- GBP, JPY, EUR et al losses exacerbated by SNB FX sales

- Heavy selling seen as SNB looks to defend CHF from USD

- NZD, AUD & SEK all appear to feature in SNB FX reserves

- GBP, JPY, EUR risking further, ongoing underperformance

Image © Adobe Images

Pound Sterling sustained widespread losses earlier this week and there were strong indications, if not evidence that the breadth and depth of its declines resulted from an apparently successful attempt by the Swiss National Bank (SNB) to defend Switzerland’s Franc from a rampantly strong U.S. Dollar.

The Dollar bounced back from last week’s losses with vengeance during the prior trading session on Tuesday and it was amid this price action that Sterling and the New Zealand Dollar were seen vying with each other for the bottom of the major currency bucket during the latter half of the day.

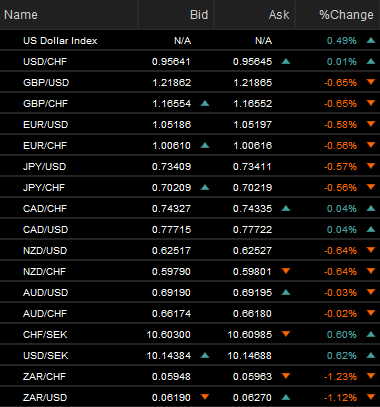

During this period there was an almost constant identical match between the performances of GBP/USD and GBP/CHF and likewise for some other currencies when measured against the Swiss Franc, including the Kiwi Dollar, which is illustrated in the various images throughout this article.

That identical match is called co-movement and has previously been found to indicate a common theme or factor driving the exchange rates that it's observed in, according to this research from the Bank of England (BoE).

Above: Selected exchange rates on Tuesday, 28 June. Shows co-movements between Dollar and Swiss Franc facing exchange rates. Source: Netdania Markets. Click image for closer inspection.

This co-movement is also a strong tell of what was afoot on Tuesday given that it took place in and around Swiss exchange rates and was coming so soon after the Swiss National Bank implied that it would sell currency reserves in order to keep the Franc from rackinging up inflationary losses.

“If there were to be an excessive appreciation of the Swiss franc, we would be prepared to purchase foreign currency. If the Swiss franc were to weaken, however, we would also consider selling foreign currency,” Swiss National Bank Chairman Thomas Jordan said on June 16.

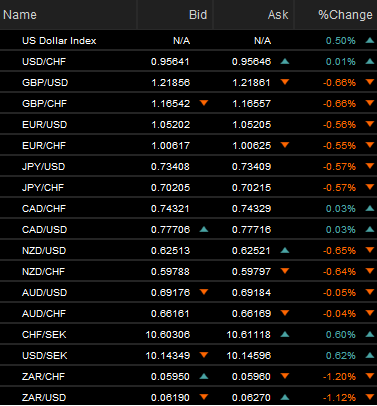

Above: Selected exchange rates on Tuesday, 28 June. Shows co-movements between Dollar and Swiss Franc facing exchange rates. Source: Netdania Markets. Click image for closer inspection.

“We will be observing the developments closely and are prepared to take the necessary measures in every situation to ensure price stability in Switzerland over the medium term,” he also said following the SNB’s surprise decision to lift its interest rate by 0.50% to -0.25% this month

Tuesday’s co-movement was strongest and most persistent in relation to Pound Sterling but it was also notably evident in relation to the Japanese Yen, Euro, Canadian Dollar and a whole bunch of other currencies that are not themselves listed as official reserve holdings of the Swiss National Bank.

Above: Selected exchange rates on Tuesday, 28 June. Shows co-movements between Dollar and Swiss Franc facing exchange rates. Source: Netdania Markets. Click image for closer inspection.

