provide the UK with a surplus which will help offset the deficit in the current account.

This will further bolster Sterling by increasing demand for it from repatriation flows.

"Britain's current account is not just determined by the familiar trade deficit, but also by the balance of overseas income and returns to foreign investors. From 2001 to 2007 this improved our position: Britons reaped more in interest and dividends from elsewhere than they paid out. This helped offset the country's excess of imports over exports, and held down the current-account deficit," says Tutor2U economics tutor Tom White.

The UK still has a large ownership of foreign assets - one of the largest of any nation according to some measures, so this represents a major potential benefit for Sterling.

"By the collapse of 2008, Britons had amassed overseas assets worth about 750% of GDP. Today, following a post-crisis retrenchment, overseas investments amount to just over 560% of GDP. But the country still leads the G20 in overseas investments, by one estimate," adds White.

Get up to 5% more foreign exchange by using a specialist provider to get closer to the real market rate and avoid the gaping spreads charged by your bank when providing currency. Learn more here.