A better year-end awaits the British Pound after inflation-busting measures are announced.

Above: London, United Kingdom. Prime Minister Liz Truss leaves 10 Downing Street for House of Commons. Picture by Simon Dawson / No 10 Downing Street.

Prime Minister Liz Truss' energy bill cap slashes future inflation projections and potentially means the UK economy avoids recession, developments that bolster Pound Sterling's outlook.

Truss announced a £2500 price cap on energy bills, that will stay in place for two years, and effectively cancel's October's planned energy cap rise to £3549.

This means energy's contribution to inflation is effectively stalled.

The Pound was volatile on the announcement, rising but then falling as markets digested competing signals from the UK, U.S. Federal Reserve and European Central Bank.

A rate hike at the ECB and promises of more rate hikes at the Fed combined to offer the Euro and Dollar support, just as markets considered the fiscal policy announcements out of the UK.

This creates a near-term churn in currency markets: the Pound to Euro exchange rate fell to a new multi-week low of 1.1478 before recovering to 1.1522, the Pound to Dollar exchange rate fell to a low of 1.1460 before recovering to 1.1474.

Near-term the situation is febrile, but from a purely UK-centric perspective, the economic outlook has changed for the better improved.

This can only be supportive of Sterling over coming weeks.

"We estimate that the direct impact of the measure will lower 2023 inflation to 5.5% from 9%," says Fabrice Montagné, an economist at Barclays.

"We'd now expect a peak of 11% in the autumn versus our previous forecast of 16% in January," says James Smith, an economist at ING.

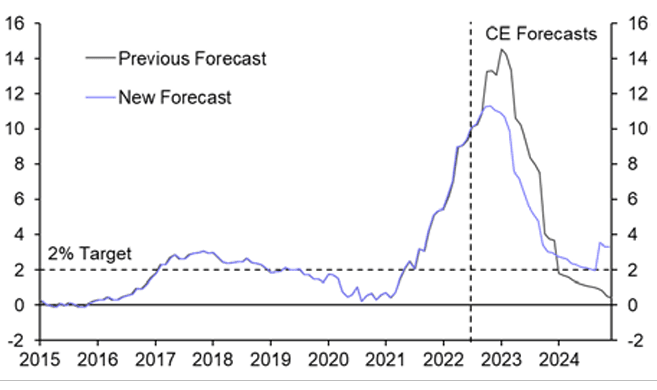

Barclays says UK inflation has now peaked - at 10.1% in July - and should finish this year slightly below 9%, before dropping more quickly in the course of 2023 as negative base effects from energy feed through.

"Rather than rise from the 40-year high of 10.1% in July to about 14.5% in January, inflation may now peak at something like 11.5% in November and then fall faster next year," says Paul Dales, Chief UK Economist at Capital Economics.

While Dales says he still sees a UK recession, he cuts in half the forecasted depth of the peak-to-trough decline in economic activity to 0.5%.

But Samuel Tombs, Chief UK Economist at Pantheon Macroeconomics, says the developments mean the UK economy should avoid recession.

Tombs has consistently proven to be the most accurate forecaster for the UK economy in recent years according to Reuters and Bloomberg polls.

Above image courtesy of Capital Economics.

Expectations for super-charged inflation and recession have created a potent mix for Pound Sterling downside in 2022; when this narrative is challenged, in the way Truss has done, the outlook therefore improves.

Yet energy price rises are still coming, after all, the cap at £2500 still represents an increase from the current cap of £1,971, although a previously announced £400 support package will ease the pain of some the advance.

It is also worth considering that some kind of rise in energy prices is needed to impact consumer demand over the winter: lower demand will be required to ensure the UK doesn't burn through gas which is clearly in limited supply at present.

The government also announced measures to boost exploration and production of natural gas in the UK as it lifts a ban on shale gas production and announces a generous round of licensing for North Sea drilling.

For the Pound's outlook, much now depends on the Bank of England's response.

"The energy price freeze is a material relief for the BoE in fighting inflation. Lower energy inflation will not only have a direct impact but will also lower core inflation through indirect channels," says Montagné.

This would suggest the Bank will potentially deliver less by way of interest rates than currently expected. Barclays think latest development support their forecast of a 50bp hike in September, a 25bp in November and status quo at 2.5% thereafter.

This is far lower than the near-4.0% peak the market is currently pricing for Bank Rate.

However, economists at Investec see the Bank's reaction function differently, instead saying the Bank will now hike further as the fiscal stimulus gives rise to increased consumer demand.

"The Bank of England is likely to take note when setting policy rates: a higher peak in the Bank rate may well result," says Sandra Horsfield, economist at Investec.