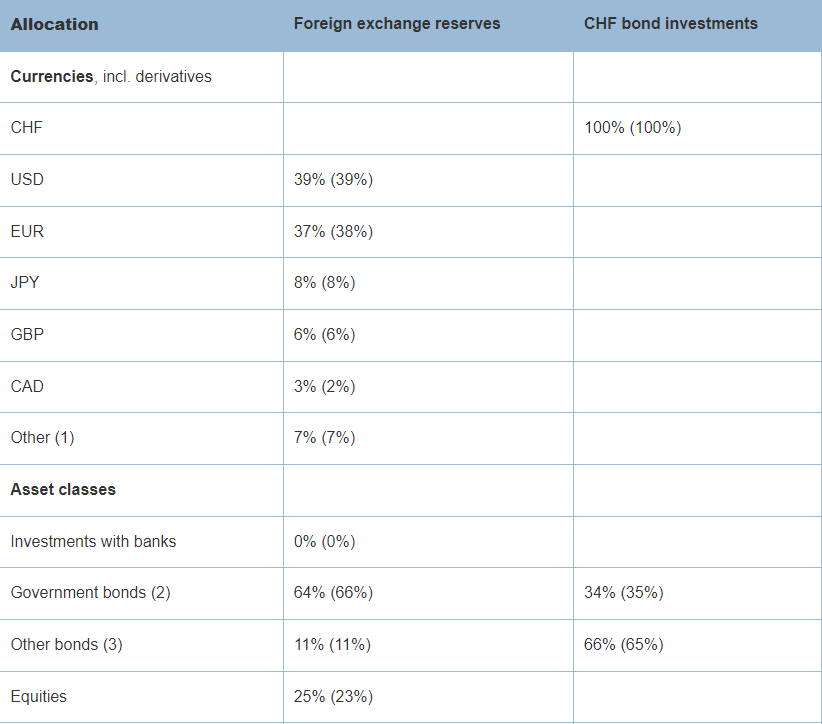

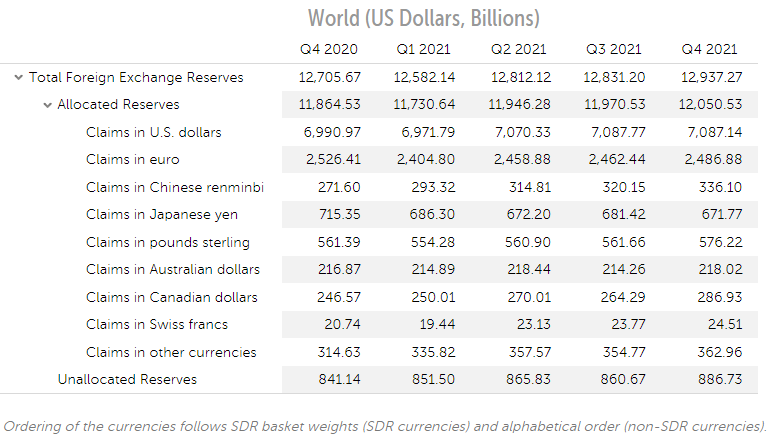

The Swiss National Bank’s official currency reserves are significant, having been valued at CHF1.01 BN (£871 BN) by the end of last year, while some 93% of them were held in U.S. Dollars, Euros, Japanese Yen, Pound Sterling and Canadian Dollars at the end of the first quarter 2022.

Sterling’s share of the reserves was 6% and equal to an estimated £52.2 BN in today’s money and around 11% of the entire $575 BN of reserve assets held in Sterling and known to the International Monetary Fund at the end of 2021.

Above: Allocation of Swiss National Bank reserve holdings. Source: Swiss National Bank.

However, the SNB also held a little more than that amount of the total portfolio, worth around 7% in the opening quarter, in smaller currencies that were listed collectively under the heading of “other” in the bank’s disclosures.

It’s never before been known outside of the SNB exactly which currencies constitute those “other” assets but Tuesday’s price action and the co-movements across the Swiss Franc exchange rate complex provided strong clues as to which some of those currencies they might be.

Above: Selected exchange rates on Tuesday, 28 June. Shows co-movements between Dollar and Swiss Franc facing exchange rates. Source: Netdania Markets. Click image for closer inspection.

There was very strong and persistent co-movement in the relevant New Zealand Dollar exchange rates on Tuesday and, albeit to a lesser extent, also in the relevant Australian Dollar and Swedish Krona exchange rates.

All of this took place in the latter half of the European trading session and from around the time when North America was beginning to join the crowd, at which point the U.S. Dollar began to strengthen broadly, and it persisted until some time after the close of European business hours on Tuesday.

Above: Selected exchange rates on Tuesday, 28 June. Shows co-movements between Dollar and Swiss Franc facing exchange rates. Source: Netdania Markets. Click image for closer inspection.

While it’s unlikely that Sterling, the Yen and Euro would ever avoid ceding ground to the U.S. Dollar in circumstances where it strengthens broadly, it was unusual for them to underperform ‘high beta’ currencies like those with commodity linkages, and especially those in emerging markets.

The fact that Sterling, the Yen, Euro and others like the New Zealand Dollar did underperform those other currencies is likely a testament of the breadth and extent to which the SNB’s reserve selling impacted the market as it sought to keep the USD/CHF rate from rising on Tuesday.

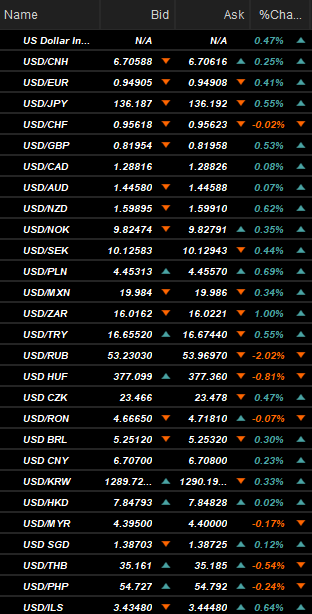

Above: Interbank reference rates for U.S. Dollar and performances on Tuesday. Source: Netdania Markets.

If there is any one thing to be inferred from this it could be a risk of further underperformance by the likes of the Pound, Yen and Euro in the short-term and for as long as the Dollar continues to place other currencies under pressure.

This is at the same time, however, par for the course with reserve currencies, which act like national savings assets for countries of the world with their central banks each and all obligated to provide liquidity in amounts necessary, at times requested and especially during periods of financial stress.

Above: Currency Composition of Official Foreign Exchange Reserves. Source: International Monetary Fund.