"There's a risk that incoming data might surprise to the upside, potentially pushing yields higher once again" - SEB.

Image © Adobe Images

The Pound was steadier on its feet near earlier lows against the Dollar and Euro in the penultimate session of the week as financial markets contemplated what central bankers could say at an imminent Federal Reserve (Fed) conference but the economic outlook could also be limiting enthusiasm for Sterling.

Sterling was trading back near the round numbers of 1.27 and 1.17 against the Dollar and Euro on Thursday, close to the prior session’s lows, after industry surveys warned of deteriorating business conditions in some key sectors with other factors also helping to lift the greenback and single currency later in the session.

Dollars were bought widely overnight and in early trade on Thursday, placing something of a lid on Sterling, after strong corporate earnings figures lifted U.S. stocks while appearing to provide a tailwind to markets in Europe on Thursday.

“Nvidia's stock experienced a notable rise in US aftermarket trading. The company's performance is pivotal as it serves as a barometer for the entire industry,” says Ole Hvalbye, a strategist at SEB Group in Sweden.

“The retreat in flash PMIs in the US, Europe, and the UK has impacted bond yields, leading the market to hope that major central banks might halt further policy tightening. For now, the US 10-year yield has fallen below 4.20%,” he adds.

Above: Pound to Dollar rate shown at daily intervals with Pound to Euro rate and selected moving averages.

S&P Global survey results suggested a downturn in the UK manufacturing sector deepened in August and that activity in the all-important services industry moderated enough to leave it close to a recession with possible implications for interest rates at the Bank of England (BoE).

“In recent months, actual activity data has diverged from survey data, particularly in the US. There's a risk that incoming data might surprise to the upside, potentially pushing yields higher once again. Currently, the market is operating under the impression that the economy is decelerating,” Hvalbye warns.

UK economic growth was close to zero in the opening half of this year but still remained positive while recent high single-digit pay increases in parts of the labour market and the prospect of household energy bills falling further relative to last year are potentially supportive of the economic outlook.

But the interest rate decisions hinge much more on the prospects for inflation and there are many factors that could yet impede its coveted return to the 2% target including wholesale energy prices, the cost of imported goods and developments relating to both demand and prices on the domestic side of the economy.

“The Bank of England has warned that half of all businesses that have borrowed will struggle to pay their debts by the end of the year, up from 45% last year and this is set to lead to more corporate wariness when it comes to pay rises and taking on new staff,” says Susanah Streeter, head of money and markets at Hargreaves Lansdown.

Prices in financial markets have implied for months that the Bank of England could be likely to continue raising interest rates until early next year with the envisaged peak for interest rates topping 6% at times, though market based measures of expectations have fallen since Wednesday’s surveys were released.

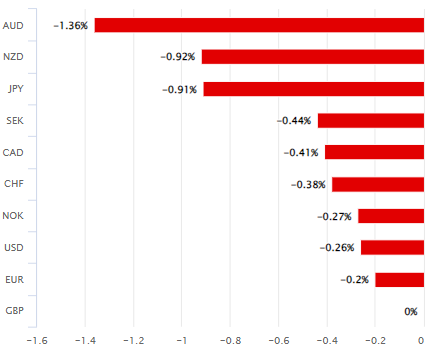

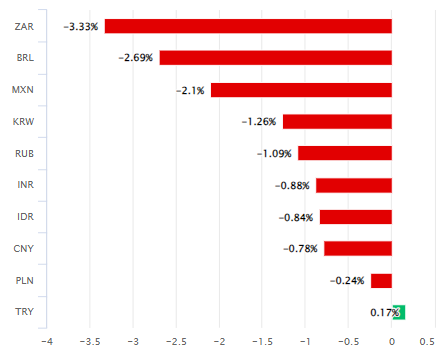

Above: Pound Sterling performance relative to G10 and G20 currencies this year. Click image for closer inspection.

Meanwhile, equivalent surveys of U.S. business activity were more resilient than those released in Europe this week, which is another potential reason for why the Dollar has remained so buoyant on Wednesday and Thursday, while previously the continental current account surplus was reported to have surged in June.

“We have argued since late last year that the reversal in 2022’s negative terms of trade shock would likely show up in a solid improvement in the EUR’s external accounts and help drive a rally in the EUR,” says Dominic Bunning, European head of FX research at HSBC.

“We still see EUR-USD trading towards 1.15 this year – although how close we get to that target will depend upon global risk appetite and US yield dynamics. Meanwhile, we believe further ECB tightening is currently underpriced relative to the Bank of England and have an open buy EUR-GBP trade idea,” he adds.

Thursday’s softer performance from Sterling comes at the opening of a three day get-together of central bankers in Jackson Hole, Wyoming, organised by the Federal Reserve where financial markets will be listening to hear whether any further increases in the Federal Funds rate can be expected in the months ahead.

“Markets are awaiting the Jackson Hole Symposium with anticipation, where Fed Chair Powell will deliver the closing remarks on Saturday (NZT). We expect that Chair Powell will err on the side of caution with respect to inflation, noting some signs of improvement but still with a long way to go,” says David Croy, a strategist at ANZ.

Above: Pound to Dollar rate shown at weekly intervals with Pound to Euro rate and selected moving averages.