NatWest Markets agree with this hypothesis, "the substantial energy support package (a mooted ~£150bn over 2 years) will boost demand and require additional monetary policy tightening," says Ross Walker, Chief UK Economist at NatWest Markets.

In response to the fiscal boost, NatWest revise up their forecast for Bank Rate to reach 3.5% from 3.0%: seeing 50bp coming September, November and December 25bp in February, leaving Bank Rate at 3.5%.

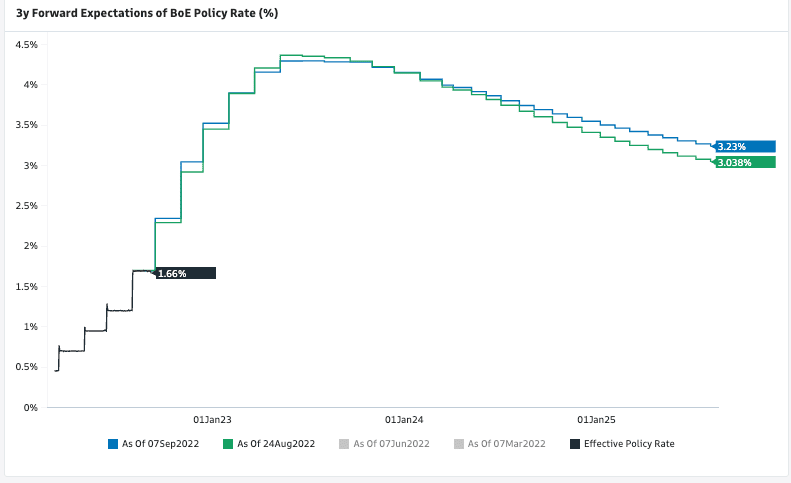

Above: UK rate hike expectations held by money markets, showing a peak in Bank Rate near 4.5% is expected. Image courtesy of Goldman Sachs.

All these projections are nevertheless below the current market implied ~4.0%, suggesting there will an inevitable reversal lower in market expectations.

Typically this would drag on the Pound.

But, the Pound is heavily oversold and interest rate expectations have been a poor guide of Sterling direction of late, implying any move lower in rate markets might not have a negative impact.

But one fundamental guide remains unchanged, and this is that general rule of thumb that economies with positive economic growth dynamics tend to command a strong currency.

All that matters for Sterling's outlook, therefore, is that growth prospects improve.

It's still early days, but Truss' energy plans appear to have helped greatly in this regard.

Near-term, the Pound remains near its lowest levels since 1985 against the U.S. Dollar and is at its lowest since June against the Euro.

Of the world's major currencies, it is the third-worst performer of 2022.

This confirms the overarching trend is against the Pound and there is no technical evidence to suggest any recovery has yet begun.

"While a step in the right direction for consumers, the move also raises questions about Britain’s fiscal health moving forward, a scenario likely to maintain general pressure on the pound," says Joe Manimbo, Senior Market Analyst at Western Union.

The full cost of the plans will be announced in due course, but this will be a tricky one to pin a figure on given it relies exclusively on forward gas prices, which are notoriously volatile at present.

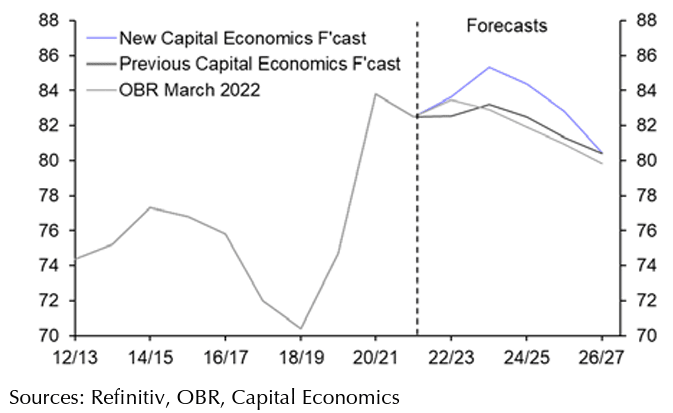

Above: UK government debt projections by Capital Economics.

Bond yields have risen of late, and are tipped to stay elevated, as a result of expectations for higher bond issuance by the government to fund the gas cap plan.

NatWest Markets - who are primary dealer in UK gilts - see the UK ten year gilt yield making a "regime shift" higher to above 4.0% over coming months.

Higher yields can prove supportive of the Pound, but for them to do so the market must believe the UK's economy will deliver robust growth.

Expect UK growth expectations to improve materially over coming weeks